Understanding Negative Convexity in Bonds: Risks & Implications

Negative convexity occurs when a bond’s duration increases in conjunction with an increase in yield. The bond price will drop as the yield grows. When interest ratesInterest RateAn interest rate refers to the amount charged by a lender to a borrower for any form of debt given, generally expressed as a percentage of the principal. fall, bond prices rise; however, a bond with negative convexity diminishes in value as interest rates decline.

In order to fully understand negative convexity, it is important to first understand convexity, bond prices, bond yields, interest rates, and bond durationDurationDuration is one of the fundamental characteristics of a fixed-income security (e.g., a bond) alongside maturity, yield, coupon, and call features..

Summary

- Negative convexity occurs when a bond’s duration increases in conjunction with an increase in yields.

- Convexity is the measure of the curvature in the relationship between a bond’s yield and its price. Convexity illustrates how, as interest rates change, the duration of a bond fluctuates.

- The relationship between bond prices and interest rates is negative.

Convexity

Convexity is the measure of the curvature in the relationship between a bond’s yield and its price. It illustrates how, as interest rates change, the duration of a bond fluctuates.

Bond Prices and Interest Rates

There is a negative link or relationship between bond prices and interest rates:

- As interest rates grow or rise, bond prices decrease or fall.

- When interest rates decrease or fall, bond prices grow.

The negative relationship can be attributed to the concept that as rates rise, the bond may lag in the earnings it offers a potential investor.

Bond Yields and Interest Rates

- As interest rates rise, bonds entering the market will have higher yields, as they are issued at new, higher rates.

- As rates increase, investors demand a greater yield from the bonds they purchase. Hence, when interest rates rise, issuers of such instruments should also raise their yields to remain competitive.

Bond Duration

Bond duration helps in measuring how much a bond’s price changes as interest rates fluctuate. Given a high duration, a bond’s price will move in the inverse direction of interest rate fluctuations to a greater degree. The opposite is also true; a lower duration means that the bond price will display less movement.

Modified Duration

Following the assumption that a change in price remains constant with an increase or decrease in yield, the modified duration measures the degree of change in a bond’s price. The adjustment in the bond price according to the change in yield is convex. It helps in improving price change estimations.

Bond Convexity Formula

Where:

- P: Bond price

- Y: Yield to maturity

- T: Maturity in years

- CFt: Cash flow at time t

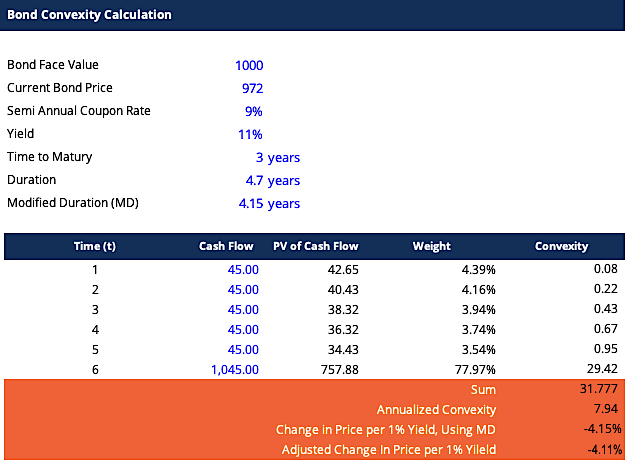

Calculating Convexity

Here is an Excel example of calculating convexity:

The results in our example demonstrate that a convexity of 7.94 can be used to predict the price change with a percentage change in yield that would be the following:

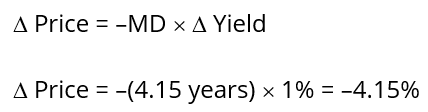

Using the Modified Duration

It shows that the price would decrease by $40.34.

In order to properly take the convexity graph shape, as seen in the graph at the beginning of this article, the price change formula must be adjusted to:

Here is the Adjusted Price Change calculation:

It shows that the price will decrease by $39.95 and not by $40.34.

Conclusion

- The price of the bond with the modified duration is $902.44 with a 1% growth in yield.

- The price of the bond with modified duration and convexity is $902.82 at a 1% growth.

- The 0.99 difference in the price change is attributed to the non-linearity of the price yield curve.

Convexity as a Risk Management Tool

Convexity can be used to determine the risk levelRiskIn finance, risk is the probability that actual results will differ from expected results. In the Capital Asset Pricing Model (CAPM), risk is defined as the volatility of returns. The concept of “risk and return” is that riskier assets should have higher expected returns to compensate investors for the higher volatility and increased risk. of a bond – the greater the convexity of the bond, the greater the sensitivity of its price to interest rate movements.

If two bonds are being analyzed for investment purposes and they have comparable yields and durations, the bond with the higher convexity is preferable in falling or stable interest rate environments, as the change in price is larger.

Reiterating Negative Convexity

Now, after gaining an understanding of convexity, we can return to our basis – negative convexity.

Convexity can be either negative or positive:

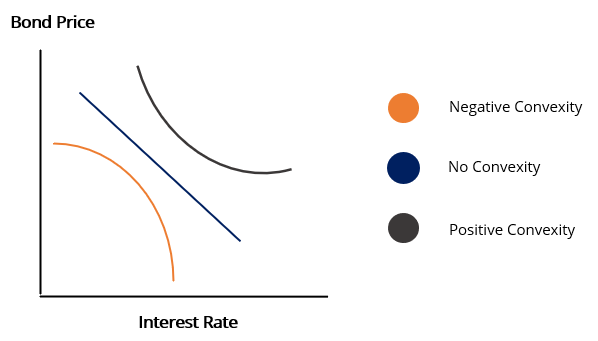

1. Positive convexity

It occurs when the duration and the yield of a bond decrease or increase together, thus they are positively correlated. The yield curve for bonds with positive convexities usually follows an upward movement.

2. Negative convexity

It occurs when there is an inverse relationship between the yield and the duration. It means that with a decline in duration, there is an increase in yield. Therefore, they are negatively correlated. The yield curve for a bond with a negative convexity usually follows a downward movement.

Related Readings

CFI is the official provider of the global Commercial Banking & Credit Analyst (CBCA)™Program Page - CBCAGet CFI's CBCA™ certification and become a Commercial Banking & Credit Analyst. Enroll and advance your career with our certification programs and courses. certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful:

- Bond PricingBond PricingBond pricing is the science of calculating a bond's issue price based on the coupon, par value, yield and term to maturity. Bond pricing allows investors

- Interest Rate RiskInterest Rate RiskInterest rate risk is the probability of a decline in the value of an asset resulting from unexpected fluctuations in interest rates. Interest rate risk is mostly associated with fixed-income assets (e.g., bonds) rather than with equity investments.

- Negative-Yielding BondsNegative-Yielding BondsNegative-yielding bonds are bonds that cause bondholders to lose money when they mature. This happens when holders of such bonds will end up with less money than what they used to purchase them.

- Yield CurveYield CurveThe Yield Curve is a graphical representation of the interest rates on debt for a range of maturities. It shows the yield an investor is expecting to earn if he lends his money for a given period of time. The graph displays a bond's yield on the vertical axis and the time to maturity across the horizontal axis.

-

Negative Correlation Explained: Understanding Inverse Relationships

A negative correlation is a relationship between two variables that move in opposite directions. In other words, when variable A increases, variable B decreases. A negative correlation is also known a

-

Understanding Negative Equity: Causes, Risks & Solutions

The concept of negative equity arises when the value of an asset (which was financed using debt) falls below the amount of the loan/mortgage that is owed to the bank in exchange for the assetTangible

invest

- Understanding Call Prices: Callable Bonds & Preferred Stocks

- Coupon Bonds: Understanding Fixed Income & Interest Payments

- Discount Bonds: Understanding Pricing & Secondary Markets

- Understanding Divergence in Technical Analysis: A Guide

- Understanding Forward Prices: Definition & How They Work

- Understanding Hedging Strategies: A Comprehensive Guide

- Understanding Negative Carry: Risks and Strategies

- Negative Gearing Explained: Understanding Investment Losses & Tax Benefits

- Understanding Noncallable Securities: A Comprehensive Guide

-

Personal Bond Explained: Release from Jail Without Bail

Personal Bond Explained: Release from Jail Without BailA personal bond, which is also called personal recognizance and own recognizance, is a written contract in which a person who has been arrested agrees to appear at all required court dates and promise...

-

Understanding Bond Duration: A Key Fixed Income Metric

Understanding Bond Duration: A Key Fixed Income MetricDuration is one of the fundamental characteristics of a fixed-income security (e.g., a bondBondsBonds are fixed-income securities that are issued by corporations and governments to raise capital....