Understanding Bond Duration: A Key Fixed Income Metric

Duration is one of the fundamental characteristics of a fixed-income security (e.g., a bondBondsBonds are fixed-income securities that are issued by corporations and governments to raise capital. The bond issuer borrows capital from the bondholder and makes fixed payments to them at a fixed (or variable) interest rate for a specified period.) alongside maturity, yield, couponCoupon RateA coupon rate is the amount of annual interest income paid to a bondholder, based on the face value of the bond., and call features. It is a tool used in the assessment of the price volatility of a fixed-income security.

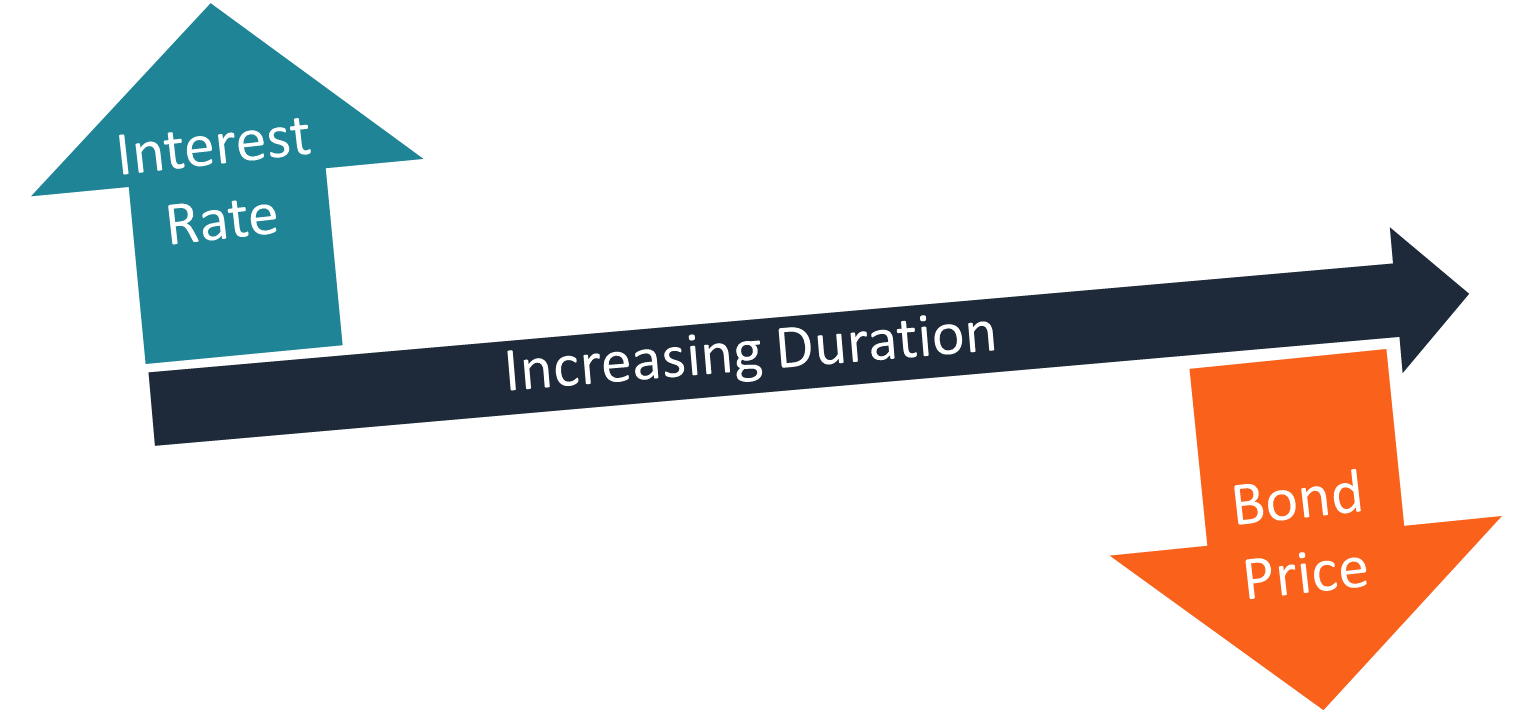

Since the interest rateInterest RateAn interest rate refers to the amount charged by a lender to a borrower for any form of debt given, generally expressed as a percentage of the principal. is one of the most significant drivers of a bond’s value, duration measures the sensitivity of the value fluctuations to changes in interest rates. The general rule states that a longer duration indicates a greater likelihood that the value of a bond will fall as interest rates increase.

Duration is commonly used in the portfolio and risk managementRisk ManagementRisk management encompasses the identification, analysis, and response to risk factors that form part of the life of a business. It is usually done with of fixed-income instruments. Using interest rate forecasts, a portfolio manager can change a portfolio’s composition to align its duration with the expected level of interest rates.

However, duration only reveals one side of a fixed-income security. A full analysis of the fixed-income asset must be done using all available characteristics.

CFI’s Fixed Income Fundamentals Course covers the essential topics for fixed-income valuation.

Types of Duration

The duration metric comes in several modifications. The most common are the Macaulay duration, modified duration, and effective duration.

1. Macaulay Duration

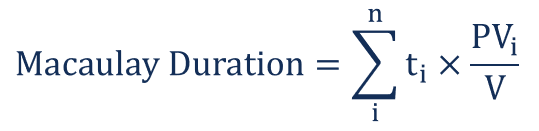

Macaulay duration is a weighted average of the times until the cash flows of a fixed-income instrument are received. The concept was introduced by Canadian economist Frederick Macaulay. It is a measure of the time required for an investor to be repaid the bond’s price by the bond’s total cash flows. The Macaulay duration is measured in units of time (e.g., years).

The Macaulay duration for coupon-paying bonds is always lower than the bond’s time to maturity. For zero-coupon bonds, the duration equals the time to maturity.

The formula for the calculation of Macaulay duration is expressed in the following way:

Where:

- ti – The time until the ith cash flow from the asset will be received

- PVi – The present value of the ith cash flow from the asset

- V – The present value of all cash flows from the asset

2. Modified Duration

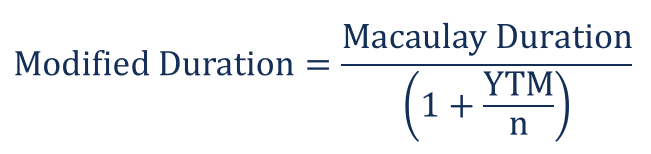

Relative to the Macaulay duration, the modified duration metric is a more precise measure of price sensitivity. It is primarily applied to bonds, but it can also be used with other types of securities that can be considered as a function of yield.

The modified duration figure indicates the percentage change in the bond’s value given an X% interest rate change. Unlike the Macaulay duration, modified duration is measured in percentages.

The modified duration is often considered as an extension of the Macaulay duration. It is supported by the following mathematical formula:

Where:

- YTM – The yield to maturity of a bond

- n – The frequency of compounding

3. Effective Duration

Effective duration is a measure of the duration for bonds with embedded options (e.g., callable bonds). Unlike the modified duration and Macaulay duration, effective duration considers fluctuations in the bond’s price movements relative to the changes in the bond’s yield to maturity (YTM). In other words, the measure takes into account possible fluctuations in the expected cash flows of a bond.

The effective duration is calculated using the following formula:

Where:

- V–Δy – The bond’s value if yield falls by y%

- V+Δy – The bond’s value if yield rises by y%

- V0 – The present value of all cash flows of the bond

- Δy – The yield change

Related Readings

To keep advancing your career, the additional CFI resources below will be useful:

- Bond PricingBond PricingBond pricing is the science of calculating a bond's issue price based on the coupon, par value, yield and term to maturity. Bond pricing allows investors

- Debt Capital MarketsDebt Capital Markets (DCM)Debt Capital Markets (DCM) groups are responsible for providing advice directly to corporate issuers on the raising of debt for acquisitions, refinancing of existing debt, or restructuring of existing debt. These teams operate in a rapidly moving environment and work closely with an advisory partner

- Equity Risk PremiumEquity Risk PremiumEquity risk premium is the difference between returns on equity/individual stock and the risk-free rate of return. It is the compensation to the investor for taking a higher level of risk and investing in equity rather than risk-free securities.

- Fixed Income TradingFixed Income TradingFixed income trading involves investing in bonds or other debt security instruments. Fixed income securities have several unique attributes and factors that

-

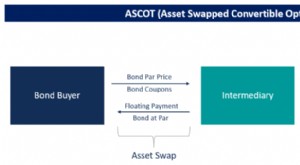

ASCOT Options: Understanding Asset-Swapped Convertible Options

The term ASCOT is short for Asset Swapped Convertible Option Transaction. It is an American style call option to buy back a convertible bond. It falls under the category of financial products called s

-

Asset Swap Explained: Definition, OTC Trading & Key Concepts

An asset swap is a derivative contract between two parties that swap fixed and floating assets. The transactions are done over-the-counterOver-the-Counter (OTC)Over-the-counter (OTC) is the trading of

finance

- Personal Bond Explained: Release from Jail Without Bail

- Coupon Bonds: Understanding Fixed Income & Interest Payments

- Discount Bonds: Understanding Pricing & Secondary Markets

- Understanding Dollar Duration: A Guide for Bond Investors

- Understanding Duration Drift in Asset-Liability Management

- Effective Duration Explained: Bond Price Sensitivity

- Understanding Key Rate Duration: A Guide for Bond Investors

- Macaulay Duration: Understanding Bond Interest Rate Risk

- Understanding Modified Duration: A Key Bond Valuation Metric

-

Understanding Amortizable Bond Premiums: A Comprehensive Guide

Understanding Amortizable Bond Premiums: A Comprehensive GuideAn amortizable bond premium refers to the excess amount paid for a bond over its face value or par valuePar ValuePar Value is the nominal or face value of a bond, or stock, or coupon as indicated on a...

-

Amortized Bonds: Understanding Principal Repayment

Amortized Bonds: Understanding Principal RepaymentAn amortized bond is a bond with the principal amount – otherwise known as face value –regularly paid down over the life of the bond. The bond’s principal is divided up according to ...