Understanding Schedule A: Itemized Deductions Explained

Schedule A is an income tax form that is used in the United States to declare itemized deductions.

It is attached to Form 1040 for taxpayers that pay annual income taxesAccounting For Income TaxesIncome taxes and their accounting is a key area of corporate finance. There are several objectives in accounting for income taxes and optimizing a company's valuation.. Taxpayers can choose to claim either a standard tax return deduction or itemize their qualifying deductions line by line. Either of the options will reduce the amount of income that taxpayers need to pay as federal income taxHow to Use the IRS.gov WebsiteIRS.gov is the official website of the Internal Revenue Service (IRS), the United States’ tax collection agency. The website is used by businesses and, and they can choose the option that provides the most savings.

Itemized deductions in Schedule A are deducted from adjusted gross incomeAnnual IncomeAnnual income is the total value of income earned during a fiscal year. Gross annual income refers to all earnings before any deductions are to arrive at the taxable income. The process involves reporting the various categories of allowable deductions and adding them up one by one. To do the calculations correctly, taxpayers must maintain an accurate record of their yearly expenses by maintaining receipts and other documentationSource DocumentsThe paper trail of a company's financial transactions are referred to in accounting as source documents. Whether checks are written to be that proves that the expenses are legitimate. The documentation that taxpayers can maintain includes bank statements, insurance bills, medical bills, donation acknowledgment letters, and property tax statements.

Standard Deductions vs. Schedule A Itemized Deductions

Choosing between the standard deduction and the itemized deduction is a personal choice that individual taxpayers must make. Both methods cannot be used simultaneously.

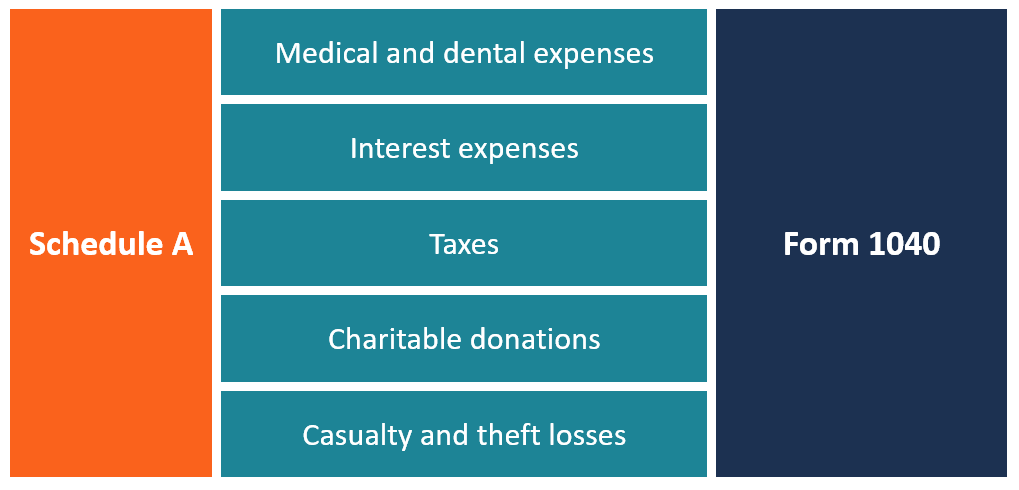

Schedule A includes seven categories of expenses that fall under itemized deductions.

- Medical and dental expenses

- Interest paid

- Taxes paid

- Gifts to charity

- Losses due to casualty and theft

- Job expenses

- Certain miscellaneous expenses

However, the last category was removed in the 2017 tax law, and miscellaneous expenses will no longer be deductible.

On the other hand, for standard deductions, there are specific guidelines on how much should be deducted to arrive at the taxable income. As of December 2017, the standard deduction is $6,350 for single taxpayers, $12,700 for a married couple that is filing jointly, and $9,350 for those who qualify as heads of households.

What Expenses can be Itemized in Schedule A?

Schedule A is categorized into several sections that cover each type of itemized deduction. Here are the main categories of expenses that can be itemized in Schedule A:

1. Medical and dental expenses

Qualified medical and dental expenses that can be listed on Schedule A include expenses that you pay out of pocket. It may include money spent on buying prescription drugs and consultation fees paid for doctor visits. Under the 2017/2018 tax law, taxpayers who incur out-of-pocket medical and dental expenses that are not covered by an insurance plan can deduct such expenses if they exceed 7.5% of their adjusted gross income.

The expenses must not be reimbursed by an insurance company or in any other manner. Under the 2019 tax plan that becomes effective in April 2020, the medical/dental deductions threshold will revert to 10%.

2. Interest expenses paid

The current tax law permits homeowners to subtract the interest that they pay on mortgages and home-equity debt. Interest expense is classified as follows:

Mortgage interest paid: The mortgage interest paid on a main home and a second home is deductible if you pay mortgage loans up to $1 million in total to the bank or mortgage company. Also, mortgage interest is deductible on a mortgage loan of up to $1 million that you pay to an individual for a main home or a second home, if the individual financed the sale.

Home equity loan: You can deduct the interest paid on a home equity loan up to $100,000.

3. Taxes paid

Taxpayers who itemize deductions can deduct two types of taxes – property taxes, and state and local income taxes.

Personal property taxes: Property taxes include state, local, and foreign real estate taxes that taxpayers pay on homes and other properties. For the taxes to be deductible, they must be based on the assessed value of the personal property, and be levied for the general public welfare. The tax must also be a uniform tax for all properties of the jurisdiction in which the tax authority is located.

State and local income taxes: You can deduct state and local taxes if you itemize deductions.

4. Charitable donations

If you choose to itemize deductions on Schedule A, you deduct cash and non-cash charitable donations of up to 50% and 30%, respectively, of your adjusted gross income. Money donations include checks, payroll deductions, credit card donations, cash, and direct withdrawals from a bank account. Non-cash donations include toys, household items, and clothing.

5. Casualty and theft losses

Taxpayers can deduct losses resulting from certain casualties such as fires, theft, or tornado, subject to certain limitations. However, only losses that exceed 10% of adjusted gross income can be deducted. If the taxpayer is reimbursed for the losses in later years, the reimbursement received must be recorded as income.

Additional Resources

Thank you for reading CFI’s guide to Schedule A. CFI is the official provider of the Financial Modeling and Valuation Analyst (FMVA)™Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program, designed to transform anyone into a world-class financial analyst. To keep learning and developing your knowledge of financial analysis, we highly recommend the additional CFI resources below:

- FUTA TaxFUTA TaxFUTA is an abbreviation for Federal Unemployment Tax Act. FUTA Tax is a United States federal tax imposed on employers to help fund unemployment payments.

- Permanent/Temporary Differences in Tax AccountingPermanent/Temporary Differences in Tax AccountingPermanent differences are created when there's a discrepancy between pre-tax book income and taxable income under tax returns and tax

- Salary CalculatorSalary CalculatorThis salary calculator can be used to estimate your annual salary equivalent based on the wage or rate you are paid per hour. Follow the instructions below to convert hourly to annual income and determine your salary on a yearly basis. Simply enter your information and this form will turn hourly to salary

- Tax ShieldTax ShieldA Tax Shield is an allowable deduction from taxable income that results in a reduction of taxes owed. The value of these shields depends on the effective tax rate for the corporation or individual. Common expenses that are deductible include depreciation, amortization, mortgage payments and interest expense

-

Understanding Profit: A Key Financial Metric

Profit is the value remaining after a company’s expenses have been paid. It can be found on an income statement. If the value that remains after expenses have been deducted from revenue is posit

-

Understanding Revenue: A Comprehensive Guide for Businesses

Revenue is the value of all sales of goods and services recognized by a company in a period. Revenue (also referred to as Sales or Income) forms the beginning of a company’s income statementInco

finance

- Understanding Discretionary Income: Definition & Examples

- EBITDA Explained: Understanding Earnings Before Interest, Taxes, Depreciation & Amortization

- Understanding Business Erosion: Causes, Risks & Prevention

- Understanding Income: Definition, Types & Uses

- Understanding Income Properties: A Guide to Real Estate Investment

- Understanding Business Expenses: A Comprehensive Guide

- Understanding the Income Statement: A Comprehensive Guide

- Understanding the Multi-Step Income Statement: A Detailed Guide

- Understanding Non-Operating Expenses: Definition & Examples

-

Understanding Net Income: A Comprehensive Guide

Understanding Net Income: A Comprehensive GuideNet income is the amount of accounting profit a company has left over after paying off all its expenses. Net income is found by taking sales revenueSales RevenueSales revenue is the income received by...

-

Non-Operating Income: Definition, Examples & Significance

Non-Operating Income: Definition, Examples & SignificanceNon-operating income refers to the part of a company’s income that is not attributable to its core business operations. It is a category in a multi-step income statementMulti-Step Income Stateme...