Black-Scholes Model: Understanding Stock Option Pricing

The Black-Scholes-Merton (BSM) model is a pricing model for financial instruments. It is used for the valuation of stock options. The BSM model is used to determine the fair prices of stock options based on six variables: volatilityVolatilityVolatility is a measure of the rate of fluctuations in the price of a security over time. It indicates the level of risk associated with the price changes of a security. Investors and traders calculate the volatility of a security to assess past variations in the prices, type, underlying stock price, strike priceStrike PriceThe strike price is the price at which the holder of the option can exercise the option to buy or sell an underlying security, depending on, time, and risk-free rate. It is based on the principle of hedging and focuses on eliminating risks associated with the volatility of underlying assets and stock options.

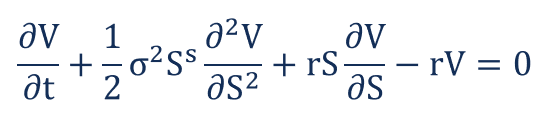

The Black-Scholes-Merton Equation

The Black-Scholes-Merton model can be described as a second order partial differential equation.

The equation describes the price of stock options over time.

Pricing a Call Option

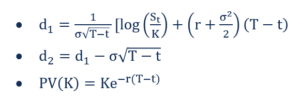

The price of a call option C is given by the following formula:

Where:

Pricing a Put Option

The price of a put option P is given by the following formula:

Where:

- N – Cumulative distribution function of the standard normal distribution. It represents a standard normal distribution with mean = 0 and standard deviation = 1

- T-t – Time to maturity (in years)

- St – Spot price of the underlying asset

- K – Strike price

- r – Risk-free rate

- Ó – Volatility of returns of the underlying asset

Assumptions of the Black-Scholes-Merton Model

- Lognormal distribution: The Black-Scholes-Merton model assumes that stock prices follow a lognormal distribution based on the principle that asset prices cannot take a negative value; they are bounded by zero.

- No dividends: The BSM model assumes that the stocks do not pay any dividends or returns.

- Expiration date: The model assumes that the options can only be exercised on its expiration or maturity date. Hence, it does not accurately price American options. It is extensively used in the European options market.

- Random walk: The stock market is a highly volatile one, and hence, a state of random walkRandom Walk TheoryThe Random Walk Theory is a mathematical model of the stock market. The theory posits that the price of securities moves randomly is assumed as the market direction can never truly be predicted.

- Frictionless market: No transaction costs, including commission and brokerage, is assumed in the BSM model.

- Risk-free interest rate: The interest rates are assumed to be constant, hence making the underlying asset a risk-free one.

- Normal distribution: Stock returns are normally distributed. It implies that the volatility of the market is constant over time.

- No arbitrage: There is no arbitrage. It avoids the opportunity of making a riskless profit.

Limitations of the Black-Scholes-Merton Model

- Limited to the European market: As mentioned earlier, the Black-Scholes-Merton model is an accurate determinant of European option prices. It does not accurately value stock options in the US. It is because it assumes that options can only be exercised on its expiration/maturity date.

- Risk-free interest rates: The BSM model assumes constant interest rates, but it is hardly ever the reality.

- Assumption of a frictionless market: Trading generally comes with transaction costs such as brokerage fees, commissionCommissionCommission refers to the compensation paid to an employee after completing a task, which is, often, selling a certain number of products or services, etc. However, the Black Scholes Merton model assumes a frictionless market, which means that there are no transaction costs. It is hardly ever the reality in the trading market.

- No returns: The BSM model assumes that there are no returns associated with the stock options. There are no dividends and no interest earnings. However, it is not the case in the actual trading market. The buying and selling of options are primarily focused on the returns.

More Resources

CFI offers the Financial Modeling & Valuation Analyst (FMVA)™Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program for those looking to take their careers to the next level. To keep learning and advancing your career, the following resources will be helpful:

- Continuously Compounded ReturnContinuously Compounded ReturnContinuously compounded return is what happens when the interest earned on an investment is calculated and reinvested back into the account for an infinite number of periods. The interest is calculated on the principal amount and the interest accumulated over the given periods

- Options: Calls and PutsOptions: Calls and PutsAn option is a derivative contract that gives the holder the right, but not the obligation, to buy or sell an asset by a certain date at a specified price.

- Risk-free RateRisk-Free RateThe risk-free rate of return is the interest rate an investor can expect to earn on an investment that carries zero risk. In practice, the risk-free rate is commonly considered to equal to the interest paid on a 3-month government Treasury bill, generally the safest investment an investor can make.

- Spot PriceSpot PriceThe spot price is the current market price of a security, currency, or commodity available to be bought/sold for immediate settlement. In other words, it is the price at which the sellers and buyers value an asset right now.

-

Understanding Divergence in Technical Analysis: A Guide

Divergence is when the asset price moves in the direction opposite to what a technical indicator indicates. When a stock is diverging, it signals weaker price trends and the beginning of a reversal.&n

-

Dow 30 Explained: Understanding the Dow Jones Industrial Average

The Dow 30, or Dow Jones Industrial Average, is a stock index that tracks the performance of the 30 biggest companies listed on the stock indices in the United States. Despite being used by analysts t

invest

- Understanding Silver Price Fluctuations: Key Factors & Trends

- Double Top Pattern: Definition, Trading Signals & Analysis

- Understanding the Forward Curve: A Comprehensive Guide

- Understanding the Heath-Jarrow-Morton (HJM) Interest Rate Model

- Heston Model: Understanding Volatility in Financial Options

- Understanding Market Support: What is 'Holding the Market'?

- Understanding Offering Price: A Guide for Investors

- Understanding Quoted Prices: A Comprehensive Guide

- Understanding Strike Price: Options Trading Explained

-

Backtesting: A Comprehensive Guide to Strategy Validation

Backtesting: A Comprehensive Guide to Strategy ValidationBacktesting involves applying a strategy or predictive model to historical data to determine its accuracy. It can be used to test and compare the viability of trading strategies so tradersSix Essentia...

-

Understanding Dead Cat bounces: A Stock Market Indicator

Understanding Dead Cat bounces: A Stock Market IndicatorThe dead cat bounce describes a financial phenomenon whereby a stock in a steady decline suddenly, and without a logical cause, gains value temporarily before continuing its downward trend. The term o...