Times Interest Earned Ratio (Cash Basis): Calculation & Interpretation

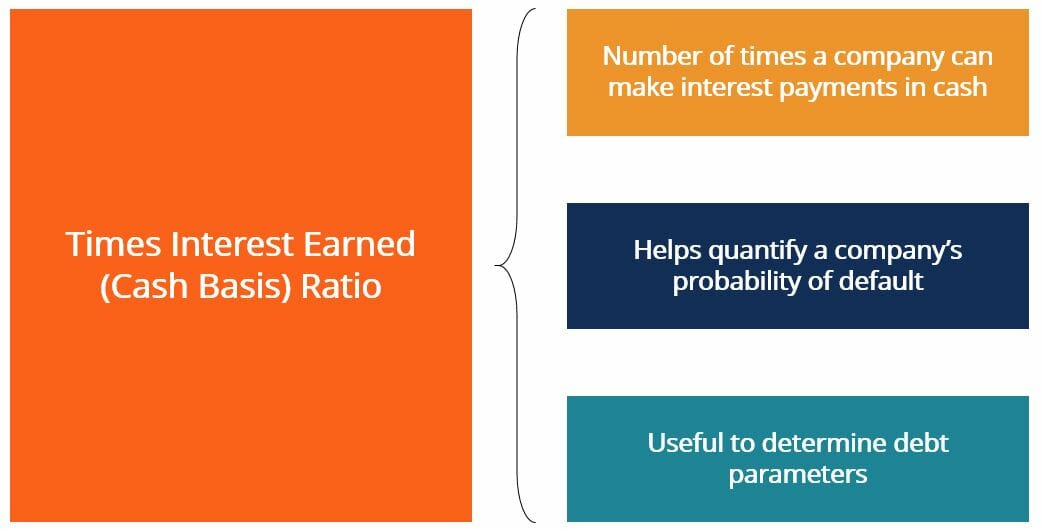

The Times Interest Earned (Cash Basis) (TIE-CB) ratio is very similar to the Times Interest Earned RatioTimes Interest EarnedThe Times Interest Earned (TIE) ratio measures a company's ability to meet its debt obligations on a periodic basis. This ratio can be calculated by dividing a company's EBIT by its periodic interest expense. The ratio shows the number of times that a company can make its periodic interest payments. Times Interest Earned (Cash Basis) measures a company’s ability to make periodic interest payments on its debt. The main difference between the two ratios is that Times Interest Earned (Cash Basis) utilizes adjusted operating cash flow rather than earnings before interest and taxes (EBIT)EBIT GuideEBIT stands for Earnings Before Interest and Taxes and is one of the last subtotals in the income statement before net income. EBIT is also sometimes referred to as operating income and is called this because it's found by deducting all operating expenses (production and non-production costs) from sales revenue.. Thus, the ratio is computed on a “cash basis”, which only takes into account how much disposable cash a business has on hand. This is cash that can be used to make debt repayments.

The TIE-CB’s main goal is to quantify the probability that a business will default on its loans. This information is useful in determining various debt parameters such as the appropriate interest rate a lender should charge the company or the amount of debtDebt CapacityDebt capacity refers to the total amount of debt a business can incur and repay according to the terms of the debt agreement. that a company can safely take on.

A relatively high TIE-CB ratio indicates that a company has a lot of cash on hand that it can devote to repaying debts, thus lowering its probability of default. This makes the business a more attractive investment for debt providers. Conversely, a low TIE-CB means that a company has less cash on hand to devote to debt repayment. Thus, there would be a higher probability of default.

How to calculate the Times Interest Earned Ratio (Cash Basis)

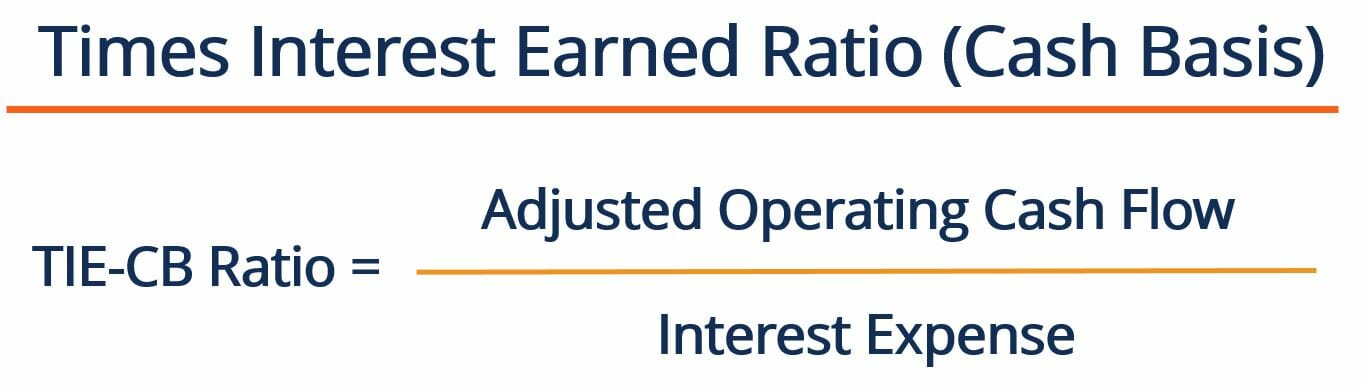

The Times Interest Earned ratio CB can be calculated by dividing a company’s adjusted cash flow from operations by its periodic interest expense. The formula to calculate the ratio is:

Where:

Adjusted Operating Cash Flow = Cash Flow From OperationsOperating Cash FlowOperating Cash Flow (OCF) is the amount of cash generated by the regular operating activities of a business in a specific time period. + TaxesAccounting For Income TaxesIncome taxes and their accounting is a key area of corporate finance. There are several objectives in accounting for income taxes and optimizing a company's valuation. + Fixed ChargesFixed and Variable CostsCost is something that can be classified in several ways depending on its nature. One of the most popular methods is classification according

Interest Expense – represents the periodic debt payments that a company is legally obligated to make to its creditors

While a high TIE-CB ratio is almost always preferred over a low ratio, an excessively high TIE-CB may mean the company may not be making the best use of its cash. For instance, a high ratio could indicate that a company may not be investing in new NPV positive projects, conducting research & development, or paying out dividends to its stockholders. As a result of this, the company may see a decrease in profitability (and subsequently cash) in the long term.

Times Interest Earned (Cash Basis) Example

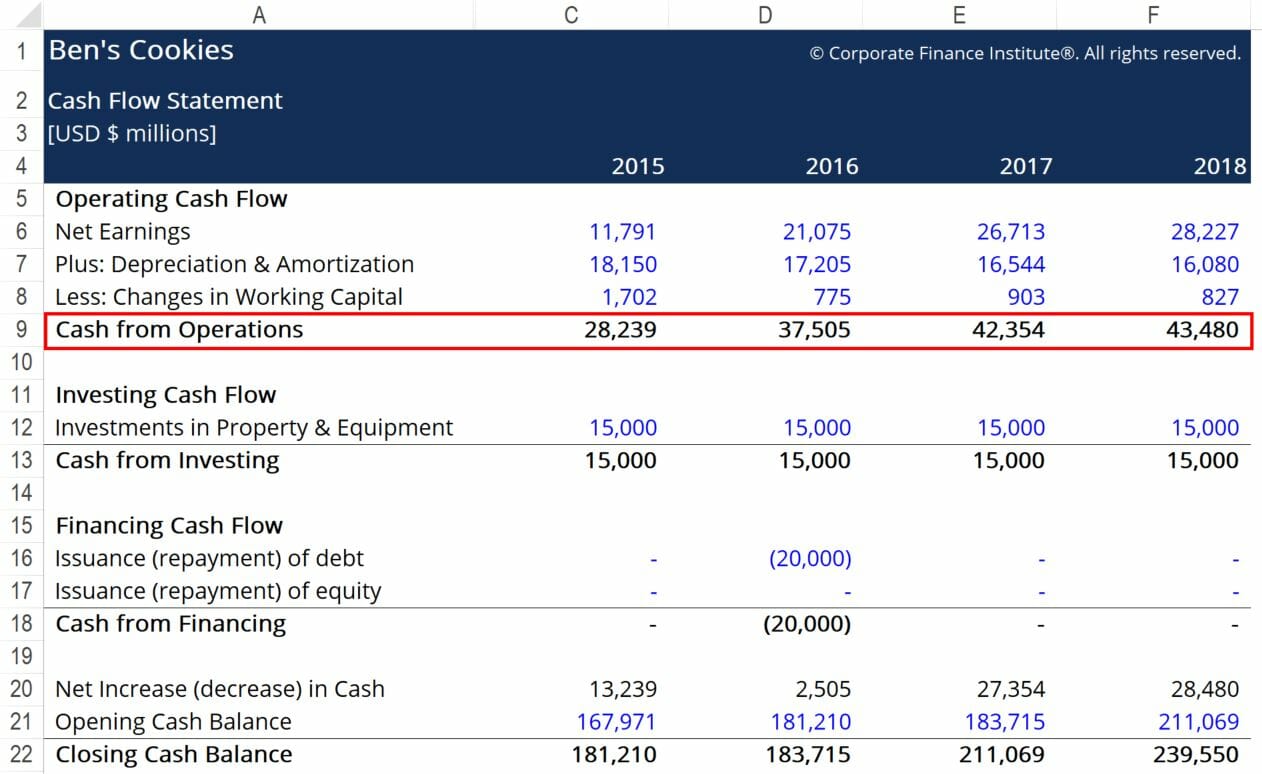

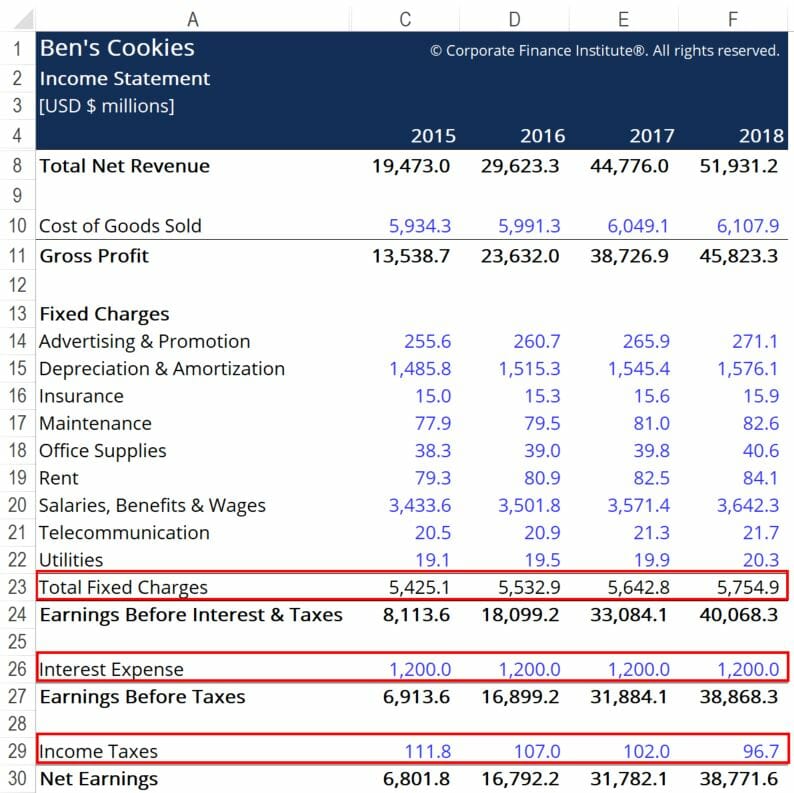

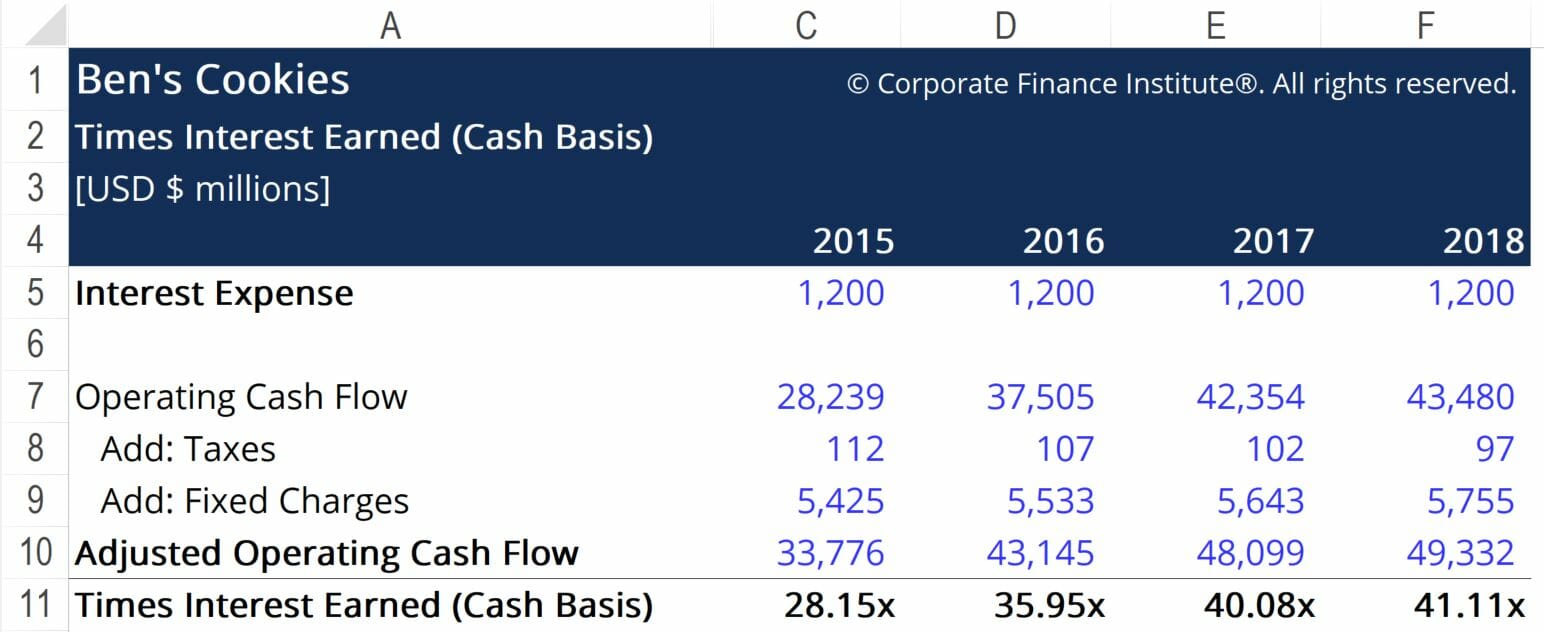

Ben’s Cookies wants to calculate its Times Interest Earned (cash basis) ratio in order to get a better idea of its debt repayment ability. Below are snippets from the business’ financial statements, with the required inputs highlighted by red boxes:

Using the formula provided above, we arrive at the following figures:

Here, we see that Ben’s TIE-CB slowly increases year over year, up to 41.11x interest in 2018. This would generally be a good indicator of financial health, as it means that Ben’s has enough cash to pay the interest on its debt. If Ben were to apply for more loans, he likely has a good chance of securing further financing, as there is a relatively low probability of default.

To better understand the financial health of the business, the TIE-CB ratio should be computed for a number of companies that operate in the same industry. If other firms operating in this industry see TIE-CB multiples that are, on average, lower than Ben’s, we can conclude that Ben’s is doing a relatively better job of managing its financial leverage. Creditors are more likely to extend further credit to Ben’s, over its competitors, if needed.

Additional Resources

Thank you for reading this CFI article on the Times Interest Earned ratio CB! CFI offers the Financial Modeling & Valuation Analyst (FMVA)™Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program for those looking to take their careers to the next level. To learn more about related topics, check out the following free CFI resources:

- How to Calculate Debt Service Coverage RatioHow to Calculate Debt Service Coverage RatioThis guide will describe how to calculate the Debt Service Coverage Ratio. First, we will go over a brief description of the Debt Service Coverage Ratio, why it is important, and then go over step-by-step solutions to several examples of Debt Service Coverage Ratio Calculations.

- Current Portion of Long-Term DebtCurrent Portion of Long-Term DebtThe current portion of long-term debt is the portion of long-term debt due that is due within a year’s time. Long-term debt has a maturity of

- Accounting Fundamentals Course – CFI

- Defensive Interval RatioDefensive Interval RatioThe defensive interval ratio (DIR) is a financial liquidity ratio that indicates how many days a company can operate without needing to tap into capital sources other than its current assets. It is also known as the basic defense interval ratio (BDIR) or the defensive interval period ratio (DIPR).

-

Sharpe Ratio: Calculate & Interpret Investment Performance

Named after American economist, William Sharpe, the Sharpe Ratio (or Sharpe Index or Modified Sharpe Ratio) is commonly used to gauge the performance of an investment by adjusting for its risk.The hig

-

Times Interest Earned (TIE): Understanding Financial Health

Times interest earned (TIE) is a financial ratio that measures a company’s ability to meet its interest obligations based on its current income. This ratio is important to current and prospective cred

finance

- Cash Conversion Ratio (CCR): Definition & Importance

- Cash Flow to Debt Ratio: Understanding and Calculation

- Cash Ratio: Understanding Your Company's Short-Term Liquidity

- Cash Turnover Ratio (CTR): Calculation & Interpretation

- Understanding the Operating Cash Flow Ratio: A Key Liquidity Metric

- Operating Cash to Debt Ratio: Understanding Financial Health

- Price-to-Cash Flow Ratio (P/CF): Definition & Analysis

- Times Interest Earned (TIE) Ratio: Calculation & Interpretation

- Short Interest Ratio: Understanding Investor Sentiment & Market Risk

-

Reserve Ratio Explained: Understanding Bank Reserves

Reserve Ratio Explained: Understanding Bank ReservesThe reserve ratio – also known as bank reserve ratio, bank reserve requirement, or cash reserve ratio – is the percentage of deposits a financial institution must hold in reserve as cash. ...

-

Understanding the Retention Ratio: Reinvesting for Growth

Understanding the Retention Ratio: Reinvesting for GrowthThe retention ratio (also known as the net income retention ratio) is the ratio of a company’s retained income to its net incomeNet IncomeNet Income is a key line item, not only in the income st...