Understanding Call Protection in Bonds: Investor Protection Explained

Call protection refers to protection from investment risk to bond investors that exists by limiting the conditions under which a bond issuer may elect to call, i.e., redeem bonds before a bond’s stated maturity date.

A call protection provision in a bond’s indenture, which outlines all the terms of the bond, may exist in one or two forms. The first form of call protection limits the time frame during which a bond may be redeemed early by the issuer. The second form of call protection requires the bond issuerBond IssuersThere are different types of bond issuers. These bond issuers create bonds to borrow funds from bondholders, to be repaid at maturity. to pay a premium when redeeming a bond before maturity.

Summary

- Call protection refers to protection from investment risk to bond investors that exists by limiting the conditions under which a bond issuer may elect redeem bonds before their stated maturity date.

- Call protection provisions limit the time frame during which a bond may be called and may require the issuer to pay investors a premium over the bond’s face value.

- Hard call protections, the most common form of call protection, govern the time frame during which a bond may be subject to early redemption.

Understanding Callable Bonds

Bond issuers often include a call provision in the bond purchase contract, which gives them the option to redeem the bond before its stated maturity date under certain conditions. Bond issuers desire a call option for early redemption to protect themselves in the event of a falling interest rate environment.

For example, consider a bond issuer who issues 10-year bonds with a stated interest rate of 9%. Now, assume that five years after the bonds are issued, prevailing interest rates fall to 5%. If the bonds include a call optionCall OptionA call option, commonly referred to as a "call," is a form of a derivatives contract that gives the call option buyer the right, but not the obligation, to buy a stock or other financial instrument at a specific price - the strike price of the option - within a specified time frame. that enables the issuer to redeem the bonds early, the issuer can do so and then issue new bonds that will only require them to pay 5% interest for their borrowed funds instead of the 9% interest that the previous bonds required. As it would represent substantial savings on their debt financing, it is in the bond issuer’s best interest to redeem the bonds early.

Of course, such a benefit for the bond issuer is a disadvantage for the bond buyer. If the bonds are called after only five years, the bond buyer only receives a 9% annual interest return on their investment for half the time that they initially expected to. The bond buyer’s only choice will be to reinvest their returned principal and the interest earned on the bond through five years in new bonds that will, in all probability, only be offering the prevailing rate of 5%.

Because of the potential loss of investment return for the bond buyer, the bond purchase contract usually offers the buyer compensation for the risk in the form of call protection that, as noted, limits the conditions under which the bond issuer can exercise the early redemption option.

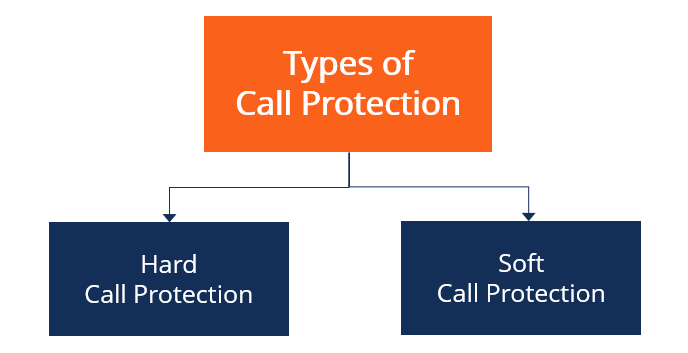

Types of Call Protection

1. Hard Call Protection

The first form of call protection that may be offered to bond buyers is called hard call protection. It is a provision that prohibits the bond issuer from calling the bonds until after a stated amount of time has elapsed.

For example, a 20-year bond may include a hard call protection that only allows the issuer to redeem the bonds after the first ten years of the bond’s life. Thus, bond buyers are assured of earning the bond’s stated interest rate, also known as the coupon rateCoupon RateA coupon rate is the amount of annual interest income paid to a bondholder, based on the face value of the bond., for at least that 10-year period.

2. Soft Call Protection

The second form is referred to as soft call protection. A soft call protection provision exists in addition to a hard call protection that governs the time frame during which bonds may be called. The provision requires the bond issuer to pay bond buyers a premium over and above the bond’s face value if it elects to redeem the bond before maturity.

Soft call protections are often stair-stepped, requiring the bond issuer to pay a higher premium for earlier redemption. For example, once again, consider a 20-year bond with a 10-year hard call protection.

The additional soft call protection might require the bond issuer to pay a 5% premium over the bond’s face value if it elects to redeem the bond in year 10 or 11; a 3% premium if it calls the bond in year 12 or 13; a 2% premium if it calls the bond in year 14 or 15; and only a 1% premium if it calls the bond somewhere between year 16 and year 19.

Related Readings

CFI offers the Capital Markets & Securities Analyst (CMSA)™Program Page - CMSAEnroll in CFI's CMSA® program and become a certified Capital Markets &Securities Analyst. Advance your career with our certification programs and courses. certification program for those looking to take their careers to the next level. To keep learning and developing your knowledge base, please explore the additional relevant resources below:

- Call ProvisionCall ProvisionA call provision refers to a clause – essentially, an embedded option - in a bond purchase contract that gives the bond’s issuer the right to

- Exercise PriceExercise PriceThe exercise price within an option is the price at which the holder is capable of purchasing the underlying asset. If the market price of

- Non-Callable BondNon-Callable BondA non-callable bond is a bond that is only paid out at maturity. The issuer of a non-callable bond can’t call the bond prior to its date of maturity. It is different from a callable bond, which is a bond where the company or entity that issues the bond owns the right to repay the face value of the bond

- Options: Calls and PutsOptions: Calls and PutsAn option is a derivative contract that gives the holder the right, but not the obligation, to buy or sell an asset by a certain date at a specified price.

-

Amortized Bonds: Understanding Principal Repayment

An amortized bond is a bond with the principal amount – otherwise known as face value –regularly paid down over the life of the bond. The bond’s principal is divided up according to

-

ASCOT Options: Understanding Asset-Swapped Convertible Options

The term ASCOT is short for Asset Swapped Convertible Option Transaction. It is an American style call option to buy back a convertible bond. It falls under the category of financial products called s

invest

- Understanding Call Dates: What You Need to Know

- Call Premium Explained: Understanding Issuer Redemptions & Option Pricing

- Understanding Call Prices: Callable Bonds & Preferred Stocks

- Understanding Call Provisions in Bonds: A Comprehensive Guide

- Understanding Call Risk in Bonds: A Comprehensive Guide

- Coupon Bonds: Understanding Fixed Income & Interest Payments

- Discount Bonds: Understanding Pricing & Secondary Markets

- Understanding Hard Call Protection in Callable Bonds

- Make-Whole Call Provisions: Understanding Early Bond Redemption

-

Understanding Bond Accretion: A Comprehensive Guide

Understanding Bond Accretion: A Comprehensive GuideAccretion is a finance term that refers to the increment in the value of a bond after purchasing it at a discount and holding it until the maturity date. A bond is said to be purchased at a discount p...

-

Understanding Amortizable Bond Premiums: A Comprehensive Guide

Understanding Amortizable Bond Premiums: A Comprehensive GuideAn amortizable bond premium refers to the excess amount paid for a bond over its face value or par valuePar ValuePar Value is the nominal or face value of a bond, or stock, or coupon as indicated on a...