Putable Bonds: Understanding Investor Protection and Early Redemption

A putable bond (put bond or retractable bond) is a type of bond that provides the holder of a bond (investor) the right, but not the obligation, to force the issuer to redeem the bond before its maturity date. In other words, it is a bond with an embedded put optionPut OptionA put option is an option contract that gives the buyer the right, but not the obligation, to sell the underlying security at a specified price (also known as strike price) before or at a predetermined expiration date. It is one of the two main types of options, the other type being a call option.. Putable bonds are directly opposite to callable bonds.

If the embedded put option is exercised, the bondholder receives the principal value of the bond at par valuePar ValuePar Value is the nominal or face value of a bond, or stock, or coupon as indicated on a bond or stock certificate. It is a static value. In certain cases, the bonds can be retracted as a result of extraordinary events. However, more frequently, the embedded put option can be exercised after a predetermined date.

How are put options important to investors and issuers?

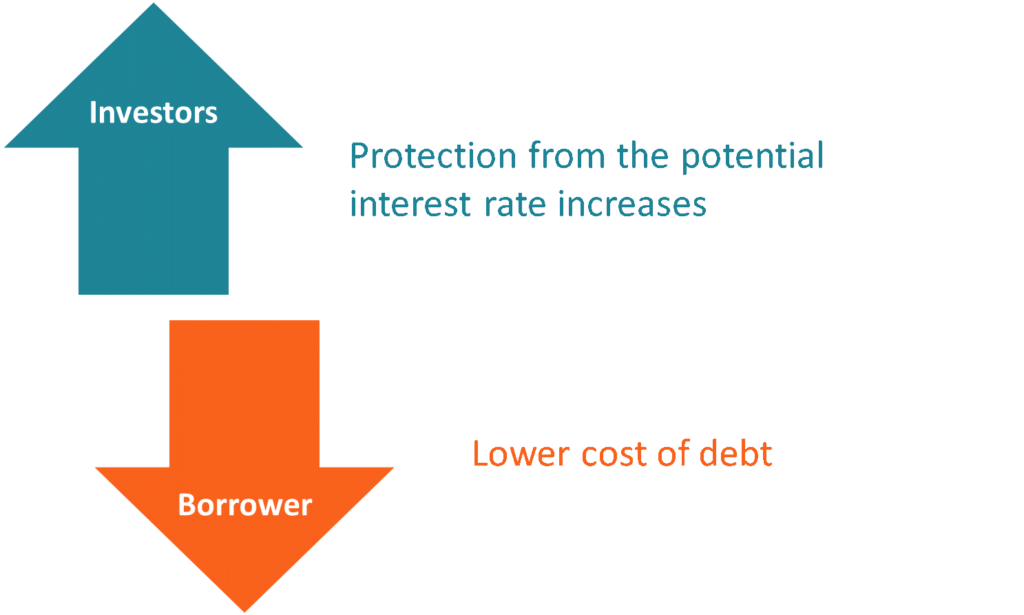

Similar to callable bonds, the rationale behind putable bonds is related to the inverse relationship between interest ratesInterest RateAn interest rate refers to the amount charged by a lender to a borrower for any form of debt given, generally expressed as a percentage of the principal. and the price of bonds. Since the value of the bonds declines as interest rates rise, they provide investors with protection from potential interest rate increases.

At the same time, the bond issuers reduce their cost of debtCost of DebtThe cost of debt is the return that a company provides to its debtholders and creditors. Cost of debt is used in WACC calculations for valuation analysis. by providing lower yields on the bonds. Investors accept lower yields in exchange for the opportunity to exit the investments in case of unfavorable market conditions.

How do putable bonds work?

Let’s consider the following example to understand how these bonds work:

ABC Corp. issues putable bonds with a face value of $100 and a coupon rate 4.75%. The current interest rate is 4%. The bonds will mature in 10 years.

The put option provides investors with the right to force ABC to redeem the bonds after the first five years.

If, after the first five years of the bonds’ life, interest rates have significantly increased, the investors do not have an incentive to keep the bonds until maturity. Rather than holding the bonds to maturity, they can exercise the embedded put option and receive the principal amount of their initial investment. They can then use the proceeds to invest in newly issued bonds with a higher coupon (interest) rate.

However, if interest rates remain the same or decline, the investors do not have an incentive to exercise the put option. They will likely hold the bonds until maturity. In such a scenario, both parties will enjoy the same payoff as in plain-vanilla bonds.

Note that the coupon rate of putable bonds may be slightly lower than that of plain-vanilla bonds. This is to compensate the issuer for the additional risk of investors exercising the put option.

How to find the value of a putable bond?

Valuing putable bonds differs from valuing plain-vanilla bonds because of the embedded put option. Since the option provides investors with the right to force the issuers to redeem the bonds, the put option affects the price of a (putable) bond.

The fair market price of a (putable) bond can be found using the following formula:

Where:

- Price (Plain – Vanilla Bond) – the price of a plain-vanilla bond that shares similar features with a (putable) bond.

- Price (Put Option) – the price of a put option to redeem the bond prior to maturity.

Additional resources

CFI is the official provider of the global Financial Modeling & Valuation Analyst (FMVA)™Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program, designed to help anyone become a world-class financial analyst. To keep learning and advancing your career, the additional resources below will be useful:

- Margin TradingMargin TradingMargin trading is the act of borrowing funds from a broker with the aim of investing in financial securities. The purchased stock serves as collateral for the loan. The primary reason behind borrowing money is to gain more capital to invest

- Options: Calls and PutsOptions: Calls and PutsAn option is a derivative contract that gives the holder the right, but not the obligation, to buy or sell an asset by a certain date at a specified price.

- Rate of ReturnRate of ReturnThe Rate of Return (ROR) is the gain or loss of an investment over a period of time copmared to the initial cost of the investment expressed as a percentage. This guide teaches the most common formulas

- SpeculationSpeculationSpeculation is the buying of an asset or financial instrument with the hope that the price of the asset or financial instrument will increase in the future.

-

Profit Sharing Bonds: Understanding Investment Income & Potential

A profit sharing bond is a fixed income security whereby the holder receives regular interest payments and a share in the profits or dividends of the bond-issuing company. Other Nam

-

Understanding Term to Maturity: A Key Bond Concept

Term to maturity is the remaining life of a bond or other type of debt instrument. The duration ranges between the time when the bond is issued until its maturity date when the issuer is required to r

invest

- Understanding Bonds: A Comprehensive Guide for Investors

- Callable Bonds: Understanding Issuer Redemption Rights

- Convertible Bonds: A Comprehensive Guide for Investors

- Green Bonds: Financing a Sustainable Future | [Your Company Name]

- High-Yield Bonds: Understanding Risk & Potential Returns

- Kangaroo Bonds: A Guide to Australian Dollar Debt

- L Bonds: Understanding Unrated Life Insurance Bonds

- Municipal Bonds: A Comprehensive Guide for Investors

- Understanding Bonds: A Comprehensive Guide for Investors

-

General Obligation Bonds (GO Bonds): A Comprehensive Guide

General Obligation Bonds (GO Bonds): A Comprehensive GuideA general obligation (GO) bond is a type of municipal bond in which the bond repayments (interest and principalPrincipal PaymentA principal payment is a payment toward the original amount of a loan th...

-

Understanding High-Yield Bond Spreads: A Comprehensive Guide

Understanding High-Yield Bond Spreads: A Comprehensive GuideA high-yield bond spread, also known as a credit spread, is the difference in yields between multiple high-yield bonds, expressed in basis points or percentage points. A high-yield bond is a term that...