Negative Goodwill Explained: Understanding Bargain Purchases

The negative goodwill (NGW) amount, also known as the “bargain purchase” amount, is the difference between the purchase price paid for an asset and its actual fair market value.

Negative goodwill is an accounting principle that occurs when the price paid for an asset is lower than its value in the market and can be thought of as a “discount” to the buyer.

Tangible/Intangible Assets and Negative Goodwill

It is important to distinguish between tangible and intangible assets:

Tangible assets come in a physical form and hold monetary value. Primary examples include property, plant, and equipment.

Intangible assets lack a physical form, do not hold monetary value, and can be unidentifiable at times. Examples of intangible assets include intellectual property (patentsPatentsPatents are documents that grant ownership of intellectual property – the idea of, or concept for, something – to an individual, group, or company. A patent, copyrights), brand recognition, and useful life.

Goodwill accounts for the value of the intangible assets – such as brand recognition and intellectual property – which can be highly valuable for well-established and/or innovative companies. Intangible assets are not included in the calculation of the market value but may be included in the purchase price.

However, the presence of negative goodwill itself implies that the purchase price was lower than the market value – indicating that intangible assets had a discounted or no value or that the company is being sold under pressure without reaping the benefits of its intangible assets.

Therefore, negative goodwill implies that the selling company is under extremely unfavorable circumstances – it could either be financially distressed, under high selling pressure, and/or facing high debt obligations, which lead to a discount on the purchase price of a company.

Practical Example

Company XYZ faced growing competition and incurred debt obligations that it could not cover. The board of directors had two choices – either file for bankruptcyBankruptcyBankruptcy is the legal status of a human or a non-human entity (a firm or a government agency) that is unable to repay its outstanding debts or sell the company.

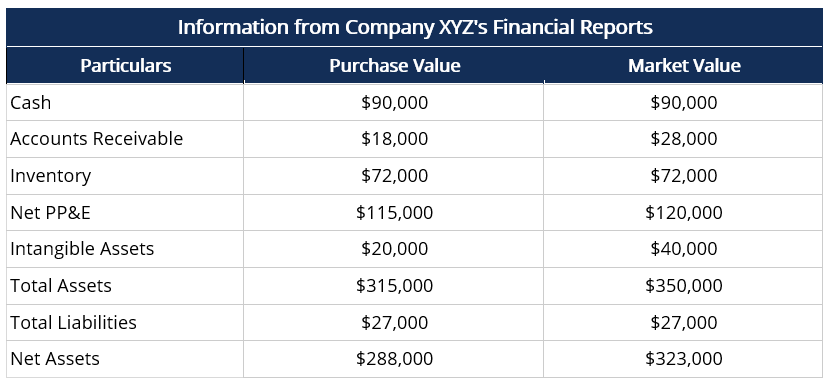

The company was recently sold for $288,000, which was lower than its fair market value. The table below reports consolidated information from Company XYZ’s financial statements:

Here:

- The purchase value of accounts receivable is lower than the fair market value due to deteriorating relations with debtors and difficulty in recollecting payments.

- The purchase value of property, plant, and equipment (PP&E) is lower than the fair market value because the company failed to account for depreciation accurately.

- The intangible assets of the company, including intellectual property and customer base, were weighed down due to the current financial situation – growing competition and high debt obligations.

Negative Goodwill vs. Goodwill

Negative goodwill occurs when the purchase price paid for an asset is lower than its value in the market. In contrast, goodwill occurs when the purchase price is higher than its market value – i.e., the goodwill amount is the premium paid by the buyer for the intangible value of the company’s assets.

While negative goodwill is an indicator of unfavorable circumstances, the presence of goodwill (i.e., “positive” goodwill) implies that the intangible value of assets is high, and the company is under relatively low pressure to sell – this situation favors the seller.

Why Does Negative Goodwill Arise?

Negative goodwill usually arises due to one of the following:

Forced or financially distressed sale of the company

Companies that are financially distressed and under pressure to sell may be willing to sell the company at a discount in the form of negative goodwill since the value of intangible assets for a distressed firm is likely to be lower.

Incorrect valuation of assets

Valuation of assets, especially long-term fixed assets, may be incorrect – given that macroeconomic factorsMacroeconomic FactorA macroeconomic factor is a pattern, characteristic, or condition that emanates from, or relates to, a larger aspect of an economy rather are constantly changing – and result in inaccurate market values. Similarly, an inaccurate valuation of intangible assets may also result in lower market values and negative goodwill.

Accounting for Negative Goodwill

According to US GAAP and IFRS, both goodwill and negative goodwill must be recognized and accounted for in the acquiring company’s financial statements.

NGW in the Income Statement

Negative goodwill must be recognized as a “gain on acquisition” in the acquirer’s income statement, under non-cash sources of income.

NGW in the Balance Sheet

In the balance sheet of the selling company, goodwill is recorded as an asset, whereas negative goodwill is part of the liabilities since it reduces the valuation. Alternatively, goodwill may be recorded as a contra-asset, or a reduction to assets to indicate the amount of NGW.

NGW in the Statement of Cash Flows

In the statement of cash flows, negative goodwill is usually recorded as a “gain on acquisition” or “gain on bargain purchase” to indicate the additional value acquired in the form of NGW.

Related Readings

CFI offers the Commercial Banking & Credit Analyst (CBCA)™Program Page - CBCAGet CFI's CBCA™ certification and become a Commercial Banking & Credit Analyst. Enroll and advance your career with our certification programs and courses. certification program for those looking to take their careers to the next level. To keep learning and advancing your career, the following resources will be helpful:

- Net Asset ValueNet Asset ValueNet asset value (NAV) is defined as the value of a fund’s assets minus the value of its liabilities. The term "net asset value" is commonly used in relation to mutual funds and is used to determine the value of the assets held. According to the SEC, mutual funds and Unit Investment Trusts (UITs) are required to calculate their NAV

- Fair Market ValueFair Market ValueThe fair market value (of a good or service being exchanged) refers to the price at which both transacting parties agreed to independently.

- IFRS vs. US GAAPIFRS vs. US GAAPThe IFRS vs US GAAP refers to two accounting standards and principles adhered to by countries in the world in relation to financial reporting

- Statement of Cash FlowsStatement of Cash FlowsThe Statement of Cash Flows (also referred to as the cash flow statement) is one of the three key financial statements that report the cash

-

Value Engineering: Definition, Benefits & Implementation

Value engineering refers to the systematic method of improving the value of a product that a project produces. It is used to analyze a service, system, or product to determine the best way to manage t

-

Value Proposition: Definition, Examples & How to Create One

A value proposition is a promise of value stated by a company that summarizes how the benefit of the company’s product or service will be delivered, experienced, and acquired. Essentially, a val

Accounting

- Understanding Financial Denomination: A Comprehensive Guide

- Understanding Equity: A Comprehensive Guide for Investors

- Face Value Explained: Definition, Examples & Importance

- Understanding Fair Value: Definition & Importance

- Understanding Money: Definition, History & Value

- Goodwill in Accounting: Definition & Value

- Understanding Goodwill Impairment: A Comprehensive Guide

- Negative Assurance Explained: Auditor's Confirmation & Its Significance

- Par Value Explained: Understanding Bonds & Stocks

-

Understanding Negative Carry: Risks and Strategies

Understanding Negative Carry: Risks and StrategiesNegative carry is a carry trade with a negative yield, meaning the cost of holding (carrying) the investment exceeds the yield. How It WorksIn some rare circumstances, it is prudent to...

-

Negative Gearing Explained: Understanding Investment Losses & Tax Benefits

Negative Gearing Explained: Understanding Investment Losses & Tax BenefitsNegative gearing occurs when an investment that is made using borrowed funds produces cash flows that are lower than the interest and other expensesExpensesAn expense is a type of expenditure that flo...