Kelly Criterion: A Guide to Optimal Betting & Investment Strategy

Kelly criterion is a mathematical formula for bet sizing, which is frequently used by investors to decide how much money they should allocate to each investment or bet through a predetermined fraction of assets. It is popular because it typically leads to higher wealth in the long run compared to other types of strategies.

Summary

- Kelly criterion is a mathematical formula for bet sizing, which is frequently used by investors and gamblers to decide how much money they should allocate to each investment or bet through a predetermined fraction of assets.

- It is popular due to how it typically leads to higher wealth in the long run compared to other types of strategies.

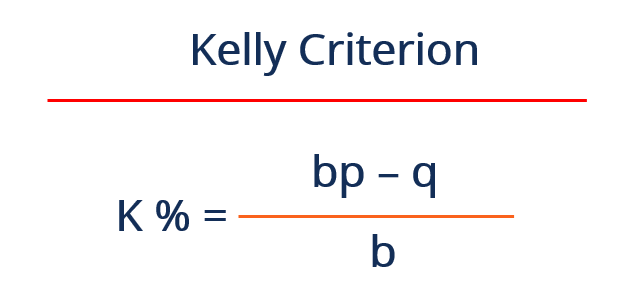

- It is based on the formula k% = bp–q/b, with p and q equaling the probabilities of winning and losing, respectively.

History of the Kelly Criterion

Kelly criterion was developed in 1956 by an American scientist, John L. Kelly, who worked as a researcher at AT&T’s Bell Labs in New Jersey. Kelly originally developed the formula to help the company with its long-distance telephone signal noise issues.

Later, it was picked up upon by the betting community, who realized its value as an optimal betting system since it would allow gamblers to maximize the size of their earnings.

Although it was reported that Kelly never used his formula for personal gain, it is still quite popular today and is used as a general money management system for investing. One reason behind its popularity is because of how frequently it is used by prominent investors, such as Warren Buffet of Berkshire Hathaway.

Understanding the Kelly Criterion

Investors often face a tough decision when trying to decide how much money to allocate, as staking either too much or too little will result in a large impact either way.

The Kelly criterion is a money-management formula that calculates the optimal amount to ensure the greatest chance of success. The formula is as follows:

Where:

- K % = The Kelly percentage that is the fraction of the portfolio Investment PortfolioAn investment portfolio is a set of financial assets owned by an investor that may include bonds, stocks, currencies, cash and cash equivalents, and commodities. Further, it refers to a group of investments that an investor uses in order to earn a profit while making sure that capital or assets are preserved.to bet

- b = The decimal odds that is always equal to 1

- p = The probability of winning

- q = The probability of losing, which is 1 – p

Example

When a dice is thrown, the chance of it landing on a 1, 2, or 3 is 50%, while the same percentage applies to an outcome of 4, 5, or 6.

Now, let us imagine that the dice can rest on a 1, 2, or 3 with a probability of 60%, meaning the probability of it landing on 4, 5, or 6 is 40%. The variables will look as follows:

- b = 1

- p = 0.60

- q = 1 – 0.60 = 0.40

Based on the Kelly criterion, K% = (1 × 0.60 – 0.40) / 1 = 0.20 or 20%

The formula is therefore suggesting that 20% of the portfolio be stake 20% of your bankroll. If the dice bias were less, at 53%, the Kelly criterion recommends staking 6%.

In such a case, the Kelly criterion suggests that if one were to go over 20% repeatedly on a low number, there is a high chance one would eventually go broke.

Under-betting less than 20%, on the other hand, would lead to a smaller profit, which means that adhering to the Kelly criterion will maximize the rate of capital growth for the long-term.

Analysis of the Results

The Kelly criterion results in the K%, which refers to a percentage that represents the size of the portfolio to devote to each investment. Basically, the Kelly percentage provides information on how much one should diversify.

One should not commit more than 20% to 25% of the capital into single equity regardless of what the Kelly criterion says, since diversificationDiversificationDiversification is a technique of allocating portfolio resources or capital to a variety of investments.The goal of diversification is to mitigate losses itself is important and essential to avoid a large loss in the event a stock fails.

Some investors prefer to bet less than the Kelly percentage due to being risk-averse, which is understandable, as it means that it reduces the impact of possible over-estimation and depleting the bankroll. It is known as Fractional Kelly.

On the other hand, if the Kelly percentage results in a percentage less than 0%, it means that the Kelly criterion is recommending that one walk away and not bet anything at all since the odds do not seem to be in one’s favor based on the formula and mathematical calculation.

Following the Kelly criterion typically results in success due to the formula is based on a simple formula using pure mathematics.

However, factors that can impact the success include accurate inputs of the probabilities of winning and losing, as an incorrect percentage would be detrimental.

In addition to that, there may be unexpected events such as stock marketStock MarketThe stock market refers to public markets that exist for issuing, buying and selling stocks that trade on a stock exchange or over-the-counter. Stocks, also known as equities, represent fractional ownership in a company crashes, which would impact all stocks regardless if the Kelly criterion was used or not.

Learn More

CFI is the official provider of the global Commercial Banking & Credit Analyst (CBCA)™Program Page - CBCAGet CFI's CBCA™ certification and become a Commercial Banking & Credit Analyst. Enroll and advance your career with our certification programs and courses. program, designed to teach you all the knowledge and skills required to become a skilled credit analyst. The following CFI resources will help further your financial education and advance your career:

- Asset AllocationAsset AllocationAsset allocation refers to a strategy in which individuals divide their investment portfolio between different diverse categories

- Money ManagementMoney ManagementMoney management refers to the process of tracking and planning an individual or group’s use of capital. In personal and corporate finance, money management

- Martingale StrategyMartingale StrategyThe Martingale Strategy involves doubling the trade size every time a loss is faced. A classic scenario for the strategy is to try and trade

- Stock Market CrashStock Market CrashA stock market crash refers to a drastic, often unforeseen, drop in the prices of stocks in the stock market. The sudden drop in stock prices

-

Klinger Oscillator: Understanding Long-Term Trends & Price Reversals

The Klinger oscillator is a financial tool that was designed by Stephen Klinger in 1977 to predict long-term trends in money flow while also detecting short-term fluctuations. In addition, it predicts

-

Margin of Safety: A Powerful Investment Principle

The margin of safety is an investment principle where the investor buys stocks when the market price is below their actual value. It is evaluated as the change between the price of a financial in

invest

- Understanding the Investment Accumulation Phase: Building Wealth Over Time

- Bandwagon Effect: Understanding Social Influence & Conformity

- Understanding the Call Market: Trading Hours & Price Determination

- Understanding the Credit Curve: A Guide for Investors

- Understanding the Dot-Com Bubble: Causes, Impact & Lessons Learned

- Dow 30 Explained: Understanding the Dow Jones Industrial Average

- Understanding the Dow Divisor: How It Impacts the DJIA

- Rule of 72: Calculate Investment Doubling Time | [Your Brand Name]

- Nifty 50: History, Significance & Key Stocks - A Comprehensive Guide

-

Kelly Criterion: A Guide to Optimal Betting & Investment Strategy

Kelly Criterion: A Guide to Optimal Betting & Investment StrategyKelly criterion is a mathematical formula for bet sizing, which is frequently used by investors to decide how much money they should allocate to each investment or bet through a predetermined fraction...

-

Keltner Channel: Definition, How to Use & Trading Strategies

Keltner Channel: Definition, How to Use & Trading StrategiesKeltner Channel refers to a technical analysis indicator composed of three separate lines. It includes a central moving average line along with channel lines located above and below the central one.&n...