Understanding Debt Default: Causes, Consequences, and Prevention

A debt default happens when a borrower fails to pay his or her loan at the time it is due. The time a default happens varies, depending on the termsDebt CovenantsDebt covenants are restrictions that lenders (creditors, debt holders, investors) put on lending agreements to limit the actions of the borrower (debtor). agreed upon by the creditor and the borrower. Some loans default after missing one payment, while others default only after three or more payments are missed. In such an event, serious repercussions can happen, such as getting a poor credit ratingFICO ScoreA FICO score, more commonly known as a credit score, is a three-digit number that is used to assess how likely a person is to repay the credit if the individual is given a credit card or if a lender loans them money. FICO scores are also used to help determine the interest rate on any credit extended.

Debt default notice

Before a debt becomes in default, a notice of debt default is sent by the creditor to the borrower, stating how far behind the debtor is in his or her payments, as well as how much is needed to get the payments updated. Usually, the notice gives the debtor about two weeks to cover the missed payments. Otherwise, the debt will default.

Debt default on secured loans and unsecured loans

A debt default on a secured loan means repossession of the collateral. For example, a person who defaults on a car loan will need to surrender the car to the creditor, just as somebody who defaults on a home equity loanMortgageA mortgage is a loan – provided by a mortgage lender or a bank – that enables an individual to purchase a home. While it’s possible to take out loans to cover the entire cost of a home, it’s more common to secure a loan for about 80% of the home’s value. must face foreclosure of the house.

However, for defaults on unsecured loans without collateral, such as credit card purchases, the borrower is typically given a grace period of, for example, 30 to 60 days. During this period, the borrower needs to make the required payments or risk having his account referred to the company’s collections department, which will then change the account’s status to default.

When this happens, the creditor may sell the default account to a third-party collector who will take over the collecting of the fees, and who may even charge higher fees to get their cut from the debt. If at this stage, still no payment is made, the third party may bring the matter to a lawyer’s office. The attorney may take the borrower to court if the debt is still not settled.

What happens in a debt default

A debt default comes with consequences that can have lasting effects on the borrower’s reputation and credit score. Credit represents an individual’s ability to borrow money. When an individual applies for a loan, whether secured or unsecured, the creditor looks at the person’s credit score because it helps determine if the person is likely to be able to pay back the loan and its interestInterest ExpenseInterest expense arises out of a company that finances through debt or capital leases. Interest is found in the income statement, but can also.

Here are other things that happen in a debt default:

#1 Annoying collectors

This is one of the most disturbing things that occur in a debt default. After receiving the debt default notice and still failing to make payments, a third-party collector will bombard the borrower with calls to get the payments. They can even come to the point of going to the borrower’s workplace, which often causes embarrassment.

#2 Legal problems

If a debt defaults and no settlement is reached despite negotiations, the collections department may secure a lawyer’s services that will send the final written notice of collection to the borrower. After all other means of collecting the debt have been exhausted, the law office may pursue a case against the borrower.

#3 More fees to pay

The irony of a debt default is that when a borrower fails to pay his dues because of financial difficulty, that actually leads to incurring more fees that need to be paid.

How to avoid a debt default

Debt defaults can often be avoided if the borrower takes the issue seriously and handles o.

#1 Acceptance

The first step to avoiding a debt default is acceptance. What needs to be accepted is the fact that debt was incurred because of the lack of sufficient funds. Now, if a debtor defaults, how would he be able to pay the loan, plus all the penalties and fees?

#2 Follow a budget

Working and living on a budget should not be seen as depriving oneself of the pleasures of life, but merely as living within one’s means. A budget must be prepared each month, setting aside a specific amount of money for each category of expenses, such as groceries, utility bills, insurance, and others. Sticking to the budget is the key.

#3 Track debts

Tracking debts is especially useful for people who have more than one debt. It can help to create a single form that details every type of debt, the individual due dates, and the amount due for each. Place the debt tracking list in a strategic and secure location.

#4 Ask for help from the family

Debts have to be dealt with by the entire family, not just by one member. Though involving the kids and letting them know of these debts is discouraged, the husband and wife should help each other in keeping track of debts.

CommunicationCommunicationBeing able to communicate effectively is one of the most important life skills to learn. Communication is defined as transferring information to produce greater understanding. It can be done vocally (through verbal exchanges), through written media (books, websites, and magazines), visually (using graphs, charts, and maps) or non-verbally is not only for the husband and the wife but also between the couple and the creditor. If there is a likely chance that a payment will be missed, it will help to contact the creditor as soon as you are aware of a possible problem. Explain your situation and ask for a little leeway, with a promise to bring the payments current as soon as possible.

More resources

CFI is the official provider of the global Financial Modeling & Valuation Analyst (FMVA)™Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful:

- Accounts PayableAccounts PayableAccounts payable is a liability incurred when an organization receives goods or services from its suppliers on credit. Accounts payables are

- Peer-to-Peer LendingPeer-to-Peer LendingPeer-to-peer lending is a form of direct lending of money to individuals or businesses without an official financial institution participating as an intermediary in the deal. P2P lending is generally done through online platforms that match lenders with the potential borrowers.

- Revolver DebtRevolver DebtRevolver debt is a form of credit that differs from installment loans. In revolver debt, the borrower has constant credit access up to the maximum

- Trade CreditTrade CreditA trade credit is an agreement or understanding between agents engaged in business with each other that allows the exchange of goods and services

-

Default Risk Premium: Understanding & Calculation

A default risk premium is effectively the difference between a debt instrument’s interest rate and the risk-free rateRisk-Free RateThe risk-free rate of return is the interest rate an investor c

-

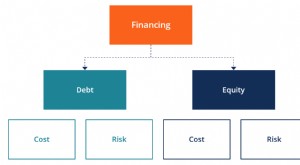

Understanding Business Financing: A Comprehensive Guide

Financing refers to the methods and types of funding a business uses to sustain and grow its operations. It consists of debtSenior and Subordinated DebtIn order to understand senior and subordinated d

finance

- Understanding Capital: Types, Categories & Value Creation

- Understanding Debt: Types, Obligations & Financial Implications

- Understanding Debt Capacity: A Guide for Businesses

- Debt Consolidation: Simplify Payments & Lower Interest Rates

- Debt Financing: A Comprehensive Guide for Businesses

- Debt Refinancing: A Comprehensive Guide to Lowering Your Payments

- Debt Restructuring: A Comprehensive Guide for Financial Distress

- Debt Settlement: Definition, How It Works & Is It Right For You?

- Unitranche Debt Explained: Structure, Benefits & Risks

-

Coverage Ratio: Understanding Your Company's Debt Repayment Ability

Coverage Ratio: Understanding Your Company's Debt Repayment AbilityA Coverage Ratio is any one of a group of financial ratios used to measure a company’s ability to pay its financial obligationsDebt CapacityDebt capacity refers to the total amount of debt a bus...

-

Understanding Credit Events: A Guide for Investors

Understanding Credit Events: A Guide for InvestorsA credit event refers to a negative change in the credit standing of a borrower that triggers a contingent payment in a credit default swap (CDS). It occurs when an individual or organization defaults...