Exit Multiple Explained: Business Valuation & Terminal Value

An exit multiple is one of the methods used to calculate the terminal value in a discounted cash flow formula to value a business. The method assumes that the value of a business can be determined at the end of a projected period, based on the existing public market valuations of comparable companies. The most commonly used multiples are EV/EBITDAEV/EBITDAEV/EBITDA is used in valuation to compare the value of similar businesses by evaluating their Enterprise Value (EV) to EBITDA multiple relative to an average. In this guide, we will break down the EV/EBTIDA multiple into its various components, and walk you through how to calculate it step by step and EV/EBITEV/EBIT RatioThe enterprise value to earnings before interest and taxes (EV/EBIT) ratio is a metric used to determine if a stock is priced too high or too low.

Analysts use exit multiples to estimate the value of a company by multiplying financial metrics such as EBIT EBIT GuideEBIT stands for Earnings Before Interest and Taxes and is one of the last subtotals in the income statement before net income. EBIT is also sometimes referred to as operating income and is called this because it's found by deducting all operating expenses (production and non-production costs) from sales revenue.and EBITDAEBITDAEBITDA or Earnings Before Interest, Tax, Depreciation, Amortization is a company's profits before any of these net deductions are made. EBITDA focuses on the operating decisions of a business because it looks at the business’ profitability from core operations before the impact of capital structure. Formula, examples by a factor that is similar to that of recently acquired companies. Exit multiple is sometimes referred to as terminal exit value.

What is Terminal Value?

Terminal value refers to the value of a project or business at a future point in time beyond the explicit forecast period. Instead, it assumes that the growth rates of all future cash flows are consistent and stable beyond the forecast period. Terminal value is typically a large portion (>50%) of the total assessed value and is therefore very important.

Terminal value addresses such limitations by allowing the inclusion of future cash flow values beyond the projection period while mitigating any issues that may arise from using the values of such cash flows.

Using Discounted Cash Flows Method to Determine Terminal Value

When estimating a company’s cash flows in the future, analysts use financial models such as the discounted cash flow (DCF)Discounted Cash Flow DCF FormulaThis article breaks down the DCF formula into simple terms with examples and a video of the calculation. Learn to determine the value of a business. method combined with certain assumptions to arrive at the value of the business. The DCF method assumes that the asset value equals the future cash flows generated by that asset.

The discounted cash flow method comprises two main components, i.e., the forecast period and terminal value. The forecast period is used when estimating the value of a company or asset for a period of about three to five years.

Using the forecast period to determine the value of a company for a period exceeding five years will cast doubt on the accuracy of the valuation obtained. Using terminal value to find the value of a company or asset attempts to solve this uncertainty. There are two approaches to calculating terminal values: Exit Multiple and Perpetual Growth method.

Calculating Terminal Value Using Exit Multiple

The exit multiple uses a market multiple basis to fairly value a business. The value of the business is obtained by multiplying financial metrics such as EBITDA or EBIT by a factor obtained from comparable companies that were recently acquired. An appropriate range of multiples can be generated by looking at recent comparable acquisitions in the public market.

The multiple obtained is then multiplied by the projected EBIT or EBITDA in year N (final year of projection period) to give the future value at the end of year N. The future value (also known as terminal value) is then discounted back using a company’s Weighted Average Cost of Capital.

The value obtained is then added to the present value of the free cash flows to obtain the implied enterprise valueEnterprise Value (EV)Enterprise Value, or Firm Value, is the entire value of a firm equal to its equity value, plus net debt, plus any minority interest. For cyclical businesses where earnings fluctuate according to variations in the economy, we use the average EBITDA or EBIT during the course of the specific cyclical rather than the amount in year N in the projection period.

This means that an industry multiple is applied rather than applying a current multiple to take into account the cyclical variations of earnings. If analysts used a current multiple, the valuation would be affected by economic cycles.

Perpetual Growth Method

The perpetual growth method is an alternative to the exit multiple method, and it accounts for the free cash flows of a business that grow at a steady rate in perpetuity. It assumes that cash will grow at a stable rate forever, starting from a specific point in the future.

While it is nearly impossible for a company to grow at the same rate for an infinite period in the future, the perpetual growth method is preferred to calculating the terminal value because it is based on the historical performance of the company.

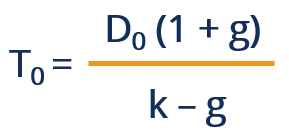

Compared to the exit multiple method, the perpetual growth method generates a higher terminal value. The formula for calculating the terminal value using the perpetual growth method is as follows:

Where:

- D0 represents the cash flows at a future period that is prior to N+1 or towards the end of period N.

- k represents the discount rate

- g represents the constant growth rate

Additional Resources

CFI is the official provider of the global Financial Modeling & Valuation Analyst (FMVA)®Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful:

- Comparable Company AnalysisComparable Company AnalysisThis guide shows you step-by-step how to build comparable company analysis ("Comps") and includes a free template and many examples.

- EBIT vs. EBITDAEBIT vs EBITDAEBIT vs EBITDA - two very common metrics used in finance and company valuation. There are important differences, pros/cons to understand.

- Entry MultipleEntry MultipleAn entry multiple, commonly used in leveraged buyouts, refers to the price paid for a company as a function of a financial metric.

- Types of Valuation MultiplesTypes of Valuation MultiplesThere are many types of valuation multiples used in financial analysis. They can be categorized as equity multiples and enterprise value multiples.

-

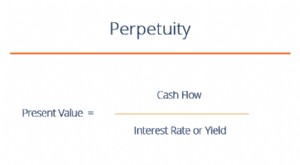

Perpetuity Explained: Understanding Infinite Cash Flows

Perpetuity in the financial system is a situation where a stream of cash flowValuationFree valuation guides to learn the most important concepts at your own pace. These articles will teach you busines

-

Understanding Value at Risk (VaR): A Comprehensive Guide

Value of risk refers to the financial benefit that an organization will gain for pursuing a risk-taking activity. Businesses undertake different activities all the time – such as starting a new

finance

- Compound Annual Growth Rate (CAGR): Definition & Calculation

- Understanding Financial Denomination: A Comprehensive Guide

- Understanding Equity: A Comprehensive Guide for Investors

- Face Value Explained: Definition, Examples & Importance

- Understanding Fair Value: Definition & Importance

- Understanding Money: Definition, History & Value

- Nominal Value Explained: Definition & Financial Significance

- Understanding Value Added: Definition & Business Applications

- What is Value Date?

-

Market Value vs. Investment Value: Understanding the Key Differences

Market Value vs. Investment Value: Understanding the Key DifferencesIn finance, you frequently encounter the concepts of market value vs investment value. The two terms may seem synonymous, however, there are some critical differences between them. In this article, we...

-

Understanding P/FFO: A Key REIT Valuation Metric

Understanding P/FFO: A Key REIT Valuation MetricP/FFO, or Price to Funds From Operations, can be described as a reliable and modern way of determining the value of a Real Estate Investment Trust (REIT)Private REITs vs Publicly Traded REITsPrivate R...