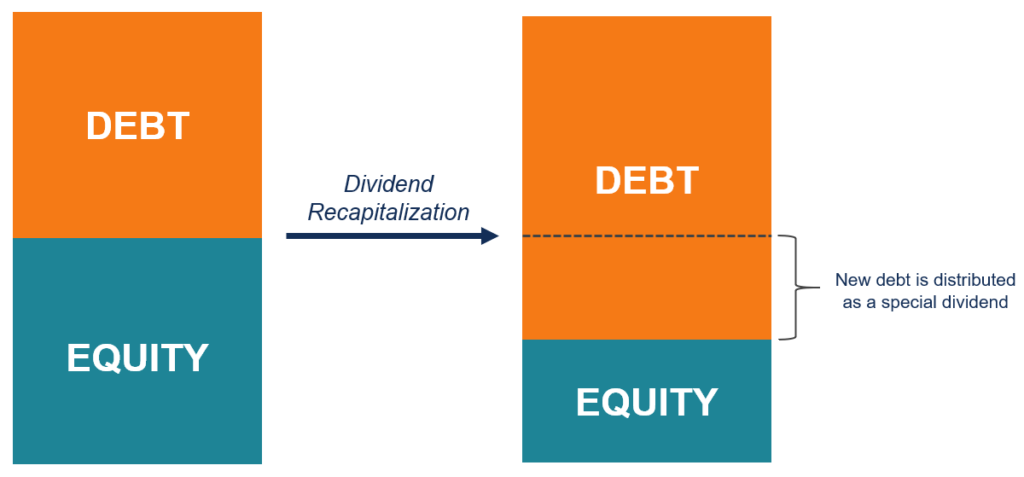

Dividend Recapitalization: Definition & How It Works

Dividend recapitalization (frequently referred to as dividend recap) is a type of leveraged recapitalization that involves the issuing of new debt by a private company,Private vs Public CompanyThe main difference between a private vs public company is that the shares of a public company are traded on a stock exchange, while a private company's shares are not. that is later used to pay a special dividend to shareholders (thereby, reducing the company’s equity financing in relation to debt financing). The source of the dividends distributed as a result of dividend recapitalization is newly incurred debt, not the company’s earnings. The recapitalization directly impacts the company’s capital structure since its leverage increases.

Uses of Dividend Recapitalization

1. To exit an investment

Dividend recapitalization is primarily used by private equity firmsTop 10 Private Equity FirmsWho are the top 10 private equity firms in the world? Our list of the top ten largest PE firms, sorted by total capital raised. Common strategies within P.E. include leveraged buyouts (LBO), venture capital, growth capital, distressed investments and mezzanine capital. and private equity groups (PEG). In private equity, it is frequently used as a method of exiting an investment. In such a case, dividend recapitalization is a viable alternative to conventional exit routes such as a sale of the stake to another private equity firm or an Initial Public Offering (IPO)Initial Public Offering (IPO)An Initial Public Offering (IPO) is the first sale of stocks issued by a company to the public. Prior to an IPO, a company is considered a private company, usually with a small number of investors (founders, friends, family, and business investors such as venture capitalists or angel investors). Learn what an IPO is.

2. To recover an initial investment

Additionally, dividend recapitalization can be employed in situations when an investor (investment company) wishes to recover its initial investment without losing its stake in a company.

3. To avoid using earned profits for dividends

Furthermore, dividend recapitalization eliminates the necessity to use the company’s earned profits to distribute dividends to shareholders. Some companies may also depend on it in a low-interest rateInterest RateAn interest rate refers to the amount charged by a lender to a borrower for any form of debt given, generally expressed as a percentage of the principal. environment.

Risks from Dividend Recapitalization

Although dividend recapitalization is beneficial to shareholders who can recover their initial investments, it can also be dangerous for the company that undergoes the process. As a company increases its leverage, there is a higher probability of default on its financial obligations. Therefore, the recapitalization may potentially lead to financial distress and, ultimately, to bankruptcy.

Because of the increased financial risk involved, creditors and shareholders who are not entitled to receiving a special dividend (e.g., common shareholders) generally do not favor the practice. It leaves the company more vulnerable to unforeseen business problems and adverse market conditions. In addition, the company’s credit rating may decrease.

Therefore, private equity firms usually undertake thorough due diligenceDue DiligenceDue diligence is a process of verification, investigation, or audit of a potential deal or investment opportunity to confirm all relevant facts and financial information, and to verify anything else that was brought up during an M&A deal or investment process. Due diligence is completed before a deal closes. to ensure that the company is suitable for dividend recapitalization and possesses sufficient capacity to take on more debt on its balance sheet. Insolvency tests, such as the balance sheet test or cash flow test, are commonly included in the due diligence process.

Practical Example of Dividend Recapitalization

Imagine Company A that is owned by PE Capital Partners, a private equity firm. Company A is a leveraged company, with $50 million in debt and $50 million in equity. PE Capital Partners is wanting to recoup its initial investment in Company A without losing its stake in the company. Thus, the private equity firm decides to undertake a dividend recapitalization of Company A.

The dividend recapitalization plan includes the issuance of corporate bonds in the amount of $25 million. After the issuance of the new bonds, the proceeds are used to distribute special dividends to investors who participated in the initial financing of the company.

Related Readings

CFI offers the Financial Modeling & Valuation Analyst (FMVA)™Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program for those looking to take their careers to the next level. To keep learning and advancing your career, the following CFI resources will be helpful:

- Accelerated DividendAccelerated DividendAn accelerated dividend is a dividend that is paid out ahead of a change in the way the dividends are treated, such as a change in the tax rate of dividends. The dividend payments are made early in order to protect shareholders and mitigate the negative impact that a change in dividend policy brings about.

- Capital StructureCapital StructureCapital structure refers to the amount of debt and/or equity employed by a firm to fund its operations and finance its assets. A firm's capital structure

- Common StockCommon StockCommon stock is a type of security that represents ownership of equity in a company. There are other terms – such as common share, ordinary share, or voting share – that are equivalent to common stock.

- Leverage RatiosLeverage RatiosA leverage ratio indicates the level of debt incurred by a business entity against several other accounts in its balance sheet, income statement, or cash flow statement. Excel template

-

Understanding Financial Gearing: Debt & Leverage Explained

Gearing is the amount of debtNet DebtNet debt = total debt - cash. Net debt is a financial liquidity metric that measures a company’s ability to pay all its debts if they were due today. Compare

-

Leverage in Finance: Strategies, Types & Risks

In finance, leverage is a strategy that companies use to increase assets, cash flows, and returns, though it can also magnify losses. There are two main types of leverage: financial and operating. To

Business strategy

- Understanding Dividend Yield: A Key Metric for Investors

- Understanding Forward Dividend Yield: A Key Metric for Investors

- Understanding Liquidating Dividends: A Comprehensive Guide

- Recapitalization: Definition, Types & Benefits | [Your Company Name]

- Special Dividends: Understanding One-Time Distributions

- Understanding Dividend Policy: A Comprehensive Guide

- Holding Companies: Definition, Purpose & How They Work

- Kaizen: Understanding Continuous Improvement for Business

- Outsourcing: A Comprehensive Guide to Benefits & Strategy

-

Understanding Clawbacks: Protecting Stakeholders from Failed Performance

Understanding Clawbacks: Protecting Stakeholders from Failed PerformanceWhat happens when a person promises to perform and then fails to deliver on their promises? Or what happens when it is found that a performance reportDue Diligence ReportExample due diligence report o...

-

Understanding Dividends: A Comprehensive Guide

Understanding Dividends: A Comprehensive GuideA dividend is a share of profits and retained earningsRetained EarningsThe Retained Earnings formula represents all accumulated net income netted by all dividends paid to shareholders. Retained Earnin...