Local Expectations Theory: Understanding Bond Yields & Term Structure

In finance and economics, the Local Expectations Theory is a theory that suggests that the returns of bonds with different maturities should be the same over the short-term investment horizonInvestment HorizonInvestment horizon is a term used to identify the length of time an investor is aiming to maintain their portfolio before selling their securities for a profit. An individual’s investment horizon is affected by several different factors. However, the primary determining factor is often the amount of risk that the investor. Essentially, the local expectations theory is one of the variations of the pure expectations theory, which assumes that the entire term structure of a bond reflects the expectations of the market regarding future short-term rates.

Understanding the Local Expectations Theory

If an investor purchases two identical bonds where one bond comes with five years to maturity while another bond comes with 10 years to maturity, the local expectations theory implies that over the short-term investment period (e.g., six months), both bonds will deliver equivalent returns to the investor.

The rationale behind the theory is that the returns of bonds are primarily based on market expectations about forward rates.Forward RateThe forward rate, in simple terms, is the calculated expectation of the yield on a bond that, theoretically, will occur in the immediate future, usually a few months (or even a few years) from the time of calculation. The consideration of the forward rate is almost exclusively used when talking about the purchase of Treasury bills It also suggests that bonds with longer maturities do not compensate investors for interest rate riskInterest Rate RiskInterest rate risk is the probability of a decline in the value of an asset resulting from unexpected fluctuations in interest rates. Interest rate risk is mostly associated with fixed-income assets (e.g., bonds) rather than with equity investments. or reinvestment rate risk.

Unlike other variations of the pure expectations theory, the local expectations theory addresses the restrictive holding period (short-term investment horizon) in which the returns of the bonds are expected to be equal.

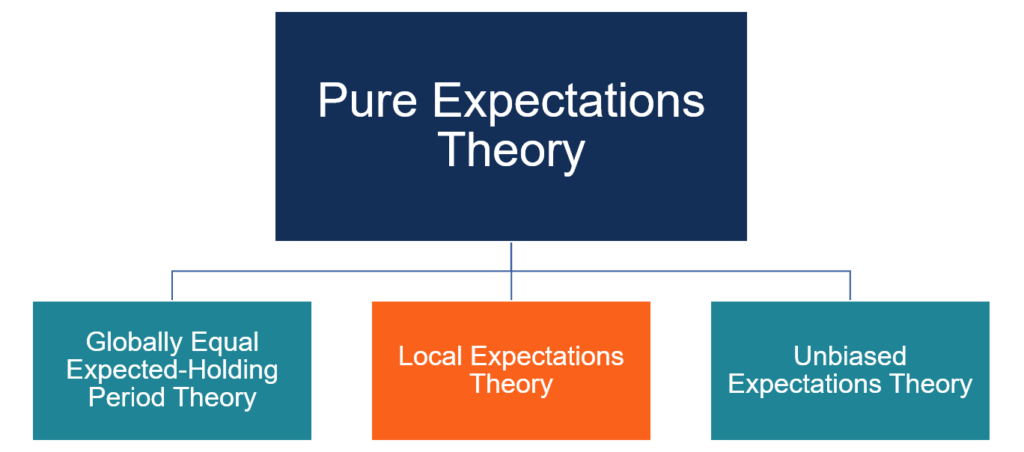

Pure Expectations Theory and its Variations

As mentioned above, the local expectations theory is a variation of the pure expectations theory. The pure expectations theory asserts that future short-term interest rates can be predicted using current long-term interest ratesInterest RateAn interest rate refers to the amount charged by a lender to a borrower for any form of debt given, generally expressed as a percentage of the principal..

In addition to the local expectations theory, the pure expectations theory comes with several other variations. The most common variations of the theory include the following:

1. Globally Equal Expected-Holding Period Return Theory

The first variation of the pure expectations theory assumes that the returns on bonds for a given holding period must be identical despite the time to maturity of the bonds.

For example, if an investor purchases one bond with the time to maturity of five years and another bond with the time to maturity of 10 years, the globally equal expected-holding period return theory suggests that for a certain holding period (no matter if the holding period is six months or three years), the returns on both bonds must be the same.

2. Local Expectations Theory

The local expectations theory is very similar to the globally equal expected-holding period return theory mentioned above. However, the main difference between the two is that the local expectations theory is restricted only to the short-term investment horizon.

In other words, if an investor buys one bond with a time to maturity of five years and another bond with a time to maturity of 10 years, the local expectations theory asserts that the returns on the bonds should be identical only during the short-term (e.g., six months).

3. Unbiased Expectations Theory

The unbiased expectations theory is the most commonly encountered variation of the pure expectations theory. The unbiased expectations theory assumes that current long-term interest rates can be used to predict future short-term interest rates.

Instead of purchasing one two-year bond, an investor may buy a one-year bond now and another one-year bond later. According to the unbiased expectations theory, the returns should be identical in either case.

Final Word

Although the pure expectations theory and its variations provide a simple and intuitive way to understand the term structure of interest rates, the theories do not usually hold in the real world. In reality, the current long-term interest rates also reflect the compensation for various risks such as interest rate risk.

Ultimately, the pure expectations theory requires the presence of perfectly efficient markets. The preferred habitat theory provides a better option to understand the term structure of interest rates in the real world.

More Resources

Thank you for reading CFI’s explanation of the local expectations theory. CFI is the official provider of the global Financial Modeling & Valuation Analyst (FMVA)™Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional resources below will be useful:

- Hurdle RateHurdle Rate DefinitionA hurdle rate, which is also known as minimum acceptable rate of return (MARR), is the minimum required rate of return or target rate that investors are expecting to receive on an investment. The rate is determined by assessing the cost of capital, risks involved, current opportunities in business expansion, rates of return for similar investments, and other factors

- Rational ExpectationsRational ExpectationsRational expectations is an economic theory that states that individuals make decisions based on the best available information in the market

- Stock Investing: A Guide to Value InvestingStock Investing: A Guide to Value InvestingSince the publication of "The Intelligent Investor" by Ben Graham, what is commonly known as "value investing" has become one of the most widely respected and widely followed methods of stock picking.

- Systematic RiskSystematic RiskSystematic risk is that part of the total risk that is caused by factors beyond the control of a specific company or individual. Systematic risk is caused by factors that are external to the organization. All investments or securities are subject to systematic risk and therefore, it is a non-diversifiable risk.

-

Understanding the Dot-Com Bubble: Causes, Impact & Lessons Learned

The dotcom bubble is a stock market bubble that was caused by speculation in dotcom or internet-based businesses from 1995 to 2000. The companies were largely those with a “.com” domain on

-

Understanding the Dow Divisor: How It Impacts the DJIA

The Dow divisor, in simple terms, is a number used to help calculate the Dow Jones Industrial Average (DJIA)Dow Jones Industrial Average (DJIA)The Dow Jones Industrial Average (DJIA), also referred to

invest

- Darvas Box Strategy: A Beginner's Guide to Profitable Trading

- Dow 30 Explained: Understanding the Dow Jones Industrial Average

- Elliott Wave Theory: A Comprehensive Guide for Traders

- Understanding the Greater Fool Theory: Market Valuation & Irrational Exuberance

- Modern Portfolio Theory (MPT): Maximize Returns, Minimize Risk

- Preferred Habitat Theory in Bond Markets: An Explanation

- Random Walk Theory Explained: Understanding Market Price Movements

- Segmented Markets Theory: Understanding Bond Term Structure

- Understanding the Liquidity Preference Theory: A Comprehensive Explanation

-

Understanding the Call Market: Trading Hours & Price Determination

Understanding the Call Market: Trading Hours & Price DeterminationThe call market refers to a market where trading does not take place continuously, but only at specified times during the trading day. Prices are dictated by the exchange rather than by bids and offer...

-

Understanding the Credit Curve: A Guide for Investors

Understanding the Credit Curve: A Guide for InvestorsThe credit curve is the graphical representation of the relationship between the return offered by a security (credit-generating instrument) and the time to maturity of the security. It measures the i...