Segmented Markets Theory: Understanding Bond Term Structure

The segmented markets theory states that the market for bondsBondsBonds are fixed-income securities that are issued by corporations and governments to raise capital. The bond issuer borrows capital from the bondholder and makes fixed payments to them at a fixed (or variable) interest rate for a specified period. is ‘segmented’ on the basis of the bonds’ term structure, and that ‘segmented’ markets operate more or less independently. Under the segmented markets theory, the return offered by a bond with a specific term structure is determined solely by the supply and demandSupply and DemandThe laws of supply and demand are microeconomic concepts that state that in efficient markets, the quantity supplied of a good and quantity for that bond and independent of the return offered by bonds with different term structures.

History of the Segmented Markets Theory

The Segmented Markets Theory was introduced by American economist John Mathew Culbertson (1921-2001) in his 1957 paper titled “The Term Structure of Interest Rates.” In his paper, Culbertson argued against Irving Fisher’s expectations driven model of the term structure and developed his own theory of how fixed income securities are priced by the market.

What is Term Structure?

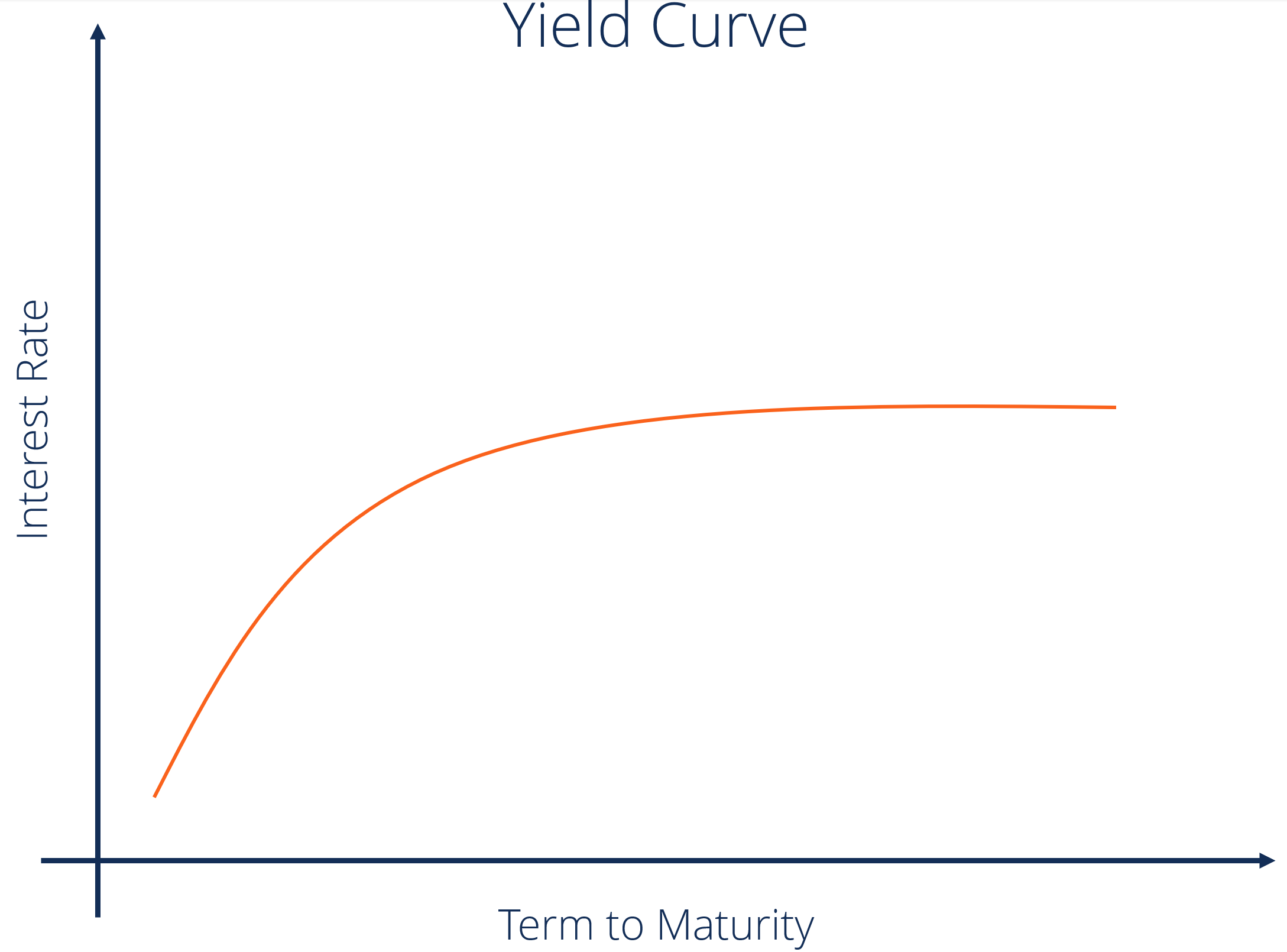

Term structure, also known as the yield curveYield CurveThe Yield Curve is a graphical representation of the interest rates on debt for a range of maturities. It shows the yield an investor is expecting to earn if he lends his money for a given period of time. The graph displays a bond's yield on the vertical axis and the time to maturity across the horizontal axis. when graphically represented, is the relationship between the interest rate paid by an asset (usually government bonds10-Year US Treasury NoteThe 10-year US Treasury Note is a debt obligation that is issued by the US Treasury Department and comes with a maturity of 10 years.) and the time to maturity. Interest rate is measured on the vertical axis and time to maturity is measured on the horizontal axis.

Normally, interest rates and time to maturity are positively correlatedCorrelationA correlation is a statistical measure of the relationship between two variables. The measure is best used in variables that demonstrate a linear relationship between each other. The fit of the data can be visually represented in a scatterplot.. Therefore, interest rates rise with an increase in the time to maturity. It results in the term structure taking on a positive slope. The yield curve is often seen as a bond market’s measure of confidence in the economy.

CFI has a comprehensive course covering all the fundamentals for fixed income securities. Check out our Fixed Income Fundamentals Course now!

Breaking Down the Segmented Markets Theory

The segmented markets theory states that the bond market is full of heterogeneous agents with different income needs. Therefore, different agents in the bond market invest in different parts of the term structure based on their income needs.

Banks tend to mainly participate in the buying and selling of short-term bonds (it is mainly due to the modern banking practice of fractional reservesFractional BankingFractional Banking is a banking system that requires banks to hold only a portion of the money deposited with them as reserves. The reserves are held as balances in the bank’s account at the central bank or as currency in the bank.) whereas pension funds tend to mainly participate in the buying and selling of long-term bonds (it is mainly due to the stable income requirements of pension funds).

According to the expectations hypothesisLocal Expectations TheoryIn finance and economics, the Local Expectations Theory is a theory that suggests that the returns of bonds with different maturities should be the same over the short-term investment horizon. Essentially, the local expectations theory is one of the variations of the pure expectations theory, the return on any long-term fixed incomeFixed Income Bond TermsDefinitions for the most common bond and fixed income terms. Annuity, perpetuity, coupon rate, covariance, current yield, par value, yield to maturity. etc. security must be equal to the expected return from a sequence of short-term fixed income securities. Therefore, any long-term fixed income security can be recreated using a sequence of short-term fixed income securities.

However, the segmented markets theory also says that long-term fixed income securities and short-term fixed income securities are fundamentally different and should not be put in the same class of assets. In general, the holders of long-term bonds need to worry about a lot more things than the holders of short-term bonds.

For example, the holders of 10-year US government bonds need to worry about inflation for the next 10 periods and interest rates for the next 10 periods whereas the holders of 1-year US government bonds only need to worry about inflation for the next period and interest rate for the next period.

Therefore, the 10-year US government bond is a very different fixed income instrument from the 1-year US government bond, and a 10-year US government bond can’t be recreated using a sequence of ten 1-year US government bonds.

Additional Resources

CFI is the official provider of the global Financial Modeling & Valuation Analyst (FMVA)™Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional resources below will be useful:

- Fixed Income Fundamentals

- Bond PricingBond PricingBond pricing is the science of calculating a bond's issue price based on the coupon, par value, yield and term to maturity. Bond pricing allows investors

- Coupon RateCoupon RateA coupon rate is the amount of annual interest income paid to a bondholder, based on the face value of the bond.

- Debt Capital Markets (DCM)Debt Capital Markets (DCM)Debt Capital Markets (DCM) groups are responsible for providing advice directly to corporate issuers on the raising of debt for acquisitions, refinancing of existing debt, or restructuring of existing debt. These teams operate in a rapidly moving environment and work closely with an advisory partner

-

Dow 30 Explained: Understanding the Dow Jones Industrial Average

The Dow 30, or Dow Jones Industrial Average, is a stock index that tracks the performance of the 30 biggest companies listed on the stock indices in the United States. Despite being used by analysts t

-

![Rule of 72: Calculate Investment Doubling Time | [Your Brand Name]](https://www.etffin.com/article/uploadfiles/202110/2021100815281678_S.png)

Rule of 72: Calculate Investment Doubling Time | [Your Brand Name]

In finance, the Rule of 72 is a formula that estimates the amount of time it takes for an investment to double in value, earning a fixed annual rate of returnRate of ReturnThe Rate of Return (ROR) is

invest

- Darvas Box Strategy: A Beginner's Guide to Profitable Trading

- Elliott Wave Theory: A Comprehensive Guide for Traders

- Understanding the Greater Fool Theory: Market Valuation & Irrational Exuberance

- Local Expectations Theory: Understanding Bond Yields & Term Structure

- MSCI Emerging Markets Index: Definition & Key Facts

- Preferred Habitat Theory in Bond Markets: An Explanation

- Random Walk Theory Explained: Understanding Market Price Movements

- Understanding the Liquidity Preference Theory: A Comprehensive Explanation

- November Market Movers: Trade Deal Optimism & Fed Policy

-

Arbitrage Pricing Theory (APT): A Comprehensive Overview

Arbitrage Pricing Theory (APT): A Comprehensive OverviewThe Arbitrage Pricing Theory (APT) is a theory of asset pricing that holds that an asset’s returnsReturn on Assets & ROA FormulaROA Formula. Return on Assets (ROA) is a type of return on inv...

-

June Market Recap: Trade Optimism & Fed Rate Outlook Drive Gains

June Market Recap: Trade Optimism & Fed Rate Outlook Drive GainsOverview Optimism on trade paired with indications the Fed will cut rates drove all major asset classes higher. By changing tune on the direction of rates, the central bank indicated concern about mix...