Make-Whole Call Provisions: Understanding Early Bond Redemption

A make-whole call provision is a clause in a bond’s contract that allows the issuer to retire the bond early by paying off the remaining debt on the bond. Furthermore, a make-whole call provision can be thought of as a call provision in which the debtor can make a lump sum payment to the creditor to retire the bond before its maturity date.

The amount that the issuer must pay the lender is determined by calculating the net present value of the coupon paymentsCoupon RateA coupon rate is the amount of annual interest income paid to a bondholder, based on the face value of the bond. and the principal that the lender would’ve received if the bond was not retired early.

How Do Make-Whole Call Provisions Work?

A make-whole call provision is created when the bond is created; it is a provision included in the bond. The call provision is exercised when the issuer of the bond decides to retire the bond early and pay off the remaining payments. The issuer of the bond is not obligated to exercise a make-whole call provision; however, they have the right to do so.

The remaining amount for the issuer to settle is determined by taking the net present valueNet Present Value (NPV)Net Present Value (NPV) is the value of all future cash flows (positive and negative) over the entire life of an investment discounted to the present. of the remaining coupon payments and the principal – in other words, how much the remaining coupon payments and the principal are worth in today’s dollars.

The discount rateDiscount RateIn corporate finance, a discount rate is the rate of return used to discount future cash flows back to their present value. This rate is often a company’s Weighted Average Cost of Capital (WACC), required rate of return, or the hurdle rate that investors expect to earn relative to the risk of the investment., which is used to calculate the net present value, is determined by an agreed-upon spread over a similar maturity Treasury; for example, if the bond issued has a maturity of 10 years, the agreed-upon spread was 50bps (0.5%), and the 10-year Treasury was yielding 1%, the discount rate would be 1.5%.

In addition, the creditor would receive the greater of the par value of the bond and the net present value when the make-whole call provision is exercised. The issuer of the bond may decide to exercise a make-whole call provision because they have generated enough cash from operations to retire the bond and no longer want it on their balance sheet.

Another reason can be if the company can raise the same or a larger amount of money from a bond at a lower rate than the current bond. Consequently, in either of the situations above, the issuer would exercise the make-whole call provision, and the bond would be retired.

Make-Whole Call Provision vs. Traditional Call

A make-whole call provision and a traditional call provision share many similarities; for example, they both give the issuer the right to retire the bond. However, a traditional call can only be exercised after a previously determined date, whereas a make-whole call provision can be exercised anytime during the bond’s horizon.

In addition, a make-whole call provision uses the greater of the par valuePar ValuePar Value is the nominal or face value of a bond, or stock, or coupon as indicated on a bond or stock certificate. It is a static value and net present value to determine the payment to the lender, while the traditional call method uses a predetermined fixed call price or a predetermined call schedule.

Advantage of Make-Whole Call Provisions

Higher returns

Make-whole call provisions are typically advantageous to investors when they are exercised, as they are typically compensated at a value above the bond’s fair value due to the “make-whole spread.”

On the contrary, the bond issuer can ask for a higher price for a bond with a make-whole call provision, as the provision presents the opportunity for the lender to earn a higher return.

Also, a bond with a make-whole call provision is more advantageous than a bond with a traditional call provision when interest rates fall, and the issuer calls the bond. The investor of the traditional call bond would only receive the predetermined call price, whereas the investor of the make-whole call provision bond would receive the higher of the par value of the bond and the net present value.

When interest rates fall, the net present value rises, which presents a more advantageous opportunity for make-whole call bond investors.

Practical Example

The following is an example of a make-whole call provision being exercised:

- Assumed a coupon payment has just been made.

- There are exactly five years until the bond matures.

- $1,000 face value and 5% annual coupon.

- Reference Treasury is yielding 1%.

- Make-whole spread is 0.5%.

By calculating the net present value using a discount rate of 1.5% (Reference Treasury yield + make-whole spread), if the make-whole call provision is exercised today, the issuer would need to pay $1,167.40 for each bond.

Additional Resources

CFI is the official provider of the global Commercial Banking & Credit Analyst (CBCA)™Program Page - CBCAGet CFI's CBCA™ certification and become a Commercial Banking & Credit Analyst. Enroll and advance your career with our certification programs and courses. certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional resources below will be useful:

- Anti-Dilution ProvisionsAnti-Dilution ProvisionsAnti-dilution provisions are clauses that allow investors the right to maintain their ownership percentages in the event that new shares are issued

- Bond PricingBond PricingBond pricing is the science of calculating a bond's issue price based on the coupon, par value, yield and term to maturity. Bond pricing allows investors

- NPV FunctionNPV FunctionThe NPV Function is categorized under Excel Financial functions. It will calculate the Net Present Value (NPV) for periodic cash flows. The NPV will be calculated for an investment by using a discount rate and series of future cash flows. In financial modeling, the NPV function is useful in determining the value of a business

- Noncallable BondsNoncallableNoncallable refers to the type of securities that cannot be redeemed by their issuers before their maturities unless penalties are paid to security holders.

-

Amortized Bonds: Understanding Principal Repayment

An amortized bond is a bond with the principal amount – otherwise known as face value –regularly paid down over the life of the bond. The bond’s principal is divided up according to

-

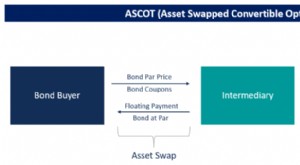

ASCOT Options: Understanding Asset-Swapped Convertible Options

The term ASCOT is short for Asset Swapped Convertible Option Transaction. It is an American style call option to buy back a convertible bond. It falls under the category of financial products called s

invest

- Understanding Call Dates: What You Need to Know

- Call Premium Explained: Understanding Issuer Redemptions & Option Pricing

- Understanding Call Prices: Callable Bonds & Preferred Stocks

- Understanding Call Protection in Bonds: Investor Protection Explained

- Understanding Call Provisions in Bonds: A Comprehensive Guide

- Understanding Call Risk in Bonds: A Comprehensive Guide

- Coupon Bonds: Understanding Fixed Income & Interest Payments

- Discount Bonds: Understanding Pricing & Secondary Markets

- Understanding Hard Call Protection in Callable Bonds

-

Understanding Bond Accretion: A Comprehensive Guide

Understanding Bond Accretion: A Comprehensive GuideAccretion is a finance term that refers to the increment in the value of a bond after purchasing it at a discount and holding it until the maturity date. A bond is said to be purchased at a discount p...

-

Understanding Amortizable Bond Premiums: A Comprehensive Guide

Understanding Amortizable Bond Premiums: A Comprehensive GuideAn amortizable bond premium refers to the excess amount paid for a bond over its face value or par valuePar ValuePar Value is the nominal or face value of a bond, or stock, or coupon as indicated on a...