Special Dividends: Understanding One-Time Distributions

A special dividend, also referred to as an extra dividend, is a non-recurring, “one-time” dividend distributed by a company to its shareholders. It is separate from the regular cycle of dividends and is usually abnormally larger than a company’s typical dividend payment.

Special dividends are typically declared after exceptionally strong company earnings, the sale of a subsidiary or business unit, a business spin-offSpin-OffA corporate spin-off is an operational strategy used by a company to create a new business subsidiary from its parent company. , or after achieving a company milestone.

Reasons for Paying a Special Dividend

A company pays out a special dividend for the following reasons:

1. Distributing extra cash available on the balance sheet

When there is a lot of cash available on a company’s balance sheetBalance SheetThe balance sheet is one of the three fundamental financial statements. The financial statements are key to both financial modeling and accounting. and it does not decide to reinvest the cash back into the business, the company may choose to distribute the cash in the form of a special dividend.

A prominent example is Microsoft’s special, one-time dividend of $3 a share in July 2004, valued at a total payout worth $32 billion.

2. Altering a company’s financial structure

Recall the accounting equation, Assets = Liabilities + Shareholders Equity. A special dividend can be used to alter a company’s capital structureCapital StructureCapital structure refers to the amount of debt and/or equity employed by a firm to fund its operations and finance its assets. A firm's capital structure by reducing equity and assets. By paying a special dividend, the company is altering the percentage of debt vs. the percentage of equity used to finance the company.

3. Instilling confidence in long-term value generation

Special dividends can be used by a company to show confidence in its long-term value generation and to improve shareholder confidence. When shareholders receive extra cash in the form of a special dividend, they are more likely to stick with the company for the long term.

4. A hybrid dividend policy – Cyclical companies

Companies may use a special dividend in conjunction with their regular dividend policy to form a hybrid dividend policy. This can be seen with cyclical companies where they are largely affected by the economic outlook.

Cyclical companies may follow a normal dividend cycle and also declare a special dividend when the company is performing better than normal. This is considered a better practice than increasing the dividend rate during economic booms and decreasing the rate during economic recessions, which may send mixed signals to investors.

Potential Disadvantages

There are possible disadvantages to consider when declaring a special dividend:

1. Perceived lack of investment opportunities

A special dividend can be seen by investors as the company finding no better use for its cash reserves. In other words, investors may see the company facing a lack of reinvestment opportunities. This may have a negative impact on the company’s stock price as investors may believe its growth potential is decreasing.

2. Opportunity cost

Companies may declare a special dividend only to realize that they do not have enough cash to fund future projects. Therefore, the opportunity costOpportunity CostOpportunity cost is one of the key concepts in the study of economics and is prevalent throughout various decision-making processes. The of declaring a special dividend is high.

For example, consider a company that distributes its cash as a special dividend to investors. If an attractive investment opportunity were then to arise, the company might not have enough cash on its balance sheet to fund the project.

Impact of a Special Dividend on Share Price

Special dividends exert the same effect as a cash dividend on share prices. For example, consider a stock that is currently trading at $100 one day before the ex-dividend dateEx-Dividend DateThe ex-dividend date is an investment term that determines which stockholders are eligible to receive declared dividends. When a company announces a dividend, the board of directors set a record date when only shareholders recorded on the company’s books as of that date are entitled to receive the dividends.. The special dividend declared is $20 per share.

Theoretically, on the ex-dividend date, the stock should decrease by $20 and trade at $80. With that said, the stock might actually be higher or lower than $80 on the ex-dividend date, depending on investor sentiment regarding the special dividend.

Journal Entries for a Special Dividend

The journal entries for a special dividend are the same as for a regular cash dividend.

Consider a company that declares, on January 1, a special dividend of $1 per share on the 5,000 shares currently outstanding. The dividends are payable on February 1 to shareholders of record as of January 15.

Special dividends payable are $5,000 (5,000 x $1), and the journal entries are as follows:

Related Readings

CFI is the official provider of the global Financial Modeling & Valuation Analyst (FMVA)™Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful:

- Accelerated DividendAccelerated DividendAn accelerated dividend is a dividend that is paid out ahead of a change in the way the dividends are treated, such as a change in the tax rate of dividends. The dividend payments are made early in order to protect shareholders and mitigate the negative impact that a change in dividend policy brings about.

- Cost of EquityCost of EquityCost of Equity is the rate of return a shareholder requires for investing in a business. The rate of return required is based on the level of risk associated with the investment

- Dividend Payout RatioDividend Payout RatioDividend Payout Ratio is the amount of dividends paid to shareholders in relation to the total amount of net income generated by a company. Formula, example

- Dividend Reinvestment Plan (DRIP)Dividend Reinvestment Plan (DRIP)A dividend reinvestment plan (DRIP or DRP) is a plan offered by a company to shareholders that it allows them to automatically reinvest their

-

Dividend Payout Ratio (DPR): Understanding & Calculation

The Dividend Payout Ratio (DPR) is the amount of dividends paid to shareholders in relation to the total amount of net incomeNet IncomeNet Income is a key line item, not only in the income statement,

-

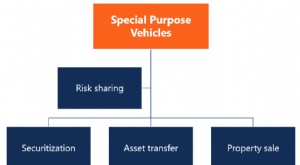

Special Purpose Vehicles (SPVs): Definition, Types & Assets

A Special Purpose Vehicle (SPV) is a separate legal entity created by an organization. The SPV is a distinct company with its own assetsTypes of AssetsCommon types of assets include current, non-curre

finance

- Understanding Dividend Per Share (DPS): A Comprehensive Guide

- Understanding Dividend Yield: A Key Metric for Investors

- DRIP (Dividend Reinvestment Plan): A Comprehensive Guide for Investors

- Understanding Forward Dividend Yield: A Key Metric for Investors

- Understanding Liquidating Dividends: A Comprehensive Guide

- Understanding Stable Dividend Policies: A Comprehensive Guide

- Understanding Dividend Policy: A Comprehensive Guide

- Dividend Recapitalization: Definition & How It Works

- Special Dividends: Understanding One-Time Payments to Shareholders

-

Dividend Irrelevance Theory: Understanding Its Implications

Dividend Irrelevance Theory: Understanding Its ImplicationsDividend Irrelevance Theory is a financial theory that claims that the issuing of dividends does not increase a company’s potential profitability or its stock price. It suggests that invest...

-

Stock Dividends: Definition, Types & How They Work

Stock Dividends: Definition, Types & How They WorkA stock dividend, a method used by companies to distribute wealth to shareholders, is a dividend payment made in the form of shares rather than cash. Stock dividends are primarily issued in lieu of ca...