Bullet Bond Portfolios: A Comprehensive Guide

A bullet bond portfolio, commonly referred to as a bullet portfolio, is made up of a range of bullet bonds, from short-term to long-term bullet bonds. A bullet bond is a non-callable bondNon-Callable BondA non-callable bond is a bond that is only paid out at maturity. The issuer of a non-callable bond can’t call the bond prior to its date of maturity. It is different from a callable bond, which is a bond where the company or entity that issues the bond owns the right to repay the face value of the bond wherein the total principal amount or its total value is paid in a lump sum on the bond’s maturity date.

Summary:

- A bullet bond is a type of a non-callable bond wherein the total principal amount or total value is paid in a lump sum on the bond’s maturity date.

- A bullet bond portfolio, commonly referred to as bullet portfolio, is made up of short-term and long-term bullet bonds.

- Bullet bonds generally carry a relatively lower interest rate. It is a result of the high risk exposure on the debt issuer’s part.

How Does the Bullet Bond Investment Strategy Work?

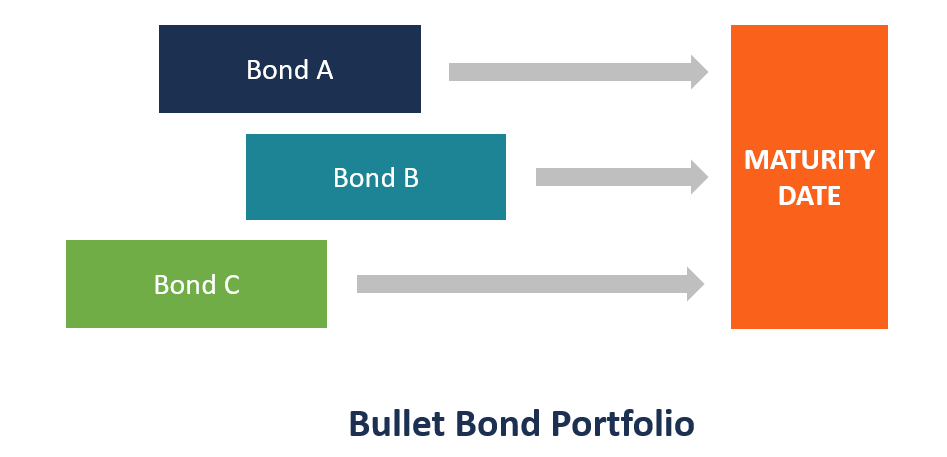

The bullet bond investment strategy is centered around creating a bullet portfolio, i.e., purchasing a number of bonds with the same maturity date. When the bonds mature on the same date, the portfolio generates substantial earnings all at once at the high end of the yield curve.

While a bullet portfolio is composed of bonds purchased in a way that all bonds come with the same maturity date, it is important to remember that the bonds are not purchased at the same time. A bullet portfolio is built by purchasing bonds at different times but with the same maturity date. It is done with the idea of diversifying the portfolio on the basis of purchase time and consequently spreading the risk of interest rateInterest RateAn interest rate refers to the amount charged by a lender to a borrower for any form of debt given, generally expressed as a percentage of the principal. fluctuations over different purchase times.

Bullet Bond Portfolio – Features

1. Principal value paid in a lump sum

A bullet bond’s total principal value is paid in a lump sum on its maturity date. This is in contrast to the general practice of amortizing a bond’s principal value over its lifetime.

2. Non-callable

It means that a bullet bond cannot be “called” or redeemed early by the debt issuerBond IssuersThere are different types of bond issuers. These bond issuers create bonds to borrow funds from bondholders, to be repaid at maturity..

3. Higher risk level for the debt issuer

A bullet bond generally carries more risk for the debt issuer since it requires payment of its entire principal amount all at once, as opposed to the general practice of amortizing a bond’s value over its lifetime. This results in a very heavy repayment obligation on the debt issuer’s part.

4. Relatively lower interest rate

Bullet bonds generally carry a relatively lower interest rate. It is a result of the high risk exposure on the debt issuer’s part.

Real-life Applications

Generally, investors adopt the bullet bond investment strategy when they need a sizable amount of capital in the future. The strategy can be used in several real-life applications, including:

- Buying a house or large property

- Remodeling a house

- Financing college education

- Purchasing a car

- Paying for mortgageMortgageA mortgage is a loan – provided by a mortgage lender or a bank – that enables an individual to purchase a home. While it’s possible to take out loans to cover the entire cost of a home, it’s more common to secure a loan for about 80% of the home’s value.

Illustrative Example

An investor wants to pay for his 15-year old daughter’s university education. Anticipating the high cost of full-time university education, the investor decides to implement a bullet investing strategy using bonds. He builds his bullet bond portfolio with a four-year maturity period in mind, as that is when his daughter would be heading off to the university. The investor purchases bonds at different times, i.e., in Year 1, Year 2, and Year 3, all maturing in year 4.

Implementing such a strategy aims to achieve a “bullet boost” of funds in Year 4 to finance the university education. Since the investor uses a bullet bond strategy, which involves purchasing bonds at different times with the same maturity date, the investor does not need to experience a sudden huge outflow of funds. In Year 4, the investor gets his total principal amount back, which helps fund his daughter’s university education.

Related Readings

CFI is the official provider of the Financial Modeling and Valuation Analyst (FMVA)™Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program, designed to transform anyone into a world-class financial analyst.

To keep learning and developing your knowledge of financial analysis, we highly recommend the additional CFI resources below:

- BondsBondsBonds are fixed-income securities that are issued by corporations and governments to raise capital. The bond issuer borrows capital from the bondholder and makes fixed payments to them at a fixed (or variable) interest rate for a specified period.

- Fixed Income PortfolioFixed Income PortfolioA fixed income portfolio comprises investment securities that pay a fixed interest until its maturity date. Upon maturity, the principal amount of the

- Term to MaturityTerm to MaturityTerm to maturity is the remaining life of a bond or other type of debt instrument. The duration ranges between the time when the bond is issued until its

- Bond PricingBond PricingBond pricing is the science of calculating a bond's issue price based on the coupon, par value, yield and term to maturity. Bond pricing allows investors

-

Amortized Bonds: Understanding Principal Repayment

An amortized bond is a bond with the principal amount – otherwise known as face value –regularly paid down over the life of the bond. The bond’s principal is divided up according to

-

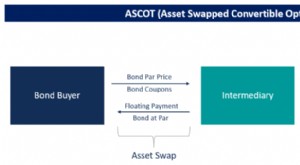

ASCOT Options: Understanding Asset-Swapped Convertible Options

The term ASCOT is short for Asset Swapped Convertible Option Transaction. It is an American style call option to buy back a convertible bond. It falls under the category of financial products called s

invest

- Active Bond Portfolio Management: Strategies & Benefits

- Barbell Bond Portfolio: Strategy, Benefits & Risk

- Understanding Financial Benchmarks: A Comprehensive Guide

- Coupon Bonds: Understanding Fixed Income & Interest Payments

- Discount Bonds: Understanding Pricing & Secondary Markets

- Laddered Bond Portfolio: A Risk-Mitigating Investment Strategy

- Understanding Noncallable Securities: A Comprehensive Guide

- Samurai Bonds: A Guide to Understanding Yen-Denominated Corporate Debt

- Treasury Bonds: A Comprehensive Guide to U.S. Government Debt

-

![Active Management: Strategies & How It Works | [Your Company Name]](https://www.etffin.com/article/uploadfiles/202110/2021100815211459_S.jpeg) Active Management: Strategies & How It Works | [Your Company Name]

Active Management: Strategies & How It Works | [Your Company Name]Active management is the use of human capital to manage a portfolio of funds. Active managers rely on analytical research, personal judgment, and forecasts to make decisions on what securities to buy,...

-

Understanding Amortizable Bond Premiums: A Comprehensive Guide

Understanding Amortizable Bond Premiums: A Comprehensive GuideAn amortizable bond premium refers to the excess amount paid for a bond over its face value or par valuePar ValuePar Value is the nominal or face value of a bond, or stock, or coupon as indicated on a...