Asset Allocation: A Comprehensive Guide to Investment Risk Management

Asset allocation refers to an investment strategy in which individuals divide their investment portfolios between different diverse asset classes to minimize investment risks. The asset classesAsset ClassAn asset class is a group of similar investment vehicles. They are typically traded in the same financial markets and subject to the same rules and regulations. fall into three broad categories: equitiesStockWhat is a stock? An individual who owns stock in a company is called a shareholder and is eligible to claim part of the company’s residual assets and earnings (should the company ever be dissolved). The terms "stock", "shares", and "equity" are used interchangeably., fixed-incomeTrading & InvestingCFI's trading & investing guides are designed as self-study resources to learn to trade at your own pace. Browse hundreds of articles on trading, investing and important topics for financial analysts to know. Learn about assets classes, bond pricing, risk and return, stocks and stock markets, ETFs, momentum, technical, and cash and equivalentsCash EquivalentsCash and cash equivalents are the most liquid of all assets on the balance sheet. Cash equivalents include money market securities, banker's acceptances. Anything outside these three categories (e.g., real estate, commodities, art) is often referred to as alternative assets.

Factors Affecting Asset Allocation Decision

When making investment decisions, an investors’ portfolio distribution is influenced by factors such as personal goals, level of risk tolerance, and investment horizon.

1. Goal factors

Goal factors are individual aspirations to achieve a given level of return or saving for a particular reason or desire. Therefore, different goals affect how a person invests and risks.

2. Risk tolerance

Risk tolerance refers to how much an individual is willing and able to lose a given amount of their original investment in anticipation of getting a higher return in the future. For example, risk-averse investors withhold their portfolio in favor of more secure assets. In contrast, more aggressive investors risk most of their investments in anticipation of higher returns. Learn more about risk and returnRisk and ReturnIn investing, risk and return are highly correlated. Increased potential returns on investment usually go hand-in-hand with increased risk. Different types of risks include project-specific risk, industry-specific risk, competitive risk, international risk, and market risk..

3. Time horizon

The time horizon factor depends on the duration an investor is going to invest. Most of the time, it depends on the goal of the investment. Similarly, different time horizons entail different risk tolerance.

For example, a long-term investment strategy may prompt an investor to invest in a more volatile or higher risk portfolio since the dynamics of the economy are uncertain and may change in favor of the investor. However, investors with short-term goals may not invest in riskier portfolios.

How Asset Allocation Works

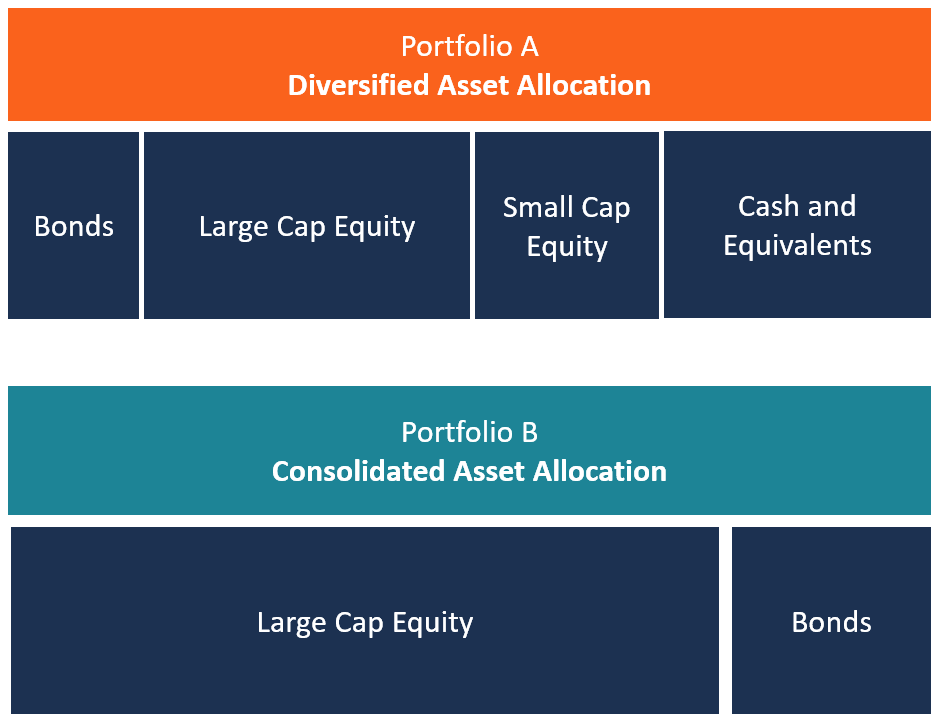

Financial advisors usually advise that to reduce the level of volatility of portfolios, investors must diversify their investment into various asset classes. Such basic reasoning is what makes asset allocation popular in portfolio management because different asset classes will always provide different returns. Thus, investors will receive a shield to guard against the deterioration of their investments.

Example of Asset Allocation

Let’s say Joe is in the process of creating a financial plan for his retirement. Therefore, he wants to invest his $10,000 saving for a time horizon of five years. So, his financial advisor may advise Joe to diversify his portfolio across the three major categories at a mix of 50/40/10 among stocks, bonds, and cash. His portfolio may look like below:

- Stocks

- Small-Cap Growth Stocks – 25%

- Large-Cap Value Stocks – 15%

- International stocks – 10%

- Bonds

- Government bonds – 15%

- High yield bonds – 25%

- Cash

- Money market – 10%

The distribution of his investment across the three broad categories, therefore, may look like this: $5,000/$4,000/$1,000.

Strategies for Asset Allocation

In asset allocation, there is no fixed rule on how an investor may invest and each financial advisor follows a different approach. The following are the top two strategies used to influence investment decisions.

1. Age-based Asset Allocation

In age-based asset allocation, the investment decision is based on the age of the investors. Therefore, most financial advisors advise investors to make the stock investment decision based on a deduction of their age from a base value of a 100. The figure depends on the life expectancy of the investor. The higher the life expectancy, the higher the portion of investments committed to riskier arenas, such as the stock market.

Example

Using the previous example, let’s assume that Joe is now at 50 years and he is looking forward to retiring at 60. According to the age-based investment approach, his advisor may advise him to invest in stocks in a proportion of 50%, then the rest in other assets. This is because when you subtract his age (50) from a hundred-base value, you’ll get 50.

2. Life-cycle funds Asset Allocation

In life-cycle funds allocation or targeted-date, investors maximize their return on investmentReturn on Investment (ROI)Return on Investment (ROI) is a performance measure used to evaluate the returns of an investment or compare efficiency of different investments. (ROI) based on factors such as their investment goals, their risk tolerance, and their age. This kind of portfolio structure is complex due to standardization issues. In fact, every investor has unique differences across the three factors.

Example

Let’s say Joe’s original investment mix is 50/50. After a time horizon of five years, his risk tolerance against stock may increase to 15%. As a result, he may sell his 15% of bonds and re-invest the portion in stocks. His new mix will be 65/35. This ratio may continue to change over time based on the three factors: investment goals, risk tolerance, and age.

Examples of Other Strategies

1. Constant-Weight Asset Allocation

The constant-weight asset allocation strategy is based on the buy-and-hold policy. That is, if a stock loses value, investors buy more of it. However, if it increases in price, they sell a bigger proportion. The goal is to ensure the proportions never deviate by more than 5% of the original mix.

2. Tactical Asset Allocation

The tactical asset allocation strategy addresses the challenges that result from strategic asset allocation relating to the long-run investment policies. Therefore, tactical asset allocation aims at maximizing short-term investment strategies. As a result, it adds more flexibility in coping with the market dynamics so that the investors invest in higher returning assets.

3. Insured Asset Allocation

For investors averse to risk, the insured asset allocation is the ideal strategy to adopt. It involves setting a base asset value from which the portfolio should not drop. If it drops, the investor takes the necessary action to avert the risk. Otherwise, as far as they can get a value slightly higher than the base asset value, they can comfortably buy, hold, or even sell.

4. Dynamic Asset Allocation

The dynamic asset allocation is the most popular type of investment strategy. It enables investors to adjust their investment proportion based on the highs and lows of the market and the gains and losses in the economy.

More Resources

CFI offers the Financial Modeling & Valuation Analyst (FMVA)®Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program for those looking to take their careers to the next level. To learn more and expand your career, explore the additional CFI resources below:

- Guide to Portfolio Management ProcessPortfolio ManagerPortfolio managers manage investment portfolios using a six-step portfolio management process. Learn exactly what does a portfolio manager do in this guide. Portfolio managers are professionals who manage investment portfolios, with the goal of achieving their clients’ investment objectives.

- Equity vs Fixed IncomeEquity vs Fixed IncomeEquity vs Fixed Income. Equity and fixed income products are financial instruments that have very important differences every financial analyst should know. Equity investments generally consist of stocks or stock funds, while fixed income securities generally consist of corporate or government bonds.

- Risk and ReturnRisk and ReturnIn investing, risk and return are highly correlated. Increased potential returns on investment usually go hand-in-hand with increased risk. Different types of risks include project-specific risk, industry-specific risk, competitive risk, international risk, and market risk.

- Stock Investment StrategiesStock Investment StrategiesStock investment strategies pertain to the different types of stock investing. These strategies are namely value, growth and index investing. The strategy an investor chooses is affected by a number of factors, such as the investor’s financial situation, investing goals, and risk tolerance.

-

Value at Risk (VaR): Understanding Investment Risk

Value at risk is a method that is used to determine the possible risk of loss for a particular type of investment. This is a strategy that attempts to determine what the worst-case scenario is f

-

Understanding Risk Aversion in Investing: A Beginner's Guide

The term risk aversion is often applied to certain types of investors. Here are the basics of risk aversion and what it means to investors. Risk Aversion The term risk aversion basically means t

Business strategy

- Understanding Risk Grades: An Investor's Guide

- Constant Weight Asset Allocation: A Simple Guide

- Dynamic Asset Allocation: A Comprehensive Guide

- Strategic Asset Allocation (SAA): A Comprehensive Guide

- Tactical Asset Allocation (TAA): A Comprehensive Guide

- Portfolio Diversification: Reduce Risk & Enhance Returns

- Asset Allocation: 4 Key Benefits for Investors

- Socially Responsible Investing: Understanding Asset Allocation

- Asset Allocation: A Comprehensive Guide to Portfolio Diversification

-

Understanding Inherent Risk: A Key Concept in Risk Management

Understanding Inherent Risk: A Key Concept in Risk ManagementInherent risk refers to the natural risk level in a process that has not been controlled or mitigated in risk managementRisk ManagementRisk management encompasses the identification, analysis, and res...

-

Understanding Leases: Types, Classifications, and Key Concepts

Understanding Leases: Types, Classifications, and Key ConceptsLeases are contracts in which the property/asset owner allows another party to use the property/asset in exchange for something, usually money or other assets. The two most common types of leases...