Equity Syndicates: A Comprehensive Guide for Investors

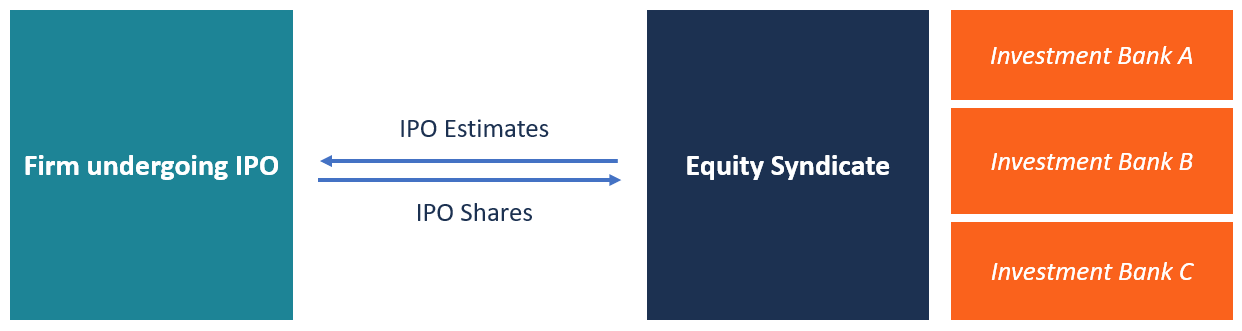

An equity syndicate refers to a group of investors who come together to determine the price and sell new IPOsInitial Public Offering (IPO)An Initial Public Offering (IPO) is the first sale of stocks issued by a company to the public. Prior to an IPO, a company is considered a private company, usually with a small number of investors (founders, friends, family, and business investors such as venture capitalists or angel investors). Learn what an IPO is to the public. The syndicate takes various considerations such as riskDefault Risk PremiumA default risk premium is effectively the difference between a debt instrument's interest rate and the risk-free rate. The default risk premium exists to compensate investors for an entity's likelihood of defaulting on their debt. and the financial status of the company when deciding on the price of the floated IPO. Equity syndicates are generally formed when the stock issue is too large to be managed by a single firm. Therefore, combining the efforts of several firms helps sell the new offering of shares quickly and completely.

The equity syndicate is headed by a lead underwriter who is responsible for directing the initial public stock offering. The typical members of an equity syndicate are the senior executives of investment banksList of Top Investment BanksList of the top 100 investment banks in the world sorted alphabetically. Top investment banks on the list are Goldman Sachs, Morgan Stanley, BAML, JP Morgan, Blackstone, Rothschild, Scotiabank, RBC, UBS, Wells Fargo, Deutsche Bank, Citi, Macquarie, HSBC, ICBC, Credit Suisse, Bank of America Merril Lynch. The members’ profit from the underwriting spread. This is the price difference between the price paid to the issuer and the public selling price.

How an Equity Syndicate Works

Since the equity syndicate members are committed to selling all the stocks on offer, they must buy shares from the issuer and sell them to the public. The practice subjects them to the risk of price decline. They mitigate this risk by spreading out the risk among all members of the syndicate.

Some members of the syndicate may receive a higher number of shares, and therefore, higher proportions of the underwriting spread. To avoid any disagreements about the sharing method, members of the syndicate usually sign an agreement that indicates the number of stocks allocated, fees, and their rights and obligations.

Price vs. Demand of the IPO

Once the IPO’s been floated and made public, there tends to be a higher demand for the stocks at the onset. In some cases, the demand for shares may exceed the supply. This will push up prices that investors must pay to become shareholdersStockholders EquityStockholders Equity (also known as Shareholders Equity) is an account on a company's balance sheet that consists of share capital plus in the issuers’ company. Initial price increases are often followed by price swings as demand decreases.

The Process of Determining the IPO Price

There are several steps involved when determining the price of an IPO. First, the underwriters seek pricing information from sales personnel who are experienced in IPOs, stock trading, and analyzing growth prospects. The equity syndicate members then convene a meeting where only members are allowed to participate.

The members use a closed bidding process to determine the price of the equity IPO. After the members agree on an IPO price, they are then allocated a percentage of shares before the IPO is floated in the market. Once the IPO is issued in the market, the syndicate members share the profits or losses depending on the changes in the IPO price.

Lead Underwriter

The lead underwriter is an investment bank that is tasked with directing the IPO on behalf of the issuing company. It leads an equity syndicate comprising other investment banks who help in pushing the IPO in the market. Once the offer’s been publicized, the IPO is sold to large customers such as institutional firms and retail clients with substantial capital to invest.

The lead underwriter in the equity syndicate receives a significant proportion of the profits for taking charge of the underwriting process. It is responsible for ensuring that all regulatory requirements by FINRA or the Securities and Exchange Commission are met. The lead underwriter allocates stocks to each member of the syndicate according to their financial capability and preferences. Also, it heads negotiations on the offering price and the timing of the offer.

During the issue, there is usually a lot of hype surrounding the offer, which increases the demand for the stocks. In return, the lead underwriter takes advantage of the excess demand to create an over-allotment, which results in more capital for the client and more commissions for the investment bank leading the issue.

The primary responsibility of the lead underwriter is to determine the final offering price. Setting the right price is important since this will influence how easy or hard it will be to sell the shares to interested investors. The price will also determine how much money the stock issuer and the syndicate obtain from the issue.

More Resources

We hope you enjoyed reading CFI’s explanation of an equity syndicate. CFI is the official provider of the Financial Modeling and Valuation Analyst (FMVA)™Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program, designed to transform anyone into a world-class financial analyst. To keep learning and developing your knowledge of financial analysis, we highly recommend the additional resources below:

- Capital Raising ProcessCapital Raising ProcessThis article is intended to provide readers with a deeper understanding of how the capital raising process works and happens in the industry today. For more information on capital raising and different types of commitments made by the underwriter, please see our underwriting overview.

- OverallotmentGreenshoe / OverallotmentOverallotment, also known as greenshoe option, is an option that is available to underwriters to sell additional shares during an Initial Public Offering (IPO). The underwriters are allowed to sell 15% more shares than the number of shares they originally planned to sell, and the option

- IPO ProcessIPO ProcessThe IPO Process is where a private company issues new and/or existing securities to the public for the first time. The 5 steps discussed in detail

- Roadshow PresentationRoadshow PresentationA roadshow presentation is a series of in-person meetings held between the management team of a corporation raising money and the institutional investors.

-

Commodity Valuation: Understanding Intrinsic Value & Market Pricing

Commodity valuation is the process of deriving the intrinsic value of a commodity under optimal market conditions. In a perfectly competitive free market, the price of a commodity reflects the intrins

-

Covered Calls: A Comprehensive Guide for Investors

A covered call is a risk management and an options strategy that involves holding a long position in the underlying asset (e.g., stockStockWhat is a stock? An individual who owns stock in a company is

invest

- Understanding Divergence in Technical Analysis: A Guide

- Understanding Equity Derivatives: A Comprehensive Guide

- Understanding Forward Prices: Definition & How They Work

- Growth Equity: Investing in Expanding Businesses | [Your Company Name]

- Understanding Hedging Strategies: A Comprehensive Guide

- Understanding Offering Price: A Guide for Investors

- Understanding Slippage in Trading: Causes & Impact

- Understanding Strangle Options: A Comprehensive Guide

- Understanding Volatility: A Key Indicator of Investment Risk

-

Understanding Call Prices: Callable Bonds & Preferred Stocks

Understanding Call Prices: Callable Bonds & Preferred StocksA call price refers to the price that a preferred stock or bond issuer would pay to buyers if they chose to redeem the callable security before the maturity date. The price is set during the issuance ...

-

Call Warrants: Understanding Rights & Investment Potential

Call Warrants: Understanding Rights & Investment PotentialA call warrant gives the holder of the investment the right, not the obligation, to purchase the underlying financial securities at a specific price on or before a certain date.If the holder does not ...