Swaptions Explained: Understanding Interest Rate Option Contracts

A swaption (also known as a swap option) is an option contractEmbedded OptionAn embedded option is a provision in a financial security (typically in bonds) that provides an issuer or holder of the security a certain right but not an obligation to perform some actions at some point in the future. The embedded options exist only as a component of financial security that grants its holder the right but not the obligation to enter into a predetermined swap contract. In return for the right, the holder of the swaption must pay a premium to the issuer of the contract. Swaptions typically provide the rights to enter into interest rate swapsInterest Rate SwapAn interest rate swap is a derivative contract through which two counterparties agree to exchange one stream of future interest payments for another, but swaptions with other types of swaps can also be created.

Understanding Swaptions

In terms of their trading characteristics, swaptions are closer to swaps than to options. For example, swaptions are over-the-counterOver-the-Counter (OTC)Over-the-counter (OTC) is the trading of securities between two counter-parties executed outside of formal exchanges and without the supervision of an exchange regulator. OTC trading is done in over-the-counter markets (a decentralized place with no physical location), through dealer networks. securities similar to swaps. In other words, the derivative contracts are traded over-the-counter, not on centralized exchanges. Also, the swaptions benefit from a great degree of flexibility since the contracts do not come in a standardized form.

Before the transaction, the counterparties in a swaption must agree on the various features of the contract. For example, the parties determine the price of the swaption (also known as the swaption’s premium) and the length of the option.

In addition, the counterparties must decide on the features of the underlying swap. The features generally include the notional amount, swap’s legs (fixed vs. float), and frequency of adjustment for the variable leg. Also, the counterparties determine the benchmark for the floating leg of a swap.

Applications of Swaptions

Swaptions come with numerous applications in the investment industry. For example, they are frequently used in hedging various macroeconomic risks such as interest rate riskInterest Rate RiskInterest rate risk is the probability of a decline in the value of an asset resulting from unexpected fluctuations in interest rates. Interest rate risk is mostly associated with fixed-income assets (e.g., bonds) rather than with equity investments.. A company anticipating an interest rate increase may purchase a payer swaption to protect itself from the interest rate risk. Additionally, the swaption may allow hedging the risks associated with financial securities such as bonds. Also, financial institutions commonly employ swaptions to change their payoff profile.

Swaptions are primarily employed by large corporations and financial institutions, including investment banksList of Top Investment BanksList of the top 100 investment banks in the world sorted alphabetically. Top investment banks on the list are Goldman Sachs, Morgan Stanley, BAML, JP Morgan, Blackstone, Rothschild, Scotiabank, RBC, UBS, Wells Fargo, Deutsche Bank, Citi, Macquarie, HSBC, ICBC, Credit Suisse, Bank of America Merril Lynch, commercial banks, and hedge funds.

Types of Swaptions

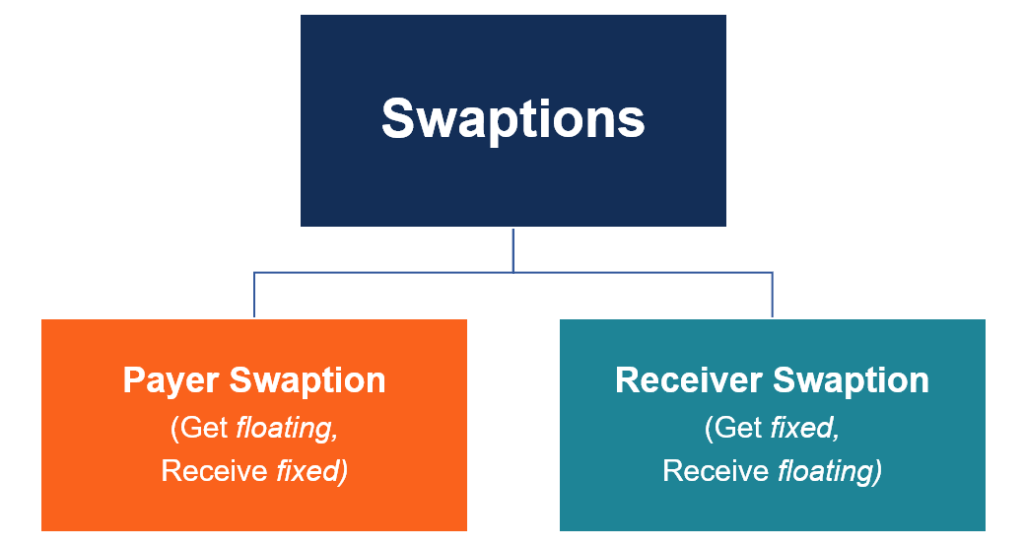

The classification of swaptions is based on the types of legs involved in the anticipating swap contract. Based on such a classification, there are two primary types of swaption: payer swaption and receiver swaption.

With the purchase of a payer swaption, the purchaser obtains the right to enter into a swap contract, which implies that he or she receives the floating swap leg in exchange for the fixed swap leg.

Conversely, the receiver swaption delivers the right but not an obligation to enter into a swap contract, in which the holder of a swap must pay the floating swap in exchange for the fixed swap leg.

Execution Styles

Similar to plain-vanilla options, swaption contracts come with different execution styles. In other words, different swaptions contain different clauses that determine the exercise dates. The most common swaption styles include European, American, and Bermudian styles.

- European swaption: A swaption that can be exercised only on the exercise date.

- American swaption: A swaption that can be exercised on any date between the origination and exercise dates, as well as on the exercise date.

- Bermudian swaption: A swaption that can be exercised on several predetermined dates in between the origination and exercise dates.

The swaptions styles are crucial in selecting the appropriate valuation method. For example, European style swaptions are typically valued using the Black valuation model. On the other hand, American and Bermudian swaptions, which are considered to be more complex relative to European options, are usually priced using Black-Derman-Toy or Hull-White models.

More Resources

CFI is the official provider of the Financial Modeling and Valuation Analyst (FMVA)™Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program, designed to transform anyone into a world-class financial analyst.

To keep learning and developing your knowledge of financial analysis, we highly recommend the additional resources below:

- Hedging ArrangementHedging ArrangementHedging arrangement refers to an investment whose aim is to reduce the level of future risks in the event of an adverse price movement of an asset. Hedging provides a sort of insurance cover to protect against losses from an investment.

- Hybrid SecuritiesHybrid SecuritiesHybrid securities are investment instruments that combine the features of pure equities and pure bonds. The securities tend to offer a higher return than pure fixed income securities such as bonds but a lower return than pure variable income securities such as equities.

- Options: Calls and PutsOptions: Calls and PutsAn option is a derivative contract that gives the holder the right, but not the obligation, to buy or sell an asset by a certain date at a specified price.

- Swap RateSwap RateThe swap rate is the fixed rate of a swap determined by the parties involved in the contract The swap rate is demanded by a receiver (i.e., the party that receives the fixed rate) from a payer (i.e., the party that pays the fixed rate) to be compensated for the uncertainty regarding fluctuations in the floating rate

-

Currency Swap Contracts: Definition & How They Work

A currency swap contract (also known as a cross-currency swap contract) is a derivative contract between two parties that involves the exchange of interest payments, as well as the exchange of princip

-

Debt/Equity Swap: Understanding Financial Restructuring

A debt/equity swap is a mechanism a company utilizes for financial restructuring. It can also be viewed as a renegotiation of debt. In a debt/equity swap, a lender receives an equity interest such as

invest

- Commodity Swaps: Definition, Uses & Hedging Strategies

- ASCOT Options: Understanding Asset-Swapped Convertible Options

- Asset Swap Explained: Definition, OTC Trading & Key Concepts

- Bermuda Swaptions: Definition, Function & Key Features

- Call Swaptions: Understanding Receiver Options for Tax Rate Swaps

- Cross Currency Swaps: Definition, Mechanics & Benefits

- Foreign Exchange Swaps: Definition, Mechanics & Uses

- Inflation Swaps: Understanding & Hedging Inflation Risk

- Put Swaption: Understanding Payer Swaptions and Rate Swaps

-

Credit Default Swaps (CDS): A Comprehensive Guide

Credit Default Swaps (CDS): A Comprehensive GuideA credit default swap (CDS) is a type of credit derivative that provides the buyer with protection against defaultKnowledgeCFI self-study guides are a great way to improve technical knowledge of finan...

-

Swaptions Explained: Understanding Interest Rate Option Contracts

Swaptions Explained: Understanding Interest Rate Option ContractsA swaption (also known as a swap option) is an option contractEmbedded OptionAn embedded option is a provision in a financial security (typically in bonds) that provides an issuer or holder of the sec...