Market Risk Premium: Definition & Calculation | Investopedia

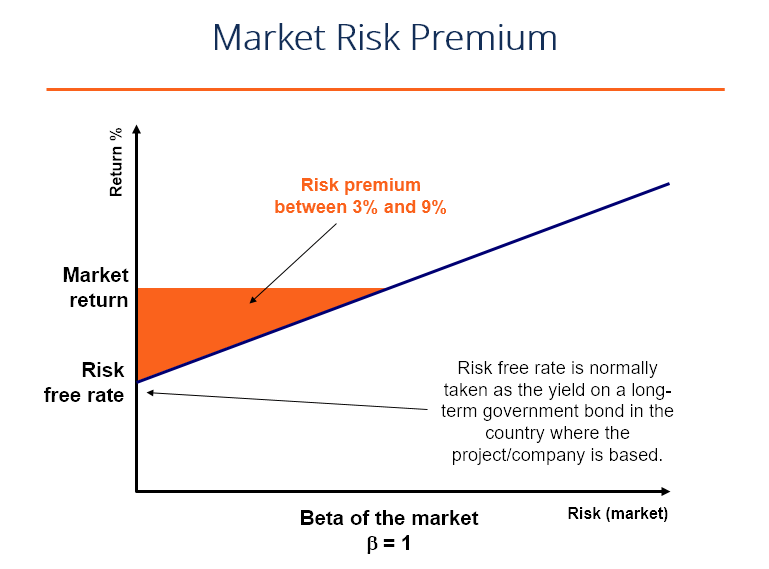

The market risk premium is the additional return an investor will receive (or expects to receive) from holding a risky market portfolio instead of risk-free assets.

The market risk premium is part of the Capital Asset Pricing Model (CAPM)Capital Asset Pricing Model (CAPM)The Capital Asset Pricing Model (CAPM) is a model that describes the relationship between expected return and risk of a security. CAPM formula shows the return of a security is equal to the risk-free return plus a risk premium, based on the beta of that security which analysts and investors use to calculate the acceptable rate of return for an investment. At the center of the CAPM is the concept of risk (volatility of returns) and reward (rate of returns). Investors always prefer to have the highest possible rate of return combined with the lowest possible volatility of returns.

Concepts Used to Determine Market Risk Premium

There are three primary concepts related to determining the premium:

- Required market risk premium – the minimum amount investors should accept. If an investment’s rate of return is lower than that of the required rate of return, then the investor will not invest. It is also called the hurdle rateHurdle Rate DefinitionA hurdle rate, which is also known as minimum acceptable rate of return (MARR), is the minimum required rate of return or target rate that investors are expecting to receive on an investment. The rate is determined by assessing the cost of capital, risks involved, current opportunities in business expansion, rates of return for similar investments, and other factors of return.

- Historical market risk premium – a measurement of the return’s past investment performance taken from an investment instrument that is used to determine the premium. The historical premium will produce the same result for all investors, as the value’s calculation is based on past performance.

- Expected market risk premium – based on the investor’s return expectation.

The required and expected market risk premiums differ from one investor to another. During the calculation, the investor needs to take the cost that it takes to acquire the investment into consideration.

With an historical market risk premium, the return will differ depending on what instrument the analyst uses. Most analysts use the S&P 500 as a benchmark for calculating past market performance.

Usually, a government bond yield is the instrument used to identify the risk-free rate of return, as it has little to no risk.

Market Risk Premium Formula & Calculation

The formula is as follows:

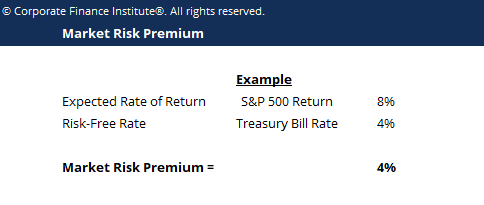

Market Risk Premium = Expected Rate of Return – Risk-Free Rate

Example:

The S&P 500 generated a return of 8% the previous year, and the current interest rate of the Treasury billTreasury Bills (T-Bills)Treasury Bills (or T-Bills for short) are a short-term financial instrument issued by the US Treasury with maturity periods from a few days up to 52 weeks. is 4%. The premium is 8% – 4% = 4%.

Download the Free Template

Enter your name and email in the form below and download the free template now!

Use of Market Risk Premium

As stated above, the market risk premium is part of the Capital Asset Pricing ModelCapital Asset Pricing Model (CAPM)The Capital Asset Pricing Model (CAPM) is a model that describes the relationship between expected return and risk of a security. CAPM formula shows the return of a security is equal to the risk-free return plus a risk premium, based on the beta of that security. In the CAPM, the return of an asset is the risk-free rate, plus the premium, multiplied by the beta of the asset. The beta Unlevered Beta / Asset BetaUnlevered Beta (Asset Beta) is the volatility of returns for a business, without considering its financial leverage. It only takes into account its assets.is the measure of how risky an asset is compared to the overall market. The premium is adjusted for the risk of the asset.

An asset with zero risk and, therefore, zero beta, for example, would have the market risk premium canceled out. On the other hand, a highly risky asset, with a beta of 0.8, would take on almost the full premium. At 1.5 beta, the asset is 150% more volatile than the market.

Volatility

It’s important to reiterate that the relationship between risk and reward is the main premise behind market risk premiums. If a security returns 10% every time period without fail, it has zero volatility of returns. If a different security returns 20% in period one, 30% in period two, and 15% in period three, it has a higher volatility of returns and is, therefore, considered “riskier”, even though it has a higher average return profile.

This is where the concept of risk-adjusted returns comes in. To learn more, please read CFI’s guide to calculating The Sharpe RatioSharpe RatioThe Sharpe Ratio is a measure of risk-adjusted return, which compares an investment's excess return to its standard deviation of returns. The Sharpe Ratio is commonly used to gauge the performance of an investment by adjusting for its risk..

Learn More

We hope this has been a helpful guide to understanding the relationship between risk and reward in corporate finance. CFI is the official global provider of the Financial Modeling and Valuation Analyst (FMVA) certificationBecome a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! program. To keep learning more about corporate finance and financial modeling, we suggest reading the CFI articles below to expand your knowledge base.

- Weighted Average Cost of Capital WACCWACCWACC is a firm’s Weighted Average Cost of Capital and represents its blended cost of capital including equity and debt.

- Sharpe Ratio CalculatorSharpe Ratio CalculatorThe Sharpe Ratio Calculator allows you to measure an investment's risk-adjusted return. Download CFI's Excel template and Sharpe Ratio calculator. Sharpe Ratio = (Rx - Rf) / StdDev Rx. Where: Rx = Expected portfolio return, Rf = Risk free rate of return, StdDev Rx = Standard deviation of portfolio return / volatility

- Valuation MethodsValuation MethodsWhen valuing a company as a going concern there are three main valuation methods used: DCF analysis, comparable companies, and precedent transactions

- Valuation InfographicValuation InfographicOver the years, we've spent a lot of time thinking about and working on business valuation across a broad range of transactions. This valuation infographic

-

Money-Weighted Rate of Return (MWRR) Explained: A Comprehensive Guide

The money-weighted rate of return (MWRR) refers to the discount rate that equates a project’s present value cash flows to its initial investment. It is used to determine the profitability of a p

-

Understanding Risk-Adjusted Return Ratios: A Comprehensive Guide

There are a number of risk-adjusted return ratios that help investors assess existing or potential investments. The ratios can be more helpful than simple investment return metrics that do not take th

finance

- Understanding the Beta Coefficient: A Guide for Investors

- Understanding CAPM: A Comprehensive Guide to Capital Asset Pricing

- Default Risk Premium: Understanding & Calculation

- Understanding Equity Risk Premium: Definition & Calculation

- Interbank Market: A Comprehensive Overview of Foreign Exchange Trading

- Liquidity Premium: Definition, Calculation & Investment Implications

- Understanding the Secondary Market: A Guide for Investors

- Understanding Systematic Risk: Factors Beyond Your Control

- Understanding Market Risk: A Comprehensive Guide

-

Equity Capital Market: Definition & How It Works

Equity Capital Market: Definition & How It WorksThe equity capital market is a subset of the broader capital market, where financial institutions and companies interact to trade financial instruments and raise capital for companies. Equity capital ...

-

Internal Rate of Return (IRR): Definition & Calculation

Internal Rate of Return (IRR): Definition & CalculationThe Internal Rate of Return (IRR) is the discount rate that makes the net present value (NPV)Net Present Value (NPV)Net Present Value (NPV) is the value of all future cash flows (positive and negative...