Fama-French Three-Factor Model: Understanding Stock Returns

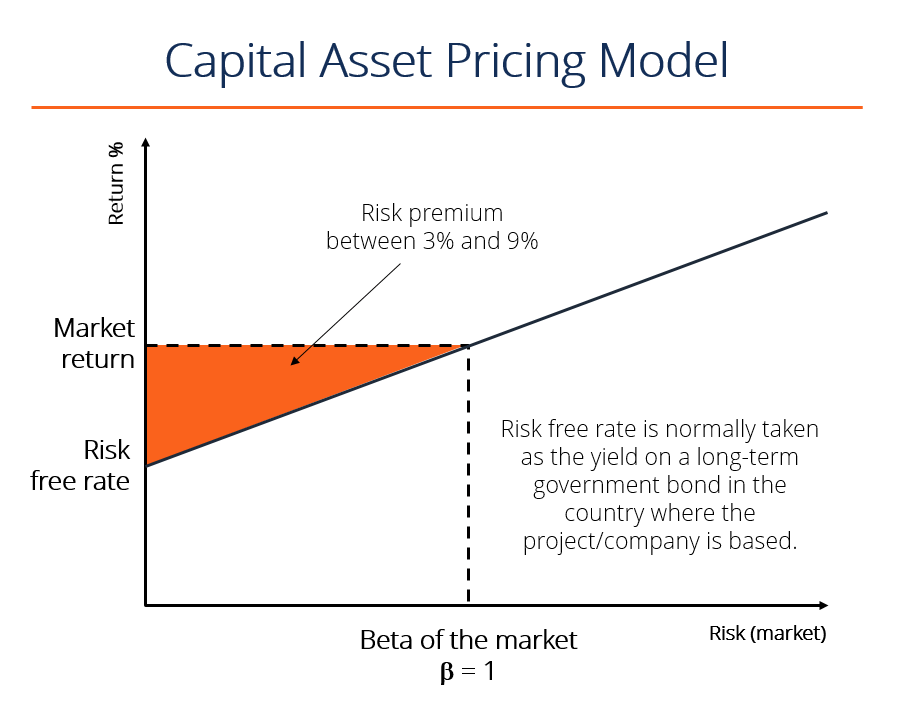

The Fama-French Three-factor Model is an extension of the Capital Asset Pricing Model (CAPM)Capital Asset Pricing Model (CAPM)The Capital Asset Pricing Model (CAPM) is a model that describes the relationship between expected return and risk of a security. CAPM formula shows the return of a security is equal to the risk-free return plus a risk premium, based on the beta of that security. The Fama-French model aims to describe stock returns through three factors: (1) market risk, (2) the outperformance of small-cap companiesSmall Cap StockA small cap stock is a stock of a publicly traded company whose market capitalization ranges from $300 million to approximately $2 billion. relative to large-cap companies, and (3) the outperformance of high book-to-market value companies versus low book-to-market value companies. The rationale behind the model is that high value and small-cap companies tend to regularly outperform the overall market.

The Fama-French three-factor model was developed by University of Chicago professors Eugene Fama and Kenneth French.

In the original model, the factors were specific to four countries: the U.S., Canada, Japan, and the U.K. Subsequently, Fama and French adjusted the factors, making them applicable for other regions, including Europe and the Asia-Pacific region.

The Fama-French Three-Factor Model Formula

The mathematical representation of the Fama-French three-factor model is:

Where:

- r = Expected rate of return

- rf = Risk-free rate

- ß = Factor’s coefficient (sensitivity)

- (rm – rf) = Market risk premium

- SMB (Small Minus Big) = Historic excess returns of small-cap companies over large-cap companies

- HML (High Minus Low) = Historic excess returns of value stocks (high book-to-price ratio) over growth stocks (low book-to-price ratio)

- ↋ = Risk

#1 Market Risk Premium

Market risk premium is the difference between the expected return of the market and the risk-free rate. It provides an investor with an excess return as compensation for the additional volatility of returns over and above the risk-free rate.

#2 SMB (Small Minus Big)

Small Minus Big (SMB) is a size effect based on the market capitalization of a company. SMB measures the historic excess of small-cap companies over big-cap companies. Once SMB is identified, its beta coefficient (β) can be determined via linear regression. A beta coefficientBeta CoefficientThe Beta coefficient is a measure of sensitivity or correlation of a security or an investment portfolio to movements in the overall market. can take positive values, as well as negative ones.

The main rationale behind this factor is that, in the long-term, small-cap companies tend to see higher returns than large-cap companies.

#3 HML (High Minus Low)

High Minus Low (HML) is a value premium. It represents the spread in returns between companies with a high book-to-market value ratio (value companies) and companies with a low book-to-market value ratio. Like the SMB factor, once the HML factor is determined, its beta coefficient can be found by linear regression. The HML beta coefficient can also take positive or negative values.

The HML factor reveals that, in the long-term, value stocks (high book-to-market ratio) enjoy higher returns than growth stocks (low book-to-market ratio).

Importance of the Fama-French Three-factor Model

The Fama-French three-factor model is an expansion of the Capital Asset Pricing Model (CAPM)Capital Asset Pricing Model (CAPM)The Capital Asset Pricing Model (CAPM) is a model that describes the relationship between expected return and risk of a security. CAPM formula shows the return of a security is equal to the risk-free return plus a risk premium, based on the beta of that security. The model is adjusted for outperformance tendencies. Also, two extra risk factors make the model more flexible relative to CAPM.

According to the Fama-French three-factor model, over the long-term, small companies overperform large companies, and value companies beat growth companies. The studies conducted by Fama and French revealed that the model could explain more than 90% of diversified portfolios’ returns. Similar to the CAPM, the three-factor model is designed based on the assumption that riskier investments require higher returns.

Nowadays, there are further extensions to the Fama-French three-factor model, such as the four-factor and five-factor models.

Related Readings

CFI offers the Financial Modeling & Valuation Analyst (FMVA)™Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program for those looking to take their careers to the next level. To keep learning and advancing your career, the following CFI resources will be helpful:

- Comparable Company AnalysisComparable Company AnalysisThis guide shows you step-by-step how to build comparable company analysis ("Comps") and includes a free template and many examples.

- Market CapitalizationMarket CapitalizationMarket Capitalization (Market Cap) is the most recent market value of a company’s outstanding shares. Market Cap is equal to the current share price multiplied by the number of shares outstanding. The investing community often uses the market capitalization value to rank companies

- Market to Book RatioMarket to Book RatioThe Market to Book Ratio, or Price to Book Ratio, is used to compare the current market value or price of a business to its book value of equity on the balance sheet.

- Valuation MethodsValuation MethodsWhen valuing a company as a going concern there are three main valuation methods used: DCF analysis, comparable companies, and precedent transactions

-

Current Ratio: Definition, Calculation & Financial Health

The current ratio, also known as the working capitalNet Working CapitalNet Working Capital (NWC) is the difference between a companys current assets (net of cash) and current liabilities (net of debt)

-

Understanding the S&P/TSX Composite Index: A Comprehensive Guide

TSX is short for the Toronto Stock Exchange, Canada’s primary exchange, and the 9th largest stock exchange in the world, based on the market capitalization of its companies. S&P stands for Standar

finance

- The Financial Modeler's Manifesto: Principles for Robust Financial Modeling

- PRAT Model: Understanding Sustainable Growth & Financial Health

- Understanding the S&P Sectors: A Comprehensive Guide

- Black-Scholes Model: Understanding Stock Option Pricing

- Understanding the Heath-Jarrow-Morton (HJM) Interest Rate Model

- Heston Model: Understanding Volatility in Financial Options

- NASDAQ-100 Index: Definition, Components & Historical Data

- McKinsey 7S Model: Understanding Organizational Effectiveness

- Dow Jones Industrial Average (DJIA): A Comprehensive Overview

-

NEX Exchange: Understanding Canada's Alternative Trading Platform

NEX Exchange: Understanding Canada's Alternative Trading PlatformThe NEX trading platform – typically referred to as the NEX Exchange – is a subset of the TSX Venture Exchange in Canada. Companies that do not qualify to be listed on the TSX Venture Exch...

-

Porter's Five Forces: A Comprehensive Guide to Competitive Analysis

Porter's Five Forces: A Comprehensive Guide to Competitive AnalysisThe Competitive Forces Model is an important tool used in strategic analysisStrategic AnalysisStrategic analysis refers to the process of conducting research on a company and its operating environment...