Understanding the Heath-Jarrow-Morton (HJM) Interest Rate Model

The Heath-Jarrow-Morton Model – also known as the HJM Model – is a framework to represent forward interest rates using an existing term structure of interest rates. The model was created based on the work developed by David Heath, Robert A. Jarrow, and Andrew Morton during the late 1980s. Their research papers led to the establishment of the model that we know today.

The purpose of using the HJM Model is to predict forward interest rates so that the predictions can be used to calculate the prices of securities affected by interest rate movements, including securities such as bonds and optionsOptions: Calls and PutsAn option is a derivative contract that gives the holder the right, but not the obligation, to buy or sell an asset by a certain date at a specified price..

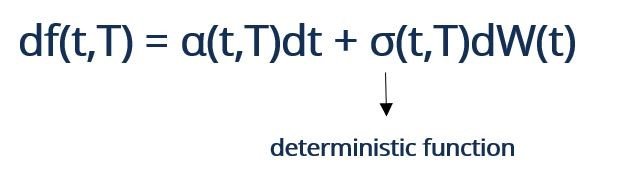

The model can be mathematically represented by the following general formula:

Where:

- α and σ are adapted

- W is a Brownian motion under the assumption of being risk-neutral

- df(t,T) represents the instantaneous forward interest rate with maturity at time T

Assumptions of the Heath-Jarrow-Morton Model

There are several assumptions presented by the Heath-Jarrow-Morton Model, such as:

- The model assumes that the forward rate is driven by volatility because the volatility in the market for futures contractsFutures ContractA futures contract is an agreement to buy or sell an underlying asset at a later date for a predetermined price. It’s also known as a derivative because future contracts derive their value from an underlying asset. Investors may purchase the right to buy or sell the underlying asset at a later date for a predetermined price. can be predicted.

- Another assumption presented by the model is that the price of each security is observable. The security can be bought and sold at any quantity at the observed price.

- The model does not explain all the complexities that come from a changing term structure.

Uses of the Heath-Jarrow-Morton Model

Investors use the Heath-Jarrow-Morton Mode to determine the prices of securities that are impacted by interest rate fluctuations. By being able to price securities, investors can engage in arbitrage opportunitiesArbitrageArbitrage is the strategy of taking advantage of price differences in different markets for the same asset. For it to take place, there must be a situation of at least two equivalent assets with differing prices. In essence, arbitrage is a situation that a trader can profit from to earn a riskless profit if there are differences between the price of the security in the market and the price of the security calculated based on the Heath-Jarrow-Morton Model.

In particular, the model can be used to price financial derivatives because the value of derivatives depends on the term structure of underlying assets. For example, the underlying asset for credit derivatives is the price of risky zero-coupon bonds. In addition to arbitrage seekers, it can also be used by asset-liability management.

The Gaussian Heath-Jarrow-Morton Model and Short-Rate Models

When the drift and volatilityVolatilityVolatility is a measure of the rate of fluctuations in the price of a security over time. It indicates the level of risk associated with the price changes of a security. Investors and traders calculate the volatility of a security to assess past variations in the prices of the instantaneous forward rate are assumed to be deterministic, it is known as the Gaussian Heath-Jarrow-Morton Model. In the mathematical formula, it is when σ becomes a deterministic function.

The Heath-Jarrow-Morton Model is often compared with other models when investors assess different strategies to price financial derivatives. They are often compared with short-rate models, but they are different from each other. The HJM Model represents the entire forward rate curve, but short-rate models only demonstrate a specific point on the curve.

Learn More

CFI offers the Commercial Banking & Credit Analyst (CBCA)™Program Page - CBCAGet CFI's CBCA™ certification and become a Commercial Banking & Credit Analyst. Enroll and advance your career with our certification programs and courses. certification program for those looking to take their careers to the next level. To keep learning and developing your knowledge base, please explore the additional relevant resources below:

- Capital MarketsCapital MarketsCapital markets are the exchange system platform that transfers capital from investors who want to employ their excess capital to businesses

- Short Rate ModelShort Rate ModelA short rate model is a mathematical model used in the evaluation of interest rate derivatives to illustrate the evolution of interest rates over time by

- Interest Rate FuturesInterest Rate FuturesInterest rate futures are futures contracts with the an interest-bearing security as the underlying asset. They can be used for speculation or hedging.

- Volatility Quote TradingVolatility Quote TradingVolatility quote trading is a form of investment that focuses on the volatility that a security is estimated to experience in the future

-

Understanding Divergence in Technical Analysis: A Guide

Divergence is when the asset price moves in the direction opposite to what a technical indicator indicates. When a stock is diverging, it signals weaker price trends and the beginning of a reversal.&n

-

Dow 30 Explained: Understanding the Dow Jones Industrial Average

The Dow 30, or Dow Jones Industrial Average, is a stock index that tracks the performance of the 30 biggest companies listed on the stock indices in the United States. Despite being used by analysts t

invest

- Understanding Silver Price Fluctuations: Key Factors & Trends

- Black-Scholes Model: Understanding Stock Option Pricing

- Double Top Pattern: Definition, Trading Signals & Analysis

- Understanding the Forward Curve: A Comprehensive Guide

- Heston Model: Understanding Volatility in Financial Options

- Understanding Market Support: What is 'Holding the Market'?

- Understanding Offering Price: A Guide for Investors

- Understanding Quoted Prices: A Comprehensive Guide

- Understanding Strike Price: Options Trading Explained

-

Backtesting: A Comprehensive Guide to Strategy Validation

Backtesting: A Comprehensive Guide to Strategy ValidationBacktesting involves applying a strategy or predictive model to historical data to determine its accuracy. It can be used to test and compare the viability of trading strategies so tradersSix Essentia...

-

Understanding Dead Cat bounces: A Stock Market Indicator

Understanding Dead Cat bounces: A Stock Market IndicatorThe dead cat bounce describes a financial phenomenon whereby a stock in a steady decline suddenly, and without a logical cause, gains value temporarily before continuing its downward trend. The term o...