Matrix Pricing: Estimating Value for Illiquid Securities

Matrix pricing is an estimation technique used to estimate the market price of securities that are not actively traded. Matrix pricing is primarily used in fixed incomeFixed Income SecuritiesFixed income securities are a type of debt instrument that provides returns in the form of regular, or fixed, interest payments and repayments of the, to estimate the price of bonds that do not have an active market. The price of the bond is estimated by comparing it to corporate bonds with an active market, and that have similar maturities, coupon rates, and credit rating. This relative estimation process can be very helpful for debtDebtDebt is the money borrowed by one party from another to serve a financial need that otherwise cannot be met outright. Many organizations use debt to procure goods and services that they can’t manage to pay for with cash. valuation of private companiesPrivately Held CompanyA privately held company is a company’s whose shares are owned by individuals or corporations and that does not offer equity interests to investors in the form of stock shares traded on a public stock exchange., which typically don’t report as much information as public companiesPublic Company FilingsPublic company filings are an important source of data and information for financial analysts. Knowing where to find this information is a critical first step in performing financial analysis and financial modeling. This guide will outline the most common sources of public company filings..

Another use of matrix pricing is for bond underwriting, which can be used to estimate what the market’s required rate of return on the bond will be.

What is Yield to Maturity?

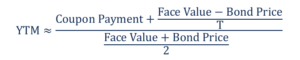

Yield to Maturity (YTM) is the total expected return from a bond if the bond is held until maturity, i.e., until the end of its lifetime, and all coupon are reinvested at the same rate.

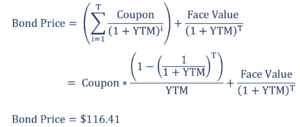

- Couponi is the coupon payment received by the bondholder at period i.

- Face Value is the amount on which the coupon payments are calculated.

- Bond Price is the market price of the bond.

If we assume that coupon payments don’t change over time, then:

The formula shown above describes a polynomial in YTM. An approximate formula for the Yield to Maturity is the following:

Learn more about YTM on CFI’s Fixed Income Fundamentals Course!

Practical Example of Matrix Pricing

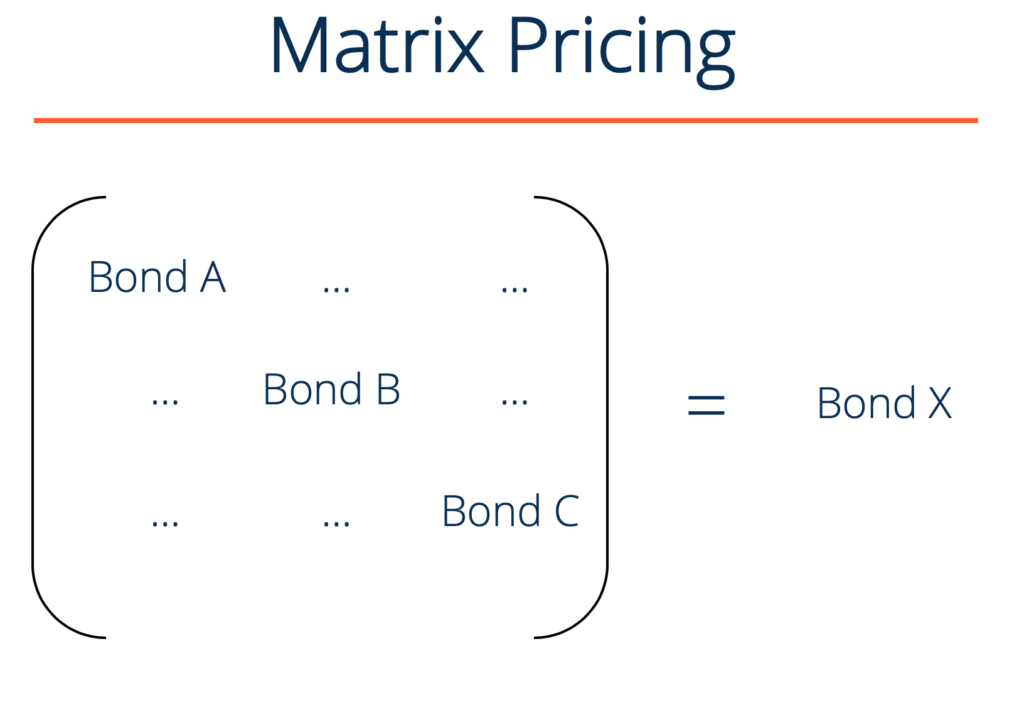

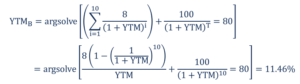

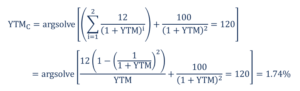

Bond A is a 6-year 10% annual coupon payment bondCoupon BondA coupon bond is a type of bond that includes attached coupons and pays periodic (typically annual or semi-annual) interest payments during its lifetime and its par value at maturity. These bonds come with a coupon rate, which refers to the bond's yield at the date of issuance. that is not actively traded on the market. Bond B is a 10-year 8% annual coupon payment bond that is actively traded on the market and with a market price of $80. Bond C is a 2-year 12% annual coupon payment bond that is actively traded on the market and with a market price of $120. All bonds come with a face valuePar ValuePar Value is the nominal or face value of a bond, or stock, or coupon as indicated on a bond or stock certificate. It is a static value of $100. In order to price Bond A:

1. Calculate the yield to maturity of Bonds B and C.

2. The estimated market discount rate of the 6-year 10% bond is the arithmetic mean of YTMB and YTMC. Therefore, YTMA = (11.46% + 1.74%) / 2 = 6.6%. An alternative method to calculate YTMA is to take the geometric mean of YTMB and YTMC.

3. Therefore, the estimated market price of Bond A is given by the following formula:

The estimated market price of Bond A based on Bonds B and C is $116.41. The estimation method is called matrix pricing because it uses a matrix like the one shown above.

More Resources

Thank you for reading CFI’s explanation of matrix pricing. CFI offers the Financial Modeling & Valuation Analyst (FMVA)™Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program for those looking to take their careers to the next level. To keep learning and advancing your career, the following resources will be helpful:

- Coupon RateCoupon RateA coupon rate is the amount of annual interest income paid to a bondholder, based on the face value of the bond.

- Equity vs Fixed IncomeEquity vs Fixed IncomeEquity vs Fixed Income. Equity and fixed income products are financial instruments that have very important differences every financial analyst should know. Equity investments generally consist of stocks or stock funds, while fixed income securities generally consist of corporate or government bonds.

- Marketable SecuritiesMarketable SecuritiesMarketable securities are unrestricted short-term financial instruments that are issued either for equity securities or for debt securities of a publicly listed company. The issuing company creates these instruments for the express purpose of raising funds to further finance business activities and expansion.

- Option Pricing ModelsOption Pricing ModelsOption Pricing Models are mathematical models that use certain variables to calculate the theoretical value of an option. The theoretical value of an

-

Understanding Noncallable Securities: A Comprehensive Guide

Noncallable, also called non-redeemable, refers to the type of securities that cannot be called (redeemed) by their issuer(s) before their maturities unless penalties are paid to security holders. Two

-

Prediction Markets: Understanding How They Work & Their Applications

A prediction market or betting market is an exchange-traded market where individuals can bet on the outcome of a variety of events with an unknown future. The events range from future commodity prices

invest

- Understanding Auction Markets: How Prices Are Determined

- Understanding Bond Pricing: Key Factors & Valuation

- Coupon Bonds: Understanding Fixed Income & Interest Payments

- Discount Bonds: Understanding Pricing & Secondary Markets

- Doji Candlestick Pattern: Meaning & Trading Signals

- Understanding the EMBI: A Guide to Emerging Market Bond Performance

- Understanding Frothy Markets: Risks & Opportunities

- Understanding Inefficient Markets: Causes & Implications

- Penetration Pricing: A Comprehensive Guide to Gaining Market Share

-

Understanding Market Sentiment: A Guide for Investors

Understanding Market Sentiment: A Guide for InvestorsThe term market sentiment, also known as investor sentiment, refers to the general outlook or attitude of investors toward a particular security or the overall financial market. The optimism or pessim...

-

![Market Timing: Strategies & How It Works | [Your Company Name]](https://www.etffin.com/article/uploadfiles/202110/2021100815253643_S.jpeg) Market Timing: Strategies & How It Works | [Your Company Name]

Market Timing: Strategies & How It Works | [Your Company Name]Market timing refers to an investing strategy through which a market participant makes buying or selling decisions by predicting the price movements of a financial asset in the future. Investors follo...