Understanding Bond Pricing: Key Factors & Valuation

Bond pricing is an empirical matter in the field of financial instrumentsPublic SecuritiesPublic securities, or marketable securities, are investments that are openly or easily traded in a market. The securities are either equity or debt-based.. The price of a bond depends on several characteristics inherent in every bond issued. These characteristics are:

- Coupon, or lack thereof

- Principal/par value

- Yield to maturity

- Periods to maturity

Alternatively, if the bond price and all but one of the characteristics are known, the last missing characteristic can be solved for.

Bond Pricing: Coupons

A bond may or may not come with attached coupons. A coupon is stated as a nominal percentage of the par value (principal amount) of the bond. Each coupon is redeemable per period for that percentage. For example, a 10% coupon on a $1000 par bond is redeemable each period.

A bond may also come with no coupon. In this case, the bond is known as a zero-coupon bond. Zero-coupon bondsOriginal Issue Discount (OID)An original issue discount (OID) is a type of debt instrument. Often a bond, OID's are sold at a lower value than face value when issued are typically priced lower than bonds with coupons.

Bond Pricing: Principal/Par Value

Each bond must come with a par valuePar ValuePar Value is the nominal or face value of a bond, or stock, or coupon as indicated on a bond or stock certificate. It is a static value that is repaid at maturity. Without the principal value, a bond would have no use. The principal value is to be repaid to the lender (the bond purchaser) by the borrower (the bond issuer). A zero-coupon bond pays no coupons but will guarantee the principal at maturity. Purchasers of zero-coupon bonds earn interest by the bond being sold at a discount to its par value.

A coupon-bearing bond pays coupons each period, and a coupon plus principal at maturity. The price of a bond comprises all these payments discounted at the yield to maturity.

Bond Pricing: Yield to Maturity

Bonds are priced to yield a certain return to investors. A bond that sells at a premium (where price is above par value) will have a yield to maturity that is lower than the coupon rate. Alternatively, the causality of the relationship between yield to maturityCost of DebtThe cost of debt is the return that a company provides to its debtholders and creditors. Cost of debt is used in WACC calculations for valuation analysis. and price may be reversed. A bond could be sold at a higher price if the intended yield (market interest rate) is lower than the coupon rate. This is because the bondholder will receive coupon payments that are higher than the market interest rate, and will, therefore, pay a premium for the difference.

Bond Pricing: Periods to Maturity

Bonds will have a number of periods to maturity. These are typically annual periods, but may also be semi-annual or quarterly. The number of periods will equal the number of coupon payments.

The Time Value of Money

Bonds are priced based on the time value of money. Each payment is discounted to the current time based on the yield to maturity (market interest rate). The price of a bond is usually found by:

P(T0) = [PMT(T1) / (1 + r)^1] + [PMT(T2) / (1 + r)^2] … [(PMT(Tn) + FV) / (1 + r)^n]

Where:

- P(T0) = Price at Time 0

- PMT(Tn) = Coupon Payment at Time N

- FV = Future Value, Par Value, Principal Value

- R = Yield to Maturity, Market Interest Rates

- N = Number of Periods

Bond Pricing: Main Characteristics

Ceteris paribus, all else held equal:

- A bond with a higher coupon rate will be priced higher

- A bond with a higher par value will be priced higher

- A bond with a higher number of periods to maturity will be priced higher

- A bond with a higher yield to maturity or market rates will be priced lower

An easier way to remember this is that bonds will be priced higher for all characteristics, except for yield to maturity. A higher yield to maturity results in lower bond pricing.

Bond Pricing: Other “Soft” Characteristics

The empirical characteristics outlined above affect bond issues, especially in the primary market. There are other, however, bond characteristics that can affect bond pricing, especially in the secondary markets. These are:

- Creditworthiness of issuing firm

- Liquidity of bond trade

- Time to next payment

Firm Creditworthiness

Bonds are rated based on the creditworthiness of the issuing firm. These ratings range from AAA to DS&P – Standard and Poor'sStandard & Poor’s is an American financial intelligence company that operates as a division of S&P Global. S&P is a market leader in the. Bonds rated higher than A are typically known as investment-grade bonds, whereas anything lower is colloquially known as junk bonds.

Junk bonds will require a higher yield to maturity to compensate for their higher credit risk. Because of this, junk bonds trade at a lower price than investment-grade bonds.

Bond Liquidity

Bonds that are more widely traded will be more valuable than bonds that are sparsely traded. Intuitively, an investor will be wary of purchasing a bond that would be harder to sell afterward. This drives prices of illiquid bonds down.

Time To Payment

Finally, time to the next coupon payment affects the “actual” price of a bond. This is a more complex bond pricing theory, known as ‘dirty’ pricing. Dirty pricing takes into account the interest that accrues between coupon payments. As the payments get closer, a bondholder has to wait less time before receiving his next payment. This drives prices steadily higher before it drops again right after coupon payment.

Learn more about bonds

- Fixed Income TradingFixed Income TradingFixed income trading involves investing in bonds or other debt security instruments. Fixed income securities have several unique attributes and factors that

- Bond TermsFixed Income Bond TermsDefinitions for the most common bond and fixed income terms. Annuity, perpetuity, coupon rate, covariance, current yield, par value, yield to maturity. etc.

- Debt Capital MarketsDebt Capital Markets (DCM)Debt Capital Markets (DCM) groups are responsible for providing advice directly to corporate issuers on the raising of debt for acquisitions, refinancing of existing debt, or restructuring of existing debt. These teams operate in a rapidly moving environment and work closely with an advisory partner

- Debt ScheduleDebt ScheduleA debt schedule lays out all of the debt a business has in a schedule based on its maturity and interest rate. In financial modeling, interest expense flows

-

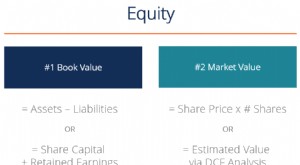

Understanding Equity: A Comprehensive Guide for Investors

In finance and accounting, equity is the value attributable to the owners of a business. The book value of equity is calculated as the difference between assetsTypes of AssetsCommon types of assets in

-

Face Value Explained: Definition, Examples & Importance

The value mentioned on an instrument like a coin, stamp, or bill is called the face value of that instrument. For example, a $100 bill comes with a face value of $100. In calculus, the face value of 3

invest

- Understanding Bond Face Value: Definition & Importance

- Understanding Bond Accretion: A Comprehensive Guide

- Understanding Basis Points: A Guide to Bond Yield Changes

- Coupon Bonds: Understanding Fixed Income & Interest Payments

- Discount Bonds: Understanding Pricing & Secondary Markets

- Ex-Post Analysis: Understanding Outcomes After Events

- Understanding Historic Pricing and Net Asset Value (NAV)

- Matrix Pricing: Estimating Value for Illiquid Securities

- Understanding Noncallable Securities: A Comprehensive Guide

-

Understanding Financial Denomination: A Comprehensive Guide

Understanding Financial Denomination: A Comprehensive GuideA denomination is a classification for the face value of a financial instrument. It includes financial instruments, such as bondsBondsBonds are fixed-income securities that are issued by corporations ...

-

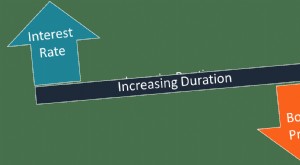

Understanding Bond Duration: A Key Fixed Income Metric

Understanding Bond Duration: A Key Fixed Income MetricDuration is one of the fundamental characteristics of a fixed-income security (e.g., a bondBondsBonds are fixed-income securities that are issued by corporations and governments to raise capital....