Understanding Forfeited Shares: Causes, Consequences, and Rights

Forfeited shares often result from when investors in equity shares fail to comply with pre-specified purchase agreements or restrictions. The end result of share forfeiture is that the shareholder no longer needs to comply with the pre-specified purchase agreement or restrictions but loses the opportunity to realize gains on their equity stake.

Moreover, the shareholder will not possess the right to recover their previous expenditure on the equity. Forfeited shares are a common by-product of employee stock option plansEmployee Stock Option (ESO)An employee stock option (ESO) is a form of financial equity compensation that is offered to employees and executives by their organization.

Summary

- The end result of share forfeiture is that the shareholder no longer needs to comply with the pre-specified purchase agreement or restrictions but loses the opportunity to realize gains on their equity stake.

- The most common reason for share forfeiture is when the shareholder fails to comply with pre-specified purchase agreements or restrictions.

- There are several ways to approximate the fair value of an option – three popular ways are: (1) The Black Scholes Merton Model, (2) Lattice Model, and (3) Monte Carlo Method.

What is the Forfeiture Rate?

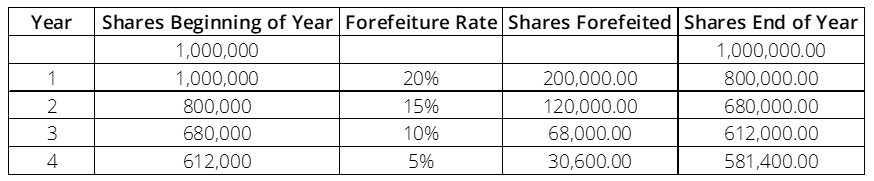

The forfeiture rate refers to the percentage of options that you expect to cancel in a year based on historical cancellation data. For every year that options are granted, you must estimate the forfeitures for the following four years. The amount of forfeitures generally trends downwards after every year.

For example, consider that you grant options for the equivalent of one million shares in 2020, and in the first year of vesting (2021), approximately 20% of the shares are forfeited. The estimated forfeiture rates from historical data of years 2, 3, and 4 are 15%, 10%, and 5%, respectively.

Therefore, at the date of options granting, the estimated shares to be forfeited in a four-year period are 200,000 + 120,000 + 68,000 + 30,600 = 418,600

The forfeiture rate is applied to the shares at the beginning of the year to calculate the number of shares forfeited. The difference between shares at the beginning of the year and shares forfeited will equal the shares at the end of the year.

The Importance of Share Forfeiture and ASC 718

When a corporation is expensing a stock option, two major steps must be followed:

- Calculating the fair value of the option

- Allocating the expense of the option over its useful economic lifeEconomic LifeEconomic life refers to the length of time an asset is expected to be useful to the owner. It is also called useful life or depreciable life

Calculating the Fair Value of an Option

The FAST defines fair value as the price that would be realizable at the sale of an asset or the amount paid to transfer a liability between market participants at the measurement date. Therefore, the fair value is the price at which the option would be purchased in an open market at the measurement date.

There are several ways to calculate an option’s fair value – a few methods include:

- The Black Scholes Merton ModelBlack-Scholes-Merton ModelThe Black-Scholes-Merton (BSM) model is a pricing model for financial instruments. It is used for the valuation of stock options.

- Lattice Model

- Monte-Carlo Method

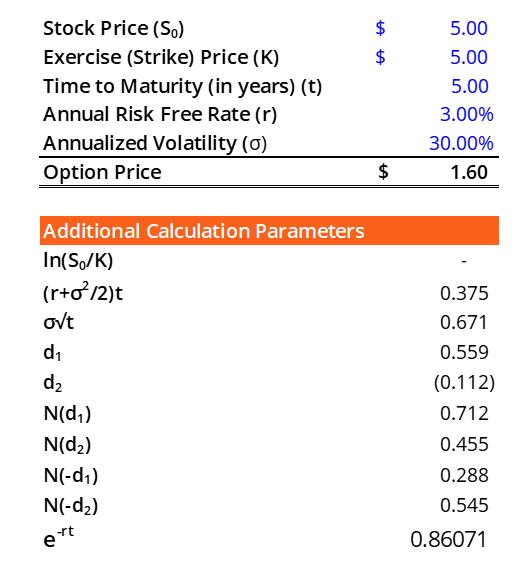

The most commonly applied method is the Black Scholes Merton Model because of its relative simplicity. In the Black Scholes Merton model, you require five inputs. The inputs are:

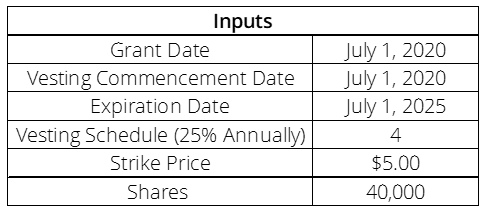

- Strike Price: The strike price is given as $5

- Share Price: The share price in our example

- Time until Expiration: The FASB introduced SAB 107, which recommends a weighting between the vesting schedule and the time to expiration. For our example, the calculation of the weighted period to expiration would be 4.

- Volatility of Underlying Security: The volatility of the underlying security is 30% over the last four years.

- Annualized Risk-Free Rate: The risk-free rate is the interest rate that you can lend money with a guaranteed return. The most popular proxy for a risk-free rate is the US Treasury Bond. However, in our case, the risk-free rate is given as 3%.

Utilizing the Black Scholes Calculator template provided by the Corporate Finance Institute found hereBlack Scholes CalculatorThis Black Scholes calculator uses to Black-Scholes option pricing method to help you calculate the fair value of a call or put option., we find that the fair value of the option is $1.60.

Allocating the Expense Over the Option’s Useful Economic Life

The next step is to find the total expense, which can be calculated as $1.60 * 40,000 = $64,000. The expense is now recorded over the useful economic life of the option grant. Here, we know that the period is 5 years. The most common way to allocate the expense is through the straight-line allocation method.

The percentage of economic life passed each year is a fifth of the total 5-year life. The proportion is applied to the total stock-based compensation expense.

Termination of Employment and the Handling of Unvested Shares

If the employee receiving stock-based compensation is terminated from their role before the shares vest, it creates complexity in financial reporting. However, expenses are not final until the options vest, but once vested, the expense is final. It is where the vested options are considered as “earned,” and the employee should be compensated because they have the right to exercise.

If an employee is terminated or leaves the company, the future stock-based compensation will not be incurred. Generally accepted accounting principles allows companies to apply a forfeiture rate – usually based on historical rates – to any expense associated with unvested shares that are being expensed.

More Resources

CFI is the official provider of the global Capital Markets & Securities Analyst (CMSA)®Program Page - CMSAEnroll in CFI's CMSA® program and become a certified Capital Markets &Securities Analyst. Advance your career with our certification programs and courses. certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful:

- Monte Carlo SimulationMonte Carlo SimulationMonte Carlo simulation is a statistical method applied in modeling the probability of different outcomes in a problem that cannot be simply solved.

- IFRS vs. US GAAPIFRS vs. US GAAPThe IFRS vs US GAAP refers to two accounting standards and principles adhered to by countries in the world in relation to financial reporting

- Strike PriceStrike PriceThe strike price is the price at which the holder of the option can exercise the option to buy or sell an underlying security, depending on

- Vesting ScheduleVesting ScheduleA vesting schedule is an incentive program established by an employer to give employees the right to certain asset classes. Employers use such type of

-

Forfeited Shares: Understanding Share Forfeiture and Consequences

What Is a Forfeited Share? A forfeited share is a share in a publicly-traded company that the owner loses (or forfeits) by neglecting to live up to any number of purchase requirements. For exam

-

Understanding Agency Costs: Protecting Shareholder Interests

Agency costs are internal costs incurred due to the competing interests of shareholders Stockholders EquityStockholders Equity (also known as Shareholders Equity) is an account on a companys balance s

finance

- A-Shares Explained: Understanding Preferred Stock & Share Classes

- Authorized Shares: Understanding a Company's Issuance Limit

- CCPPO Shares Explained: Understanding Cumulative, Convertible, & Participating Preferred Stock

- Common vs. Preferred Stock: Understanding the Differences

- Outstanding Shares: Definition & Importance for Investors

- Preferred Shares: A Comprehensive Guide for Investors

- Understanding Voting Shares: Your Right to Participate in Company Decisions

- Understanding Anti-Dilution Provisions: Protecting Investor Equity

- LEAPS Explained: Understanding Long-Term Equity Options

-

Understanding Forfeited Shares: Causes, Consequences, and Rights

Understanding Forfeited Shares: Causes, Consequences, and RightsForfeited shares often result from when investors in equity shares fail to comply with pre-specified purchase agreements or restrictions. The end result of share forfeiture is that the shareholder no ...

-

Treasury Stock: Definition, Purpose, and Implications

Treasury stocks, also known as reacquired stocks, is the portion of a previously issued stock that a company has purchased (bought back) from its shareholder. These stocks are held by the company and ...